SoFi Adds $3.6B in Commitments to Loan Platform Business

Plus Step Draws Senate Scrutiny, New York Fed Links Betting to Delinquencies, FICO Scores Slip, Splitit Expands Offline, Klarna Scales $17B in U.S. Lending

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

SoFi adds $3.6 billion in new commitments to its loan platform business, reinforcing its shift toward a capital-light model. Meanwhile, Beast Industries’ acquisition of Step is under fire, with Senator Elizabeth Warren issuing a deadline to address concerns over youth safety and crypto expansion. We’re also looking at a new Fed study linking mobile sports betting to a spike in credit delinquencies, FICO’s latest report on falling U.S. credit scores, and Klarna doubling its credit facility to $2 billion to fuel American growth.

Lots to break down. Let’s get toasting!

— Carlos Caro, Founder at NMG, Co-Founder of The Free Toaster

— Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please share our Newsletter or Podcast with 1 of your colleagues!

SoFi Secures $3.6 Billion in Loan Platform Partnerships

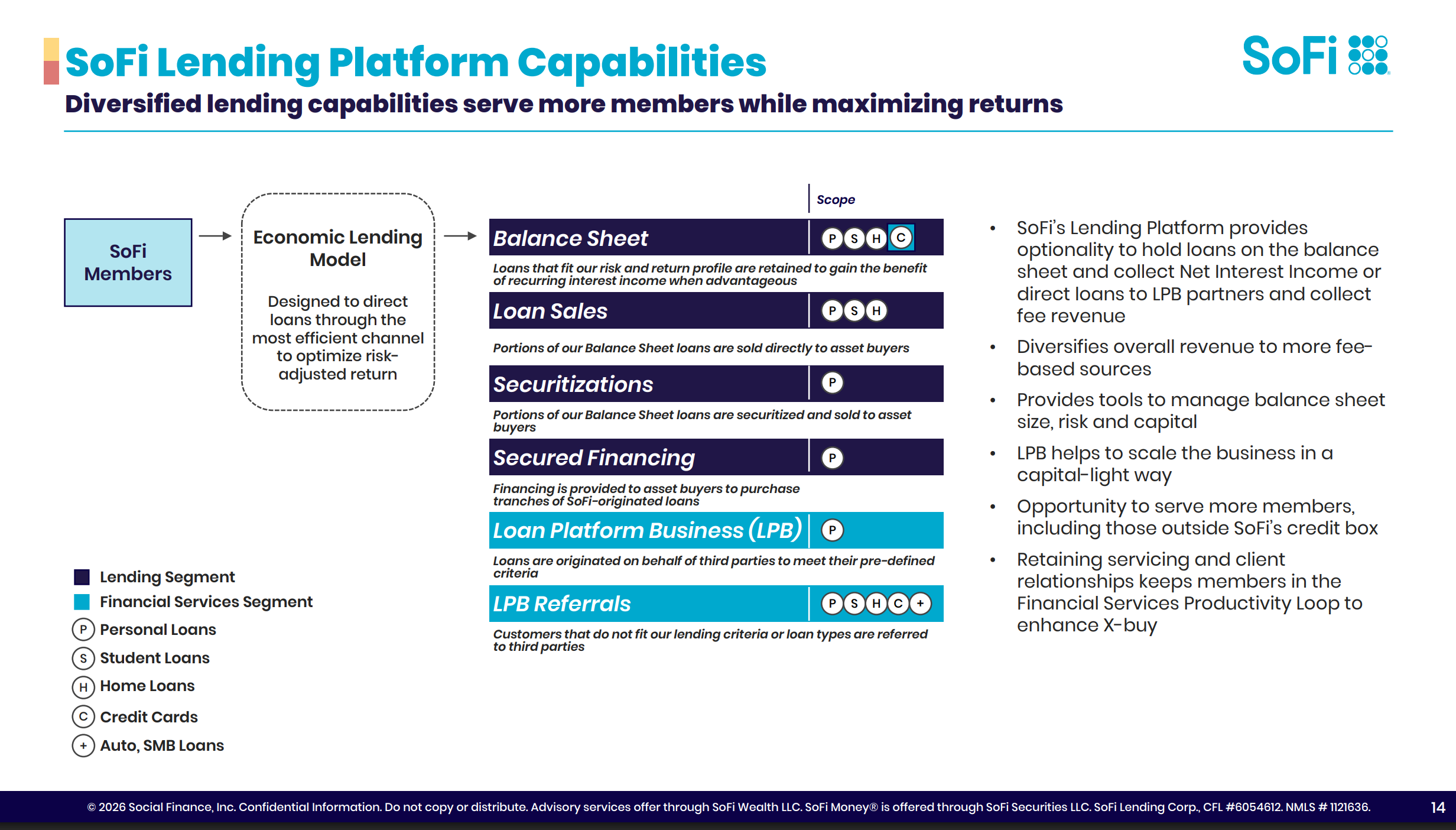

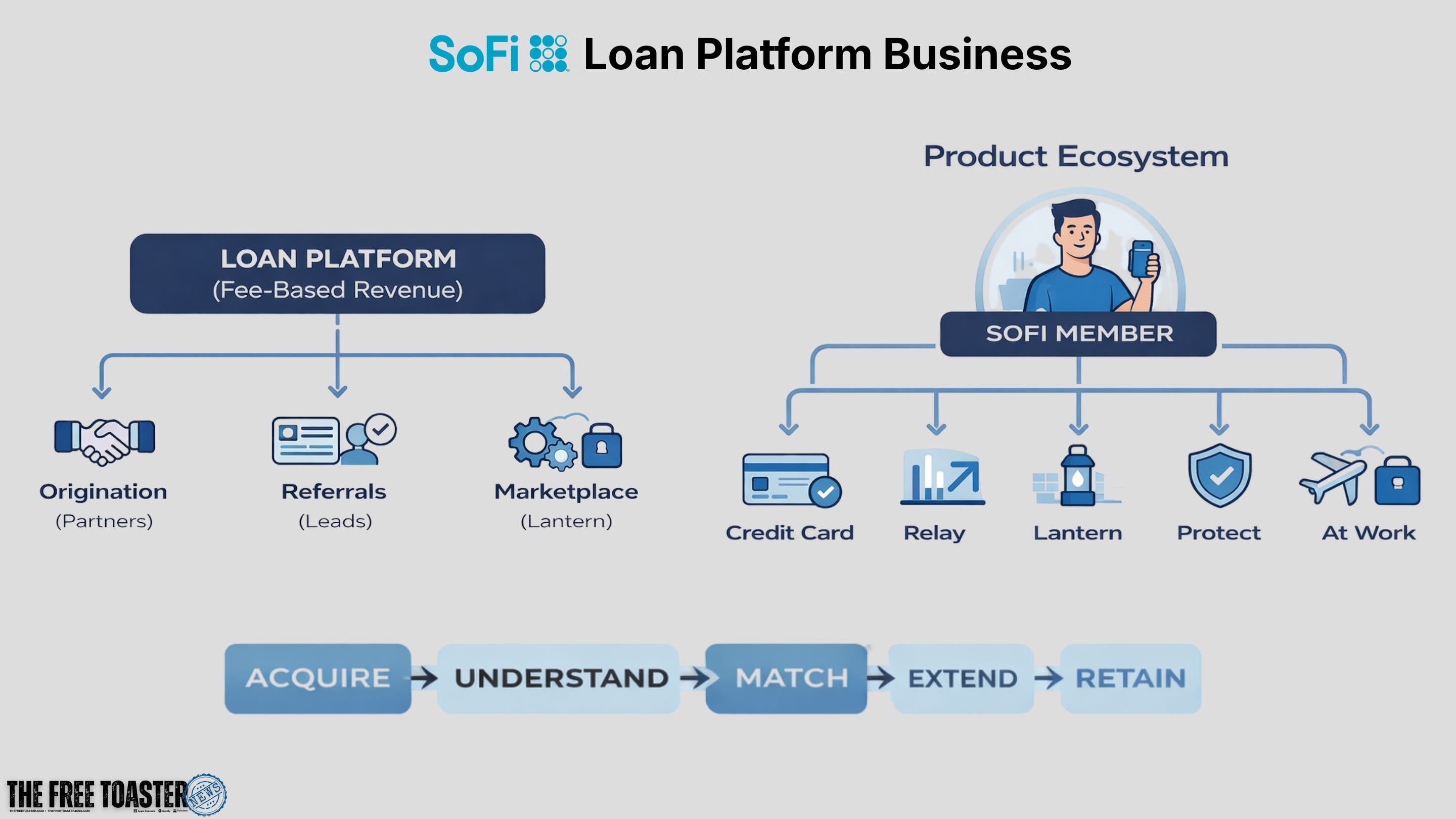

Not every borrower who comes to SoFi gets a SoFi loan. Some fall outside the credit box, meaning they don’t meet SoFi’s own underwriting criteria. That’s where the Loan Platform Business comes in. Instead of a dead end, those borrowers get routed to partners through referrals or the Lantern marketplace. SoFi still earns fee income and retains the servicing relationship. The marketing spend converts regardless of whether SoFi holds the loan.

That context matters for understanding why three new LPB agreements totaling over $3.6 billion in personal loan commitments is a bigger deal than the headline number suggests. A global bank takes $1 billion, a financial services and insurance group $600 million over 12 months, and a top-five global private asset manager up to $2 billion over two years. This follows a year where the LPB pulled in over $10 billion in total commitments.

SoFi spends heavily on brand, stadium naming rights, national TV, celebrity partnerships. That spend drives significant borrower demand. The LPB is what ensures none of that demand goes to waste. SoFi originates on behalf of third parties, collects fees, and retains servicing rights without carrying the credit risk. CEO Anthony Noto framed it plainly: “By connecting strong borrower demand with institutional capital, we’re building a capital-light, fee-based business that complements our overall lending business while leveraging our existing technology platform capabilities in underwriting, pricing, marketing and servicing.”

