Did ChatGPT Just Fix The Cash Flow Underwriting Distribution Problem?

Plus the Affiliate Marketing Summit for Lenders

Hey Toaster Readers,

This week is sponsored by New Market Growth.

The way people find and use credit is changing fast, and AI is driving the shift. This week, we look at how large language models are becoming the ultimate distribution channel for cash flow underwriting by turning apps like ChatGPT into personal finance super apps.

We also dive into two new industry reports. Marqeta reveals that consumers are building their own custom portfolio of credit products, while a study from BCG and FT Partners shows fintech hitting a major revenue resurgence driven by real profitability. Plus, we look at Sezzle’s latest super app expansion, including a new Pay-in-5 option that is boosting order values.

There’s a lot of data to unpack. Let’s get toasting!

Carlos Caro, Founder at NMG, Co-Founder of The Free Toaster

Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

But First, An Event You Can’t Miss

Affiliate Marketing Summit for Lenders

Proudly Sponsored by Experian & Engine by Gen

Register NOW for early bird pricing!

Will LLMs Solve Distribution For The Cash Flow Lenders?

(read the full version in our latest editorial here)

We Were Wrong About Cash Flow Underwriting’s Distribution Problem

A year and a half ago, I (Carlos) wrote a piece called Where’s The Consumer Demand For Cash Flow Underwriting (CFU)?

Cash flow underwriting has always had one problem: nobody can sell it. The moment a consumer hits “give us your bank login,” they bail. Application rates tank, throughput drops, and the affiliate marketplaces route volume to bureau-only lenders instead.

I used to think that was a dead end. I don’t anymore.

Second-look is quietly working. Lenders are using CFU not as a primary decision, but as a second chance. Customer gets declined on bureau data. Instead of killing the lead, you offer: share your bank data and we might approve you. The person who just got told “no” is the most motivated to say yes. You monetize dead leads, your approval rate climbs, you pay higher affiliate bounties, and the flywheel spins.

But the real unlock is the LLM.

As we wrote in a recent Free Toaster edition, 200 million people already come to ChatGPT every month to ask financial questions. With Plaid now fully integrated, those questions aren’t abstract anymore — they’re grounded in real transaction data. Perplexity built the same thing. Credit Karma is plugging approval odds directly into the ChatGPT experience.

Think about what that means: a user asks about credit cards. ChatGPT reviews their actual spending via Plaid, identifies $8,000 in annual United flight spend, surfaces the United card, checks approval odds through Credit Karma, and prompts them to apply. Product discovery, underwriting match, and conversion funnel — all inside a chat window.

That’s the distribution channel CFU has been waiting for. Not a lender begging you to log into your bank. An AI you’ve already handed your financial life to, pointing you toward better rates and smarter products. The data plumbing for cash flow underwriting is getting laid down by consumers themselves (voluntarily) because the more context they give the model, the better it serves them.

We called it the personal finance super app. The flywheel is already rolling: more data makes smarter recommendations, smarter recommendations build more trust, more trust unlocks more data. At 200 million MAUs, that flywheel has serious momentum.

The open question isn’t whether CFU gets mass distribution anymore. It’s who owns the consumer relationship when it does — ChatGPT, your bank’s AI layer, Credit Karma’s approval odds infrastructure, or someone we haven’t met yet.

But the path from “I’m asking my AI about groceries” to “I’m taking out a better loan” is shorter than most people think. The natural next move after understanding your money is optimizing it. And optimizing it is exactly what lenders sell.

[Check out our full-length editorial here]

Marqeta’s State of Credit: Credit Is Now a Portfolio Consumers Assemble Themselves — and Most Issuers Aren’t Built For It

Marqeta dropped its 2026 State of Credit Report, a survey of 4,000 consumers and 1,000 SMBs across the US and UK, and the through-line is one every growth and product lead should internalize: customers no longer “have” a credit product, they assemble a portfolio of them and switch by transaction. 85% of consumers weigh multiple factors before picking a payment method, 59% used both debit and credit in the last 90 days, and 79% of BNPL users keep using BNPL even when they have a card. BNPL isn’t cannibalizing cards, it’s a parallel rail people toggle into on purpose.

