Apple Just Put BNPL Into 65 Million Apple Pay Wallets

With iOS 26, Apple Pay now surfaces installment options at in-store checkout, turning every transaction into a lending decision for issuers and BNPL providers alike.

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

Apple is aggressively moving buy-now, pay-later into the mainstream by embedding one-tap installments directly into the iPhone’s payment sheet for in-store use. This disruption is part of a broader shift in consumer finance, as Upstart expands into revolving credit with Cash Line and Bank of America democratizes its rewards program by slashing minimum balance requirements. Also, AI is rapidly reshaping the industry’s backend, from Intuit and Anthropic’s push into automated accounting to Experian’s new ChatGPT app that streamlines the insurance shopping experience.

Lots to break down. Let’s get toasting!

— Carlos Caro, Founder at New Market Growth

— Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please share our Newsletter in your internal Slack channels!

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

Apple Pay Pushes BNPL To Offline (In-Store) Transactions

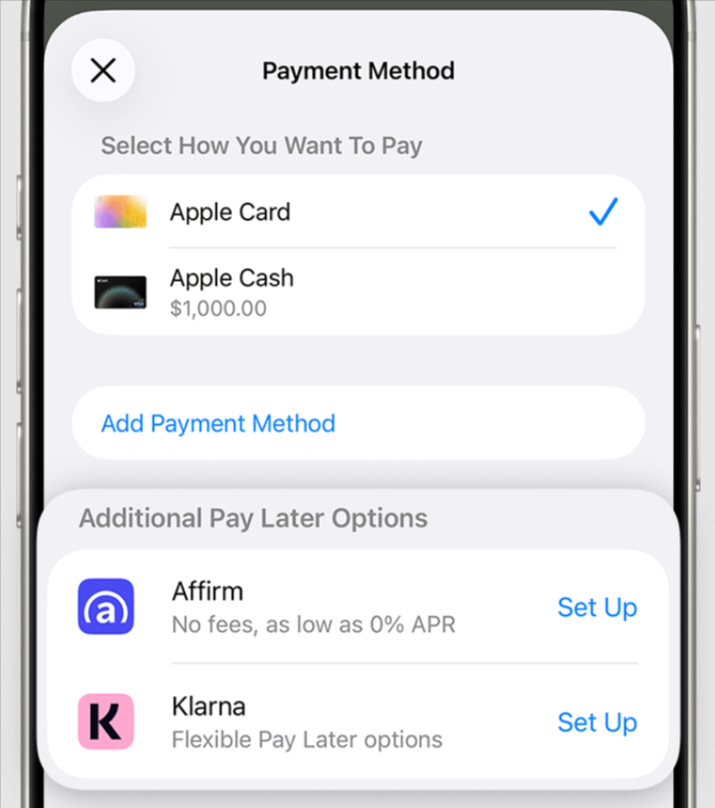

Apple is now pushing the ability for Apple Pay users to pay with installments at the physical register, not just online and in apps. With iOS 26, installment options show up right inside the Apple Pay payment sheet when you tap to pay in store. What used to require opening a separate app or converting a purchase after the fact is now a one-tap decision at the moment of payment. Apple is not lending directly. Loans come from participating providers including Affirm, Klarna, Citi, and Synchrony. The feature is also rolling out internationally across Canada, the UK, France, Italy, Spain, Denmark, and Sweden. (Apple Support) (PYMNTS)

How It Actually Works

You’re at the checkout register. You double-click your iPhone’s side button and your Apple Pay card appears. If your linked card supports installments, you’ll now see two options: Pay In Full and Pay Later.

Tap Pay Later and you’re shown the installment plans available from your card issuer or BNPL provider, including terms, payment schedule, and any conditions. Select a plan, tap Agree & Continue, confirm with Face ID, and hold your phone to the reader. Done.

You can even set up an installment plan after your purchase. Complete the transaction normally, and when the notification comes in, follow the prompts to convert it to a plan retroactively.

Previously, you loaded your card, made the purchase, and then maybe went to Affirm or your issuer’s app to convert it later. Now the installment option is right there at the point of decision. The friction is gone.

Toaster’s Take

This isn’t any ‘ole product launch. Now lenders have to compete for transactions on the basis of rewards AND their BNPL options.

Buy now, pay later started niche. It expanded online. It became a major category with Affirm. Now it’s embedded at the operating system level by Apple. That signals that BNPL has reached the mainstream adoption curve, and if you’re a card issuer not offering installments, you need to stop and think about what you might be missing by sitting out.

