Wells Fargo Books 631,000 New Credit Card Accounts

Plus, JPMorgan Chase and Citi report earnings, JetBlue’s new travel perks, and Atlas’s $420 million pivot to the ultrawealthy.

Hey Toaster Readers,

This week is sponsored by our friends at Bulldog Media Group.

Wells Fargo is reporting a massive surge in new credit card accounts, but there is a catch: purchase volume isn't keeping pace, and a reporting change for co-branded cards is muddying the waters. JPMorgan Chase and Citi are posting major profit jumps , JetBlue and Barclays are overhauling premium card benefits , and Atlas is pivoting to a $999 billionaire charge card after its previous debit startup collapsed.

Lots to break down. Let’s get toasting!

Carlos Caro, Founder at NMG, Co-Founder of The Free Toaster

Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please share our Newsletter or Podcast with 1 of your colleagues!

Wells Fargo Posts $5.3B Q1 Profit as Loan Growth Hits $1 Trillion Milestone

Wells Fargo posted $21.4 billion in revenue for Q1 2026, up 6% year-over-year, with net income of $5.3 billion. The loan book crossed $1 trillion in period-end balances, with commercial and industrial lending the primary growth driver, up 23% year-over-year. Consumer loans held relatively flat. Deposits were up 7%, and average deposit costs continued falling, down 15 basis points from the same period last year. Consumer loans grew modestly, up about 4% year-over-year, with auto originations more than doubling and credit card balances up 5%. Card fees climbed 9% on higher merchant processing and debit interchange income. Headcount fell 7%, which management tied to ongoing efficiency initiatives, while advertising and promotion spend jumped over 100% year-over-year.