Here’s the why for operators. The report quantifies the single most under-exploited leak in the funnel, the decline. 63% of denied card applicants were never offered an alternative product, yet 60% would have taken a credit-builder, and 76% of denied credit card applicants surveyed would undergo a credit check to upgrade to revolving credit when their profile is ready.

That’s a population you already paid CAC to acquire and then showed the door. The strategic answer Marqeta is selling, “flexible credentials” (one card that flips between debit, credit, and BNPL) plus co-brand-debit-with-BNPL, is really a retention-and-graduation play: keep the relationship through the credit transition instead of re-acquiring the customer later at full price. 48% of 18 to 44s want flexible credentials, rising to 71% among multi-card holders, and the demand skews toward people most comfortable with non-bank providers, which is exactly where a Marqeta-powered issuer wants the wind blowing. [Business Wire] [Marqeta]

The caveat: this is research from a company that profits if you believe it, and it’s a press release, not a filing. But the declined-applicant numbers are the kind of thing you can validate against your own data this week.

Sponsored by New Market Growth

New Market Growth helps lenders build and scale affiliate marketing programs on channels like Credit Karma, Experian Marketplace, Lending Tree, Bankrate, Credible, and many more. NMG clients spend $50-$100MM per year in affiliate channels, and the founding team (one of whom is Free Toaster co-founder Carlos Caro), have advised in excess of 50 lenders over the course of their corporate and agency careers.

If you’re a Free Toaster Reader at a lender that spends over $500K per month in affiliate marketing, we’re offering a free, 90-minute audit of your affiliate marketing program. After research we’ll conduct on our side, we’ll book time to share the strengths, weaknesses, and opportunities we observe in your program.

Outside eyes could help unlock the growth you’re looking for in H2 2026.

Email carlos@newmarketgrowth.com with subject line “90-minute audit” and we’ll contact you to get the preliminary information we need to get to work.

Sezzle Expands the Super App: New Rewards Currency, Pay-in-5, and AI Across the Stack

Sezzle pushed its super-app strategy further: the Earn tab now carries a new rewards currency (Sezzle Points, earned via cashback, surveys, and receipts, redeemable for gift cards) alongside AI-powered shopping. The distribution data point worth stealing is Pay-in-5, a no-cost five-installment option where April average order values ran 44% higher than Pay-in-4, a direct lever on basket size and merchant economics, not just a UX tweak. Sezzle is running Klarna’s playbook, converting a one-and-done BNPL checkout into a recurring engagement surface . [GlobeNewswire]

Fintech Resurgence. The Next Cycle Belongs to Operators Who Own Distribution and the Balance Sheet

BCG and FT Partners put out their Global Fintech Report 2026, “From Recovery to Resurgence,” and it’s a must-read. The top line: sector revenue hit $504B in 2025, up 22% year over year, growing roughly three times faster than incumbent financial institutions. The bigger shift is quality of growth. Among the 85 largest public fintechs, 74% are now profitable, and average EBITDA margins climbed 400bps to 20%. The “growth at all costs” era is closed. Capital is being priced on durable unit economics, not GMV.

Here is the why for operators, and it runs across distribution, underwriting, and the balance sheet.

First, distribution is being rewired by AI.

The report calls out the move from search to answers, generative engines and AI overviews intercepting intent before a user ever reaches a comparison page, plus agentic commerce where AI assistants execute checkout. For any lender that buys leads or ranks for “best personal loan,” this is the affiliate funnel eroding in real time. The defensible play is owning the customer relationship and the re-engagement loop, not renting clicks.

Second, the bank-charter wave.

Charter applications and approvals jumped more than fivefold, with names like Revolut, Nubank, and crypto-native players pursuing charters and banking licenses. Owning the charter means owning deposits, cheaper funding, and the ability to keep lending economics in house instead of renting a sponsor bank. That is a direct lever on loan margins.

