With Plaid Integration, ChatGPT is now a distribution channel for personal finance.

Plus a Free Toaster Conference Exclusive for Publishers and Lenders

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

ChatGPT is now a distribution channel for personal finance. OpenAI launched a feature that allows users to connect their bank accounts using Plaid. They also partnered with Intuit to integrate tools like Credit Karma’s approval odds. This means ChatGPT can review a user's actual spending data, determine their approval odds, and recommend personalized financial products.

We explore how this new setup impacts traditional search traffic and affiliate sites like NerdWallet, and how this changes the affiliate marketing landscape in the lending industry.

Plus, we drop details on our upcoming September event in San Francisco, the Affiliate Marketing Summit For Lenders.

Lots to break down. Let’s get toasting!

Carlos Caro, Founder at NMG, Co-Founder of The Free Toaster

Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please forward this to 1 of your colleagues!

Toaster Exclusive Event

Learn more at: events.thefreetoaster.com

This event is Proudly Sponsored by Experian & MoneyLion

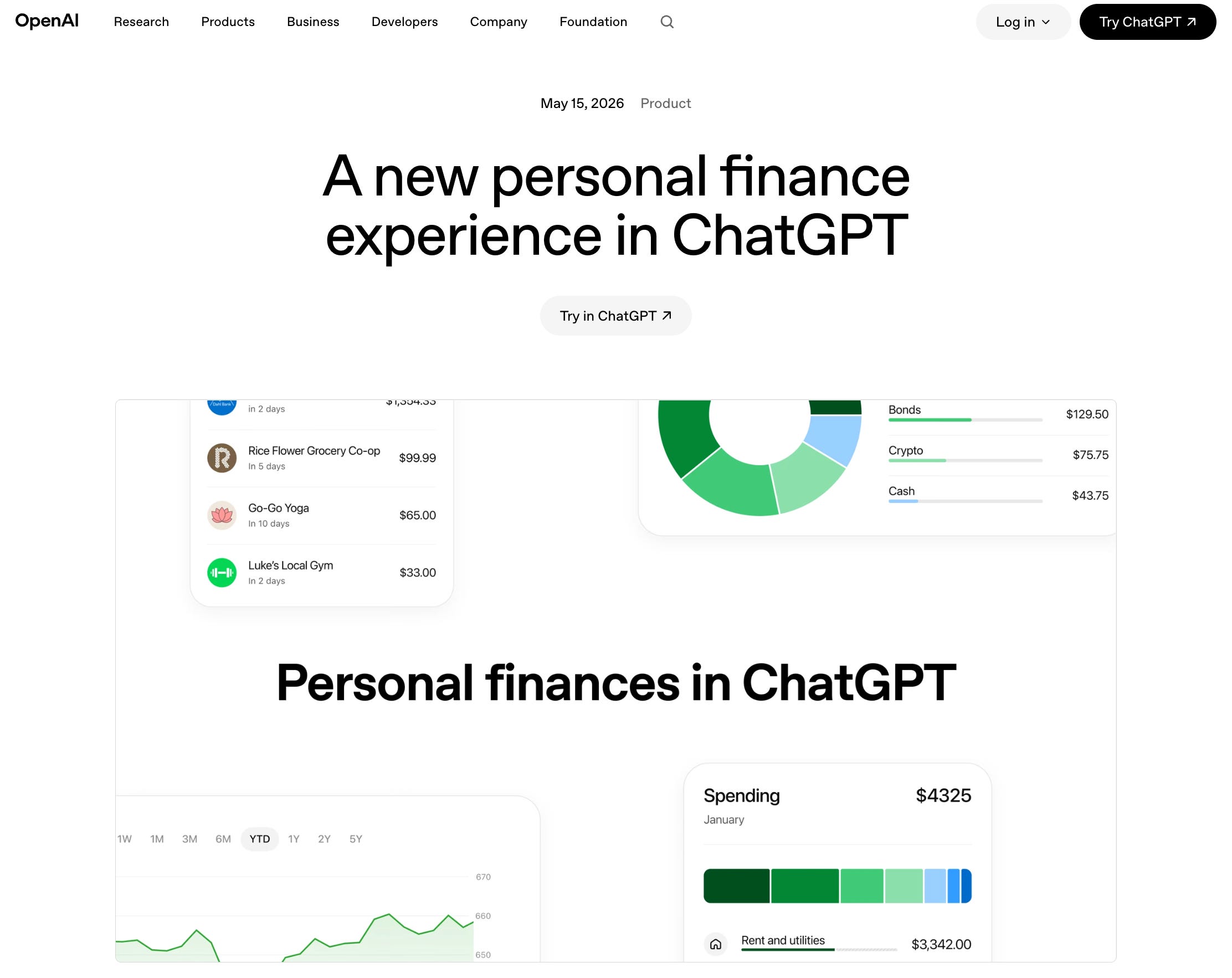

ChatGPT Is Now a Distribution Channel For Financial Products

OpenAI launched a personal finance experience inside ChatGPT.