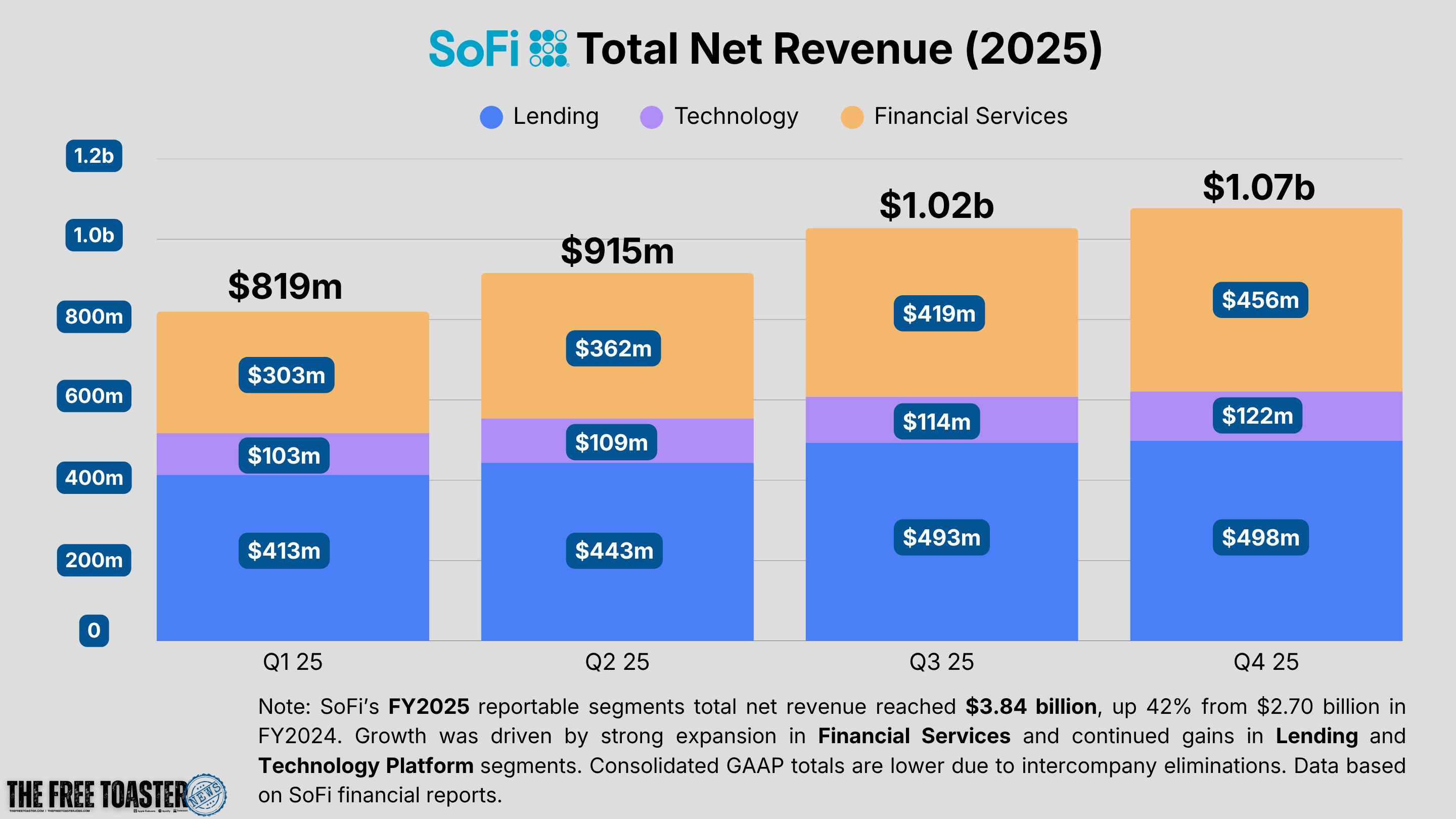

The LPB sits inside SoFi’s Financial Services segment and is a core driver of that segment’s growth, scaling from $303 million in Q1 2025 to $456 million by Q4. In FY2025, the Loan Platform Business accounted for more than 75% of Financial Services noninterest income, making it the segment’s dominant revenue driver by a wide margin.

Three institutional partners in a single announcement reflects growing demand from asset managers for exposure to consumer credit. SoFi’s adjusted net revenue hit $3.61 billion in FY2025, up 35% year over year, with fee-based revenue growing 53%. For fintech operators building in the lending space, the model is worth studying. Serve more customers, hold less risk, keep the relationship. That’s the playbook SoFi is running. (SoFi)

We’re going deeper into the entire SoFi Lending Business, including their LPB in an upcoming issue, breaking down how the model works, what it means for personal lending distribution, and what other fintechs can learn from it. Stay tuned.