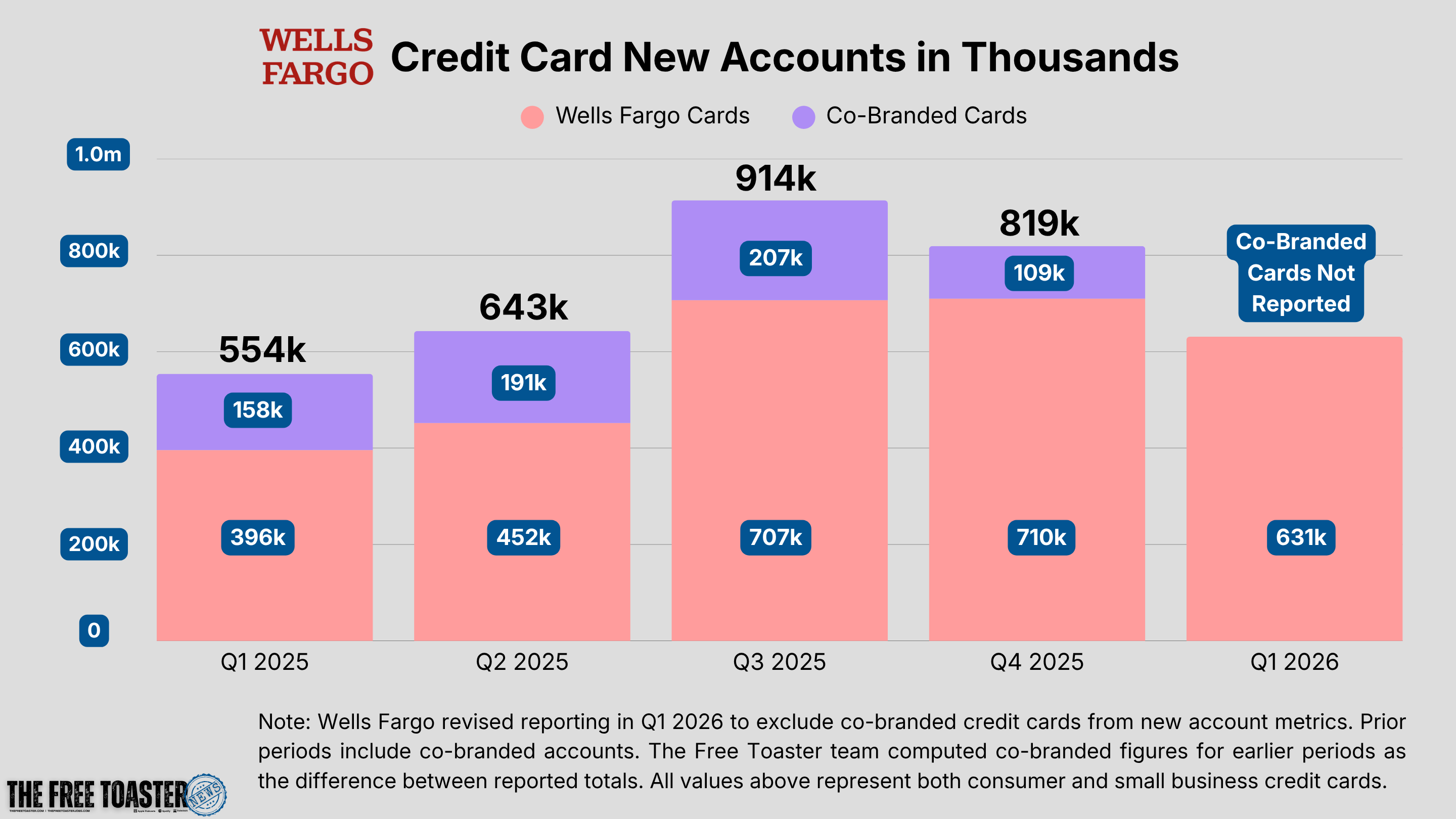

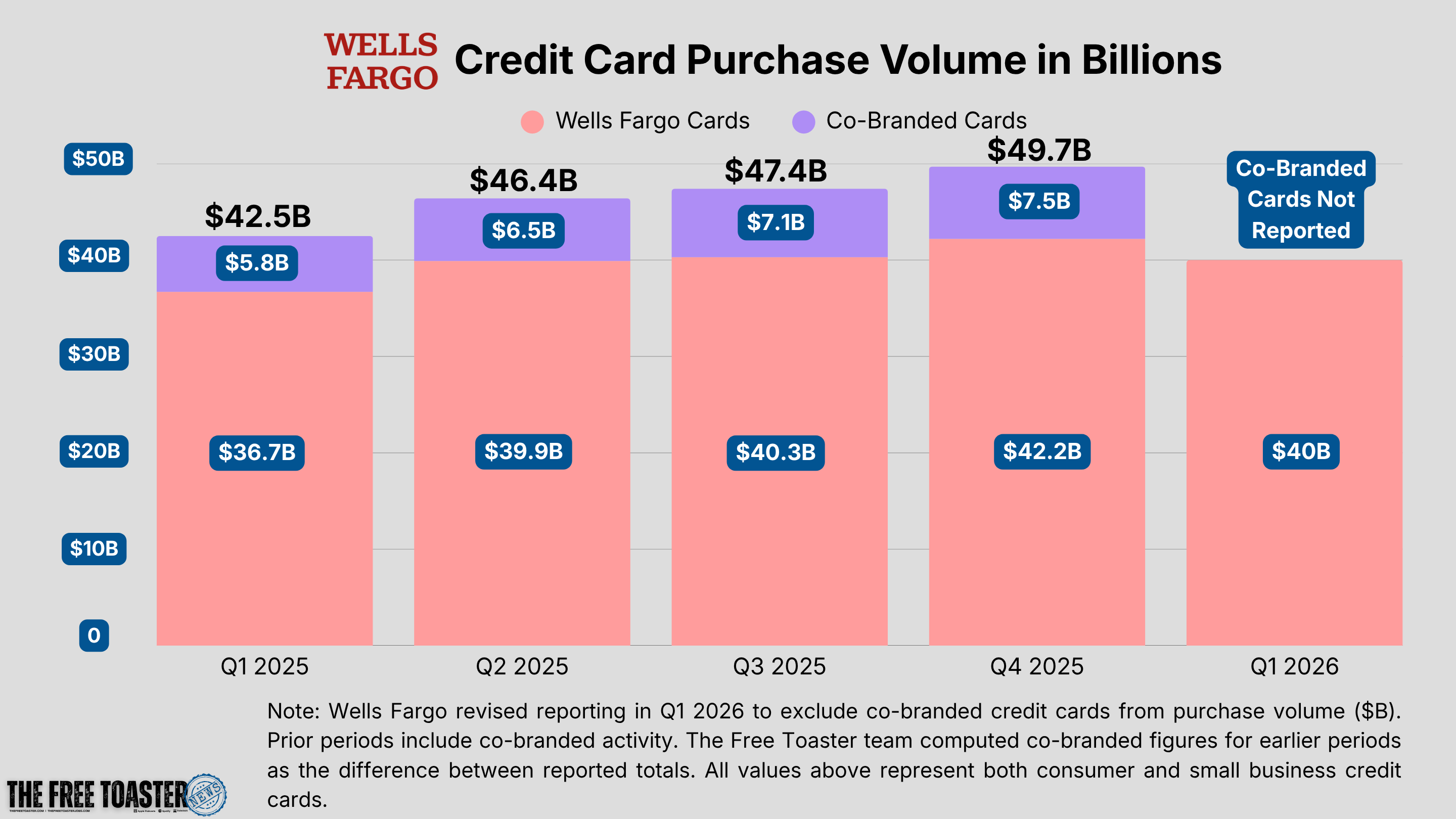

The more interesting story for fintech operators is what’s happening in Consumer Banking. Wells opened 631,000 new credit card accounts in Q1 2026, nearly 60% more than the 396,000 opened in Q1 2025. Purchase volume also climbed, reaching $40.0 billion versus $36.7 billion a year prior. Both figures cover combined consumer and small business customer activity. Worth flagging: Wells revised its credit card metrics this quarter to exclude co-branded cards, with prior periods restated to match. That means the growth figure reflects proprietary card activity only, which is worth keeping in mind before reading too much into the year-over-year jump. (Wells Fargo)

Toaster’s Take

Account growth of that magnitude runs far above the typical 5-10% range for large issuers. That alone is worth a second look. But the bigger puzzle is what isn’t moving alongside it. Purchase volume grew modestly year-over-year. Balances don’t show a similar spike. Delinquencies are stable. The natural question: if these are high-quality acquisitions, why isn’t spend following?

A few possible explanations:

One is churn. The metric here is new accounts, not net new accounts. Wells could be adding aggressively on one end while losing or closing accounts on the other. Another is acquisition mix. If the funnel has shifted toward lower-spend or promotional-driven signups, you’d get exactly this pattern: strong account numbers, weak purchase volume. A third is portfolio reshuffling. Wells may be migrating customers from discontinued products into new ones, which counts as new accounts in the data without necessarily representing new customers.