Perplexity did a similar thing a month earlier.

This marks the early innings of consumer attention shifting away from Google and the traditional affiliate listing pages and into the LLMs (for financial products).

What Actually Happened

200 million people already come to ChatGPT every month to ask financial questions.

Previously, ChatGPT was answering personal finance questions in the abstract. It would give high-level answers loaded with assumptions, or it forced the customers to answer a pile of detailed questions.

Now, with Plaid fully integrated into ChatGPT, it answers those questions based on the customer’s real financial data.

How it works (for users in the “Pro” tier):

Connect bank accounts through Plaid

ChatGPT gets read access to balances, transactions, investments, and liabilities

Users get a financial dashboard, the ability to ask freeform questions, and personalized product recommendations built on their financial profile

Perplexity built the same thing with Plaid, while also layering in investment-grade data from FactSet, Coinbase, Nasdaq, and S&P Global.

ChatGPT and Perplexity both seem to appreciate the power of answering personal finance questions for their customers in the specific, not just the abstract.

Intuit’s Role In All Of This

In November 2025, Intuit announced a new $100M+ multi-year contract designed to accelerate its AI-driven expert platform strategy. TurboTax, Credit Karma, QuickBooks, and Mailchimp now live directly inside the ChatGPT experience.

Intuit’s CEO Sasan Goodarzi said: “For us, it doesn’t matter whether a customer comes directly to using our platform or we are where they are within an app, in this case ChatGPT.”

From OpenAI’s perspective, one of the unique things Credit Karma brings to the table is their approval odds models. The ability to tell a user, based on their real credit profile, how likely they are to get approved for a given card, loan, or mortgage. That’s roughly 2 decades of data infrastructure across 130MM+ members.

Imagine this: A user asks about credit cards. ChatGPT reviews their spending (enabled through the Plaid link), identifies $8,000 in annual United flight spend, surfaces the United card, checks approval odds through Credit Karma, and prompts them to apply. No new tab. No search results page.

That’s product discovery, validation of an underwriting match, and (potentially) a conversion funnel. And this can happen in a few key strokes inside ChatGPT.

Who Should Feel Threatened?

Traditional content affiliates should be very worried.

Specifically, sites that rank for terms “best travel credit card 2025,” serve generic display ads, and collect referral fees when users click through and apply.

That static webpage listicle couldn’t possibly know you spent $8,000 on flying on United last year. ChatGPT does. And, going further, it can tell you how many incremental rewards you’ll earn by moving your spend and confirm that the issuer will approve you if you apply.

Sites like NerdWallet have great content. But, OpenAI already consumed that data. What sites like NerdWallet don’t have is approval odds models with the scale and fidelity of a giant like Credit Karma.

Consumers chase convenience and utility.

The utility of an adviser with the context of Plaid’s transaction data, the certainty layer of Credit Karma’s approval odds, and the intelligence of OpenAI’s best foundational models is hard to beat.

Game, set, match for the LLMs. RIP Google’s pile of blue links.

The New Competitive Landscape

Credit Karma’s position is strong.

They are in a position to be the largest-scale approval odds provider for the ChatGPT ecosystem. OpenAI has no incentive to replicate that in-house. Building credit bureau & lender relationships, selecting attributes, and predicting approval odds across dozens of lenders is two decades of infrastructure work.

Experian’s position is also very interesting.

While a smaller-scale consumer marketplace than Karma (at least for now), they’re a credit bureau, too. So while Karma has to worry (at least a little bit) about existential risk tied to their credit bureau relationships, Experian can control their destiny across the value-chain.

OpenAI will happily outsource the challenge of predicting approval odds, especially knowing the total market for affiliate marketing spend in consumer lending is in the ballpark of $6B per year. That’s peanuts for a giant like OpenAI.

There’s an opening for the banks, though.

Karma’s models aren’t perfect. Based on their relationship with lenders & the bureaus, they can assert with high confidence that you’ll be approved, but they don’t guarantee it with 100% certainty. (To their credit through, they’ve gone as far as to offer consumers up to $50 when they get declined on offers with the Credit Karma Guarantee badge).