Sponsored by Spinwheel

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

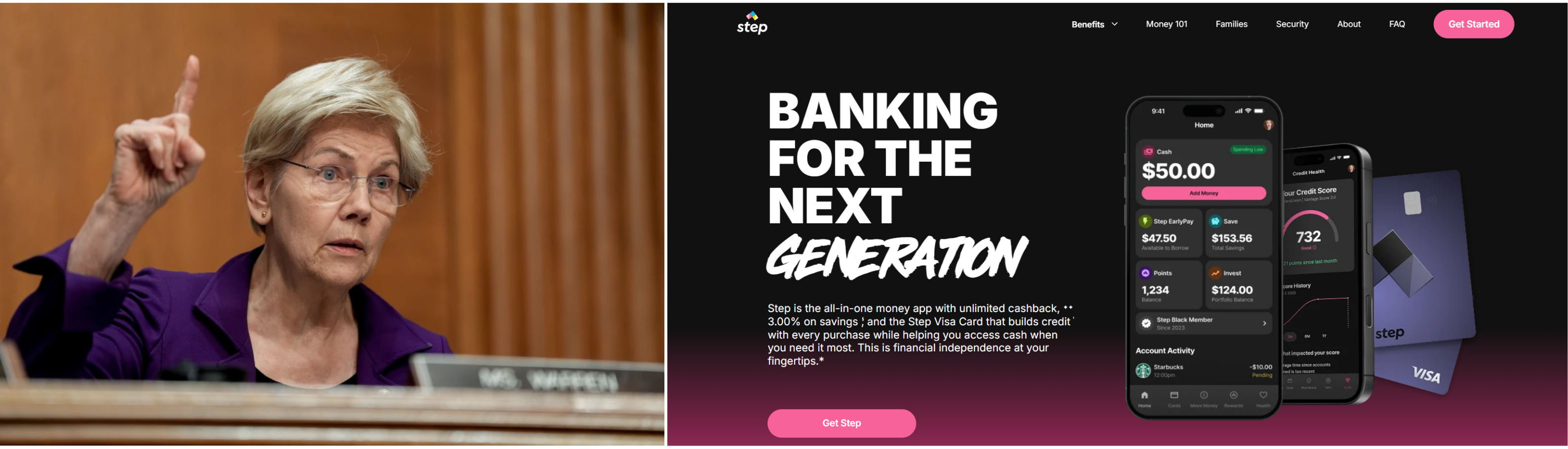

Senator Warren Questions Beast Industries Acquisition of Step Over Youth Safety and Crypto Expansion

Beast Industries faces a formal inquiry from the Senate Banking Committee following its acquisition of Step, a financial app serving 7 million users aged 13 to 18. Senator Elizabeth Warren issued a deadline of April 3 for the company to address concerns regarding insider trading allegations involving a Beast Industries employee and the platform's planned expansion into cryptocurrency exchange services. Step currently uses Evolve Bank and Trust to provide FDIC insurance and credit cards, though Evolve recently settled a class action lawsuit for $11.9 million over a data breach. The acquisition gives Beast Industries access to a user base where 39% of the channel's 471 million subscribers are minors. Beast Industries recently accepted a $200 million investment from Bitmine to integrate decentralized finance into the platform. Warren specifically questioned the lack of a general counsel and formal misconduct reporting at the media company. Beast Industries stated it is currently examining all marketing and compliance to meet regulatory requirements. (American Banker)

The Free Toaster previously covered this acquisition in a past issue and revisited it in a recent podcast episode, breaking down Step’s stalled growth, the economics behind teen neobanks, and the risk of pushing young users toward gambling-adjacent products under monetization pressure.

New York Fed Study Links Sports Betting Legalization to Rising Credit Delinquencies

Under-40 credit card delinquencies rose 7.9% in states following sports betting legalization, according to a report from the Federal Reserve Bank of New York. The New York Fed found that auto loan delinquencies in the same age group increased by 5.6%. While only 3.1% of the population actively bets on sports after legalization, the financial impact is significant enough to lower median credit scores by 1 point across entire counties. Data suggests that for the specific group of individuals who take up gambling, delinquencies jump by approximately 10 percentage points. Younger bettors under 40 see a 26 percentage point spike in late payments. These findings align with separate data from the University of California Consumer Credit Panel showing legalization increases bankruptcy likelihood by 10%. The authors wrote that sports betting can have dramatic implications for household financial stability as access expands through mobile apps and prediction markets like Kalshi and Polymarket. (Bloomberg) (Federal Reserve Bank of New York)

Upgrade’s Launch of Boost Money with John Doppke, VP of Product at Upgrade

In the latest episode of The Free Toaster, Carlos and Nick sit down with John Doppke (VP of Product at Upgrade) to unpack the launch of Boost Money. Discover the strategy behind this "four-in-one" financial account and how cash-flow underwriting is powering a new era of interest-free advances.