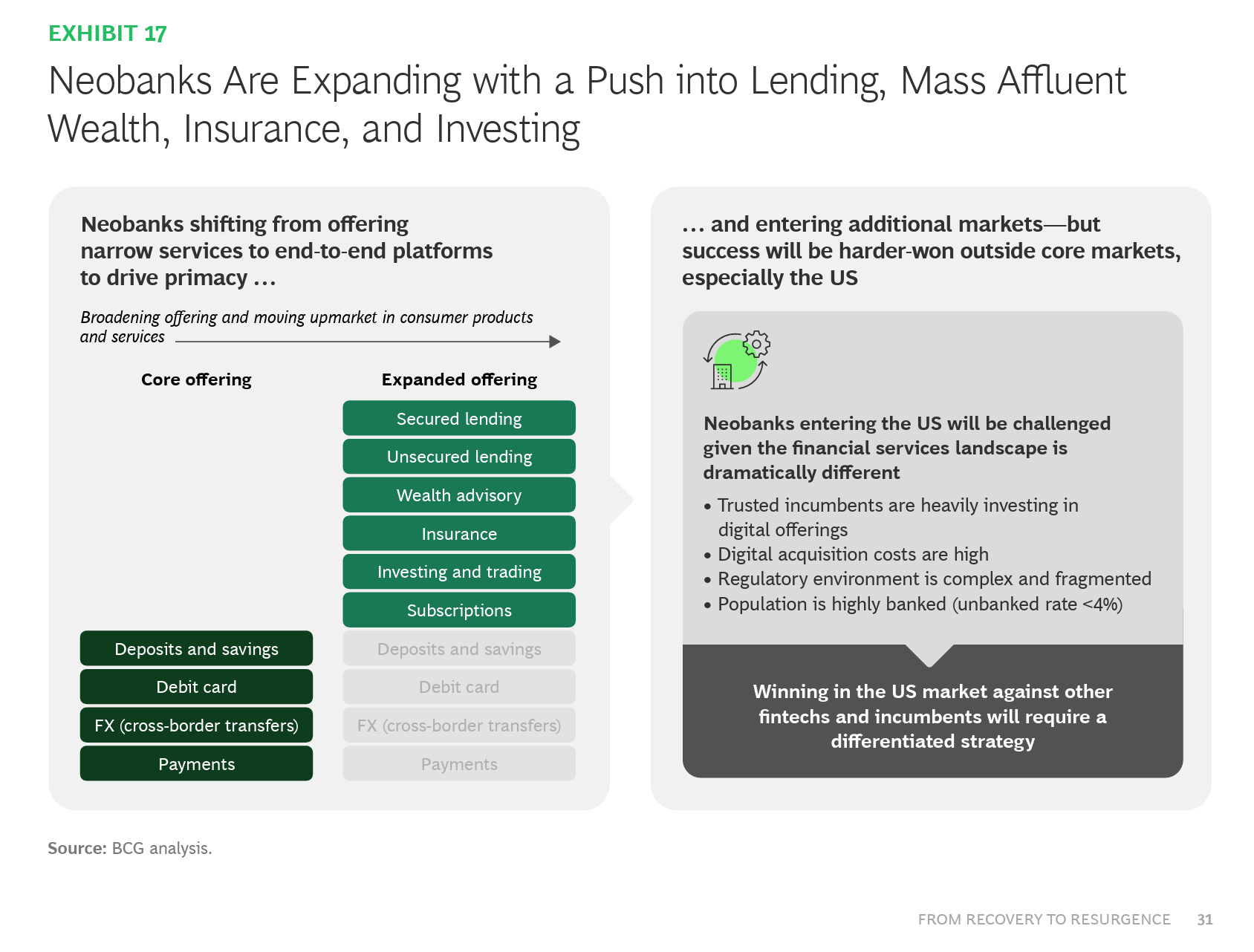

Third, neobanks are graduating into credit.

The scaled digital banks are pushing past deposits and interchange into lending, where the real net interest margin lives, which puts them on a collision course with incumbent card issuers on exactly the underwriting and acquisition terrain this audience operates in. M&A is consolidating the winners, deal volume rose to 659 transactions, with scaled fintechs like Capital One buying their way into capability and reach.

The strategic takeaway is consistent across the report: revenue resurgence is real, but the operators who compound through the next cycle are the ones who control distribution as AI eats search and who control the capital and the charter behind their loans. [BCG + FT Partners]

Please support our Newsletter by sharing this edition with a colleague!

And, consider checking out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Spot something worth sharing with your team? Drop this week’s edition in their inbox.

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.