If a lender like Wells Fargo or Capital One built a direct integration with OpenAI, they could in theory deliver 100% certainty, something the likes of Karma and Experian would have a very hard time replicating. (And, to be clear, we’re not saying that 100% certainty is easy for the banks, it’s just that they have an advantage over the affiliates).

That’s because the lender could run their underwriting model with their own decisioning data in the background.

The affiliate marketplaces and the lenders have slightly different credit bureau datasets and they pull the data from the bureaus at different points in time, and those nuances could make the difference between ChatGPT saying “your chances for getting this product are really, really great” and “I can 100% guarantee it.” That’s a subtle, but important difference in consumer lending.

As the LLM surface proves it ability to secure consumer attention and transaction flow to lending products, OpenAI will have to decide if they want their approval odds coming through affiliate marketplaces like Credit Karma or Experian, directly from the lenders, or some combination of the two.

If OpenAI builds an open interface where any lender can plug in their own underwriting signal, the approval odds layer becomes a infrastructure race between institutions. And OpenAI will arbitrate whose signal it trusts most.

I’m guessing that’s something the executives at Credit Karma, Experian, and the other organizations positioned to play this role (companies like Free Toaster sponsor Spinwheel) are thinking about.

What Distribution Channels Survive The LLM Disruption

Direct mail is off-line. The AI overloads won’t be controlling what envelopes land in your inbox anytime soon. This will continue to be a bread and butter channel.

Social is structurally separate. It’s entertainment and education oriented. People don’t go to TikTok to ask financial questions. The issue with social is that approval rates tend to be lower due to the lack of credit-bureau-based targeting at the top of the funnel.

Podcast, YouTube, out-of-home. Owned media channels will stay as powerful mediums to get brand messages across, but will be tough to crack as direct-response channels because they lack credit bureau data signal at the marketing stage.

Google-based search intent will be swallowed whole. That slice of attention maps almost perfectly onto what ChatGPT, Claude, Perplexity, and the LLMs are now racing to capture.

Closing Thoughts

The LLMs are in the early days of constructing a personal finance super app.

The super app will accumulate context across your cards, deposit accounts, savings accounts, and use it to inform the answer to every question.

Further, because people will arm these super apps with personal context, financial goals, and lifestyle preferences, the super apps will do an amazing job delivering personalized, proactive advice that will create utility for the customer.

We have a classic data-led product flywheel.

ChatGPT gets smarter and more useful as you connect more data and context.

Smarter recommendations build more trust and more users. More trust and more users unlocks more data. At 200 million monthly active users, that product flywheel is already rolling down the hill.

Plaid unlocks the transaction layer. Credit Karma (and other data-forward marketplaces like Experian) could plug in the approval odds layer. Those are some of the foundational layers of a personal finance super app.

And more are coming, because we still need to solve for fraud, identity, and transaction processing at scale to make the most out of the LLM surface for personal finance.

The organizations that notice this, and can build a business owning a layer inside of the LLM surfaces, will have compounding advantages over time.

The ones waiting to see how it plays may be left fighting over the consumer attention that doesn’t migrate to the LLMs. Or, they’ll have a heck of a time elbowing their way in when they realize they’re late to the party.

The questions for every consumer lender and publisher right now: Do you have proprietary data, a differentiated model asset, or a product or service worth plugging into the personal finance super app? Or, do you have the ability to create this super app yourself?

It’s not a given that OpenAI, Perplexity, or Anthropic will earn the trust of the consumer as the personal finance super app.

How many people will hand ChatGPT the user name and password to their bank accounts and/or their Credit Karma or Experian accounts?

That’s a big unknown right now.

But the answer to that question over the next 12-24 months could materially change the landscape of consumer lending marketplaces.

[OpenAI] [Perplexity]

Sponsored by Spinwheel

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

News Pod #18 - NerdWallet’s Q1’26 Earnings: Why Is The Stock Down 30%

Catch us on Apple Podcasts, Spotify, Substack, or your favorite player.

Please support our Newsletter by sharing this edition with a colleague!

And, consider checking out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(SEO) Google Search as you know it is over (TechCrunch)

(SEO) Google Search is getting its biggest changes ever (The Verge)

(Agentic Commerce) Would you let robots spend your money? Google is betting on it (The Verge)

(BNPL) Affirm seeks bank apps to build its BNPL empire (American Banker)

(BNPL) Google Embeds Klarna BNPL Into Gemini AI Conversations (PYMNTS)

(Banks) Fintech firm Mercury hits $5.2 billion valuation after funding round, up 49% in 14 months (CNBC)

Spot something worth sharing with your team? Drop this week’s edition in their inbox.

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.