Offline is the Real Unlock

BNPL has historically skewed online, but roughly 3 out of every 4 U.S. retail dollars are still spent in store. E-commerce accounted for just 16.4% of total U.S. retail sales in Q3 2025, per the U.S. Census Bureau. Meanwhile, Apple Pay already captures about 54% of in-store mobile wallet transactions and accounted for 10.2% of eligible in-store purchases in 2025 according to a PYMNTS Intelligence study of 3,339 U.S. consumers. By putting installment options at the physical register, Apple is expanding BNPL’s addressable market in a big way. This may be the bigger story: not that Apple supports installments, but that it’s pushing them into the ~83% of retail that happens offline.

The Wallet Becomes a Marketplace

Apple chose not to give exclusivity to a single BNPL provider. Affirm, Klarna, Citi, and Synchrony are all visible inside the wallet, creating competitive territory at the moment of payment. Think of it like how issuers compete for new accounts inside Credit Karma, except this marketplace lives one tap away from every transaction. It’s not enough to just integrate. Winning placement inside the wallet becomes a real operational focus. We wouldn’t be surprised if lenders eventually need to dedicate teams to manage and grow their Apple Pay wallet share (if that’s not happening already).

Acquisition is No Longer Episodic

Previously, issuers competed on rewards, perks, and credit limits. Customer acquisition happened once in a while. Someone opened a card once a year, maybe. Now every single checkout is a decision moment. Apple puts “pay in full” and “pay later” side by side. The user chooses every time. Fighting for share of wallet might have just hit its Apple Pay BNPL moment.

The Bottom Line

More than half of U.S. smartphone users are on iPhones and an estimated 65.6 million people in the U.S. use Apple Pay. Google Pay supports some BNPL options through partners, but hasn’t embedded a native installment experience as deeply as Apple has. If this gains traction, expect Google to follow and wallet-level installment marketplaces to become standard.

We keep seeing the signs. Issuers may no longer be able to ignore offering BNPL on their card products. Not when Apple puts it one tap away on every iPhone.

The Free Toaster Podcast takes the biggest fintech, credit, and payments stories of the week and breaks down what they mean for growth, distribution, and product strategy. If you read the newsletter, this is the conversation behind it.

Listen on Apple Podcasts, Spotify, Substack, or wherever you get your podcasts.

Be sure to check out our latest pod!

(And if you have a strong opinion on anything in today’s Edition and would like to be on the show - we record at 12pm ET on Fridays - let us know!)

Upstart Announces Cash Line, Bringing Always-On Credit to Millions of Americans

Upstart is launching Cash Line, a revolving line of credit intended to provide consumers with persistent access to funds. As an AI-based lending marketplace that matches borrowers with over 100 banks and credit unions, the company is positioning this product as a more predictable alternative to traditional cash advance apps. The service offers a minimum credit limit of $200 for approved users, with the potential to reach $5,000. Upstart also includes a feature called Rest Mode to give borrowers more flexibility over their repayment schedules. Users pay a $10 monthly membership fee for credit lines up to $500, while larger draws incur an APR ranging from 5% to 36%. Although a full release is scheduled for later in 2026, the company is currently opening a waitlist for a beta version of the platform. This move shifts the company further into the revolving credit space, moving beyond its existing focus on personal, auto, and home equity loans. (Upstart)

Toaster Readers: Is this innovative or the 10th rendition of this in the marketplace? If you have a strong POV we’d love to have you on the Podcast to discuss. Reply to this email and let us know.

New BofA Rewards™ Program to Reach Millions More Clients with Expanded Benefits

Bank of America is replacing its current rewards structure with BofA Rewards, a loyalty program that removes previous balance requirements for anyone with a personal checking account. This financial institution, which provides banking and investment services to roughly 70 million clients, previously required a $20,000 minimum balance for similar perks. Starting May 27, about 30 million additional customers qualify to enroll and access benefits like credit card bonuses and cash back deals. Depending on how much a member uses the program and their specific tier, the bank estimated the annual value of these perks ranges from $150 to $4,000. Higher-tier members also receive credits for streaming services and access to events related to travel or motorsports. The company also updated its mobile app to help users track and activate these offers more easily. By shifting to this model, Bank of America attempts to capture a wider range of customers regardless of their current account balances. (Bank of America)

Want To Reach Our Readers In Person?

The Free Toaster is betting big on live events in 2026.

If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. Think coffee meetups, lunches, dinners, 1-day events, golf outings, wine tastings.

Our events team can help you bring it to life. Contact amanda@thefreetoaster.com for more information.