Catch us on Apple Podcasts, Spotify, Substack, or your favorite player.

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

FICO Report: Average U.S. Credit Score Falls to 714 as Student Loan and Mortgage Delinquencies Rise

FICO reported the average U.S. credit score fell to 714 in its Spring ’26 Credit Insights report. This 2-point annual decline follows the resumption of student loan payments and a rise in mortgage delinquencies. FICO provides the analytics used by 90% of top U.S. lenders to assess consumer risk. A record 48.1% of consumers now hold scores of 750 or higher. Conversely, 24% of consumers reported skipping or making less than minimum payments over the last 12 months. Gen Z led all age groups in new credit activity with 25% opening at least one new card. Interest rates influenced 77% of consumers in their timing of credit applications. Survey data shows 67% of adults incorrectly believe personal income directly impacts their score. (FICO)

Splitit Expands Card-Linked Installments to Field Sales via Splitit Go

Splitit launched Splitit Go to capture a share of the $4.6 trillion annual U.S. services market where transactions occur face-to-face. This mobile solution allows contractors, medical providers, and automotive shops to offer installment plans via smartphone or tablet. Splitit functions as a card-linked installment platform that uses a customer's existing credit line rather than issuing new loans. Merchants generate payment plans through a QR code, text, or email during in-person consultations. The system requires no new credit applications or third-party underwriting for the consumer. It integrates into existing CRMs and field service platforms through a single API. This launch moves the company's embedded payment technology from e-commerce into physical environments like showrooms and service counters. (Splitit)

Klarna Doubles Elliott Investment Management Facility to $2B to Fuel $17B in US Loan Growth

Klarna doubled its credit facility with Elliott Investment Management to $2 billion to support up to $17 billion in US loan originations over the next three years. The digital bank sells newly originated receivables to Elliott funds on a rolling basis to maintain off-balance-sheet funding. This expansion follows a period where Klarna reported that US financing volume grew significantly in Q4 2025. Under the three-year agreement, Klarna retains all underwriting and servicing responsibilities for its 118 million active users. The company currently processes 3.4 million transactions daily across retailers like Uber, H&M, and Nike. This deal provides the capital required to meet American consumer demand for financing alternatives. (Klarna)

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(Lending) Allied Solutions and Loquat Partner to Deliver Omnichannel Digital Onboarding and Lending (Allied Solutions)

(Lending) Harborstone Credit Union Selects Upstart for Personal Lending (Upstart)

(Cards) American Express Unveils New Graphite™ Business Cash Unlimited Card, Rewarding Business Owners With Unlimited 2% Cash Back (American Express)

(Lending) Wolters Kluwer and FairPlay AI Announce Strategic Partnership to Deliver AI-Driven Fair Lending Optimization Capabilities (Wolters Kluwer)

(Payments) Mastercard Explores Sale of Payments Unit It Bought From Nets in 2019, FT Reports (Reuters)

(Lending) Luana Savings Bank Adopts nCino for Digital Lending (IBS Intelligence)

(Fintech) Plaid Expands Into Media With Acquisition of This Week in Fintech (Fintech News Switzerland)

(Payments) Cardlay Launches U.S. Embedded Spend Platform, Enabling Incumbents to Compete With Turnkey Commercial Spend Platforms (Business Wire)

(Payments) 200 Million More Friends on Venmo – Send Money to PayPal Users Around the World (PayPal)

(Banking) VIDEO: UBS Bank USA National Charter Approval (UBS)

(Lending) Square Expands Access to Capital, Financing More Sellers With Innovative, Tech-Powered Underwriting (Square)

(Marketing) SurgePays Launches Managed Marketing Services Platform Across Nationwide Retail Network (GlobeNewswire)

(Payments) A New Era of Platform Payouts: Branch Is Now Stripe’s Embedded Digital Wallet for Worker Payouts (Branch)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/sofi-adds-36b-in-commitments-to-loan

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.