Intuit and Anthropic Partner to Bring Trusted Financial Intelligence and Custom AI Agents to Consumers and Businesses

Intuit, the financial technology company that operates TurboTax and QuickBooks, is partnering with AI firm Anthropic to integrate automated agents into its software for mid-sized businesses. This multi-year agreement allows these companies to use the Claude language model to build agents for specific tasks like accounting and compliance workflows. A restaurant owner could potentially use the system to identify variances in profit margins by connecting sales data with payroll records. On the consumer side, Intuit is linking its financial data with Claude so users can estimate tax refunds or create invoices directly within Anthropic’s apps. Intuit is also providing Claude Code to its own engineers to speed up software development. While the companies describe the tools as a significant shift in capability, they noted that the systems rely on Intuit’s existing data and security infrastructure. These features are expected to begin rolling out in spring 2026. This move suggests that the future of personal finance might involve handing off the more repetitive aspects of bookkeeping to automated systems. (Intuit)

Experian Launches Insurance Marketplace App on ChatGPT

Experian launched its Insurance Marketplace app on ChatGPT, providing a way for people to shop for auto insurance through a chat interface. This global data and technology company, which handles credit reporting and financial services, aims to replace traditional forms with a conversation that allows users to compare rates from 37 carriers. Instead of clicking through various websites, users provide a ZIP code to see different coverage options and estimated prices. The company states that this process can help consumers find savings that sometimes exceed $1,000 per year. This move is part of a broader plan to move financial decision-making into AI environments. While users can explore prices in the chat, they must still go to the company website to finish a personalized quote. This setup attempts to simplify insurance shopping by using a bot to organize information that is usually spread across static pages. (Experian)

TransUnion 2026 Originations Forecast Shows Continued Positive Momentum Amidst Moderate Expansion

TransUnion, a global firm that collects and analyzes consumer credit data for businesses, expects credit originations to grow at a moderate pace through 2026. While the 2025 spike in auto loans will likely slow down as federal EV tax credits expire, mortgage and personal loans are taking over as the primary drivers of growth. Homeowners are seeing more options as interest rates move lower, which improved affordability and led to a sixth straight quarter of growth for home equity products. In the personal loan market, originations reached 7.2 million as fintech lenders took a 42% share of the sector. Despite these high volumes, TransUnion reports that lenders are staying cautious with risk because delinquency rates rose across several categories. Consumers are still using credit regularly, with total card balances reaching a substantial $1.15 trillion while the growth rate begins to level off. The data suggests the credit market is returning to traditional patterns following a period of high inflation. (TransUnion)

GoCardless Introduces AI-Native Tool for Businesses to Communicate With the Platform in Natural Language

GoCardless, a bank payment company that specializes in direct debit and instant payment processing, released its Model Context Protocol to help developers interact with its platform using natural language. This tool allows businesses to use large language models to communicate with the system, potentially reducing the time required to integrate the service into their own websites. Instead of manually searching through technical documentation, a user like a gym owner can ask the AI for specific information, such as which payments are overdue. The company notes that this setup simplifies workflows today while providing a foundation for future AI agents to handle transactions independently. This update follows a pattern of the firm using machine learning to handle failure rates and identify high-risk transactions. One of its existing tools, Success+, currently recovers an average of 70% of payments that do not go through on the first attempt. It is an interesting shift toward making financial back-ends more approachable through conversational interfaces. (GoCardless)

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to accelerate your affiliate marketing? Chat with New Market Growth

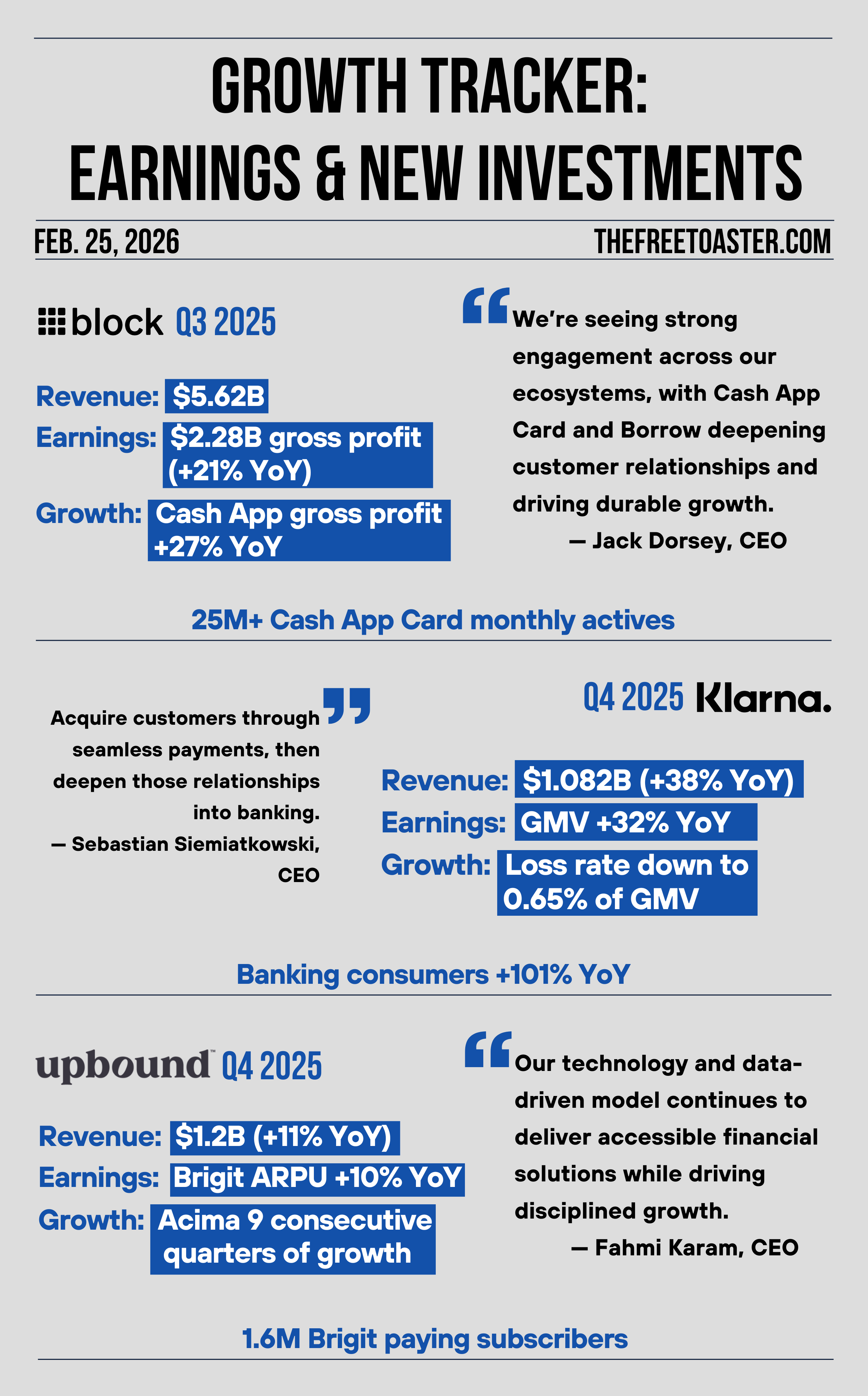

Sources: Block, Klarna, Upbound

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(Partnership) Major League Soccer Names Chime Official Retail Banking, Credit Card, and Debit Card Partner (MLS)

(Banking) Equifax Delivers Optimal Path™ Directly to U.S. Consumers via the myEquifax Mobile App (Equifax)

(Legal) Baltimore Sues Fintech Company Dave Over ExtraCash Overdraft Product (JD Supra)

(Policy) Kansas Bankers Launch Campaign Against Marshall-Backed Credit Card Legislation (KCTV5)

(Fintech) Stripe‘s Bridge Secures Conditional OCC Approval For National Trust Bank Charter (Payments Dive)

(Lending) DailyPay Upsizes Secured Credit Facility To $960 Million (PR Newswire)

(Crypto) Quantoz Partners With Visa To Make Stablecoins Spendable (Quantoz)

(Payments) Desert Financial Credit Union Partners With Alacriti To Unify Instant And Legacy Payments (Alacriti)

(Banking) Backbase And Plaid Partner To Bring Open Finance To AI-Powered Banking (Backbase)

(Payments) Britain Plots Visa Rival Over Fears Trump Could Pull The Plug On Payments (The Guardian)

(Partnership) Visa Renews Partnership Across Red Bull Formula One Teams (Visa)

(Finclusion) Ericsson And Mastercard Enhance Global Digital Money Movement And Accelerate Digital Financial Inclusion (Mastercard)

(Retail) eBay Partners With TrueLayer To Offer Pay By Bank At Checkout (TrueLayer)

(M&A) Grab Accelerates Financial Services Roadmap With Acquisition Of Digital Investing Platform, Stash Financial, Inc. (Grab)

(Banking) Marshall Community Credit Union Selects Mahalo Banking To Enhance Digital Agility (Business Wire)

(Cybersecurity) Cloudflare And Mastercard Partner To Extend Comprehensive Cyber Defense Across Critical Infrastructure And Small Businesses (Mastercard)

(Lending) Credit Unions Warm Up To Small-Dollar Loans, Challenging EWA (American Banker)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/apple-just-put-bnpl-into-65-million

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.