The co-branded card exclusion adds another layer. Wells revised its credit card metrics this quarter to exclude co-branded cards, with prior periods restated to match. That change affects how the year-over-year growth reads, and it’s worth keeping in mind when interpreting the magnitude of the spike.

The new card launches don’t resolve the question either. Wells rolled out a Private Bank Visa Infinite and Autograph Premier this quarter, both targeting high-income and private banking clients through tight underwriting and limited distribution. These are relationship-deepening products, not intended for the mass-market. The audience is simply too small to generate 200,000-plus incremental accounts in a single quarter. And if premium cards were driving the growth, you’d expect higher spend per account. That’s not showing up in the numbers.

So the real question heading into Q2 is whether spend starts to move. If it does, this quarter looks like the early signal of a more deliberate push into card acquisition.

We’re digging into this further on the next episode of The Free Toaster News Pod later this week.

Sponsored by Bulldog Media Group

Reach the Borrowers Others Miss.

Bulldog Media Group specializes in connecting consumer lenders with less than perfect borrowers — a massive, underserved market that requires precision targeting to get right. With 25 years of financial services marketing experience, they deliver qualified leads through affiliate marketing, targeted email, and data-driven acquisition strategies built for this exact audience.

If you’re a lender looking to scale, these are your people.

JPMorgan Reports Record Q1 2026: $16.5B Profit Amid Robust Growth

JPMorgan posted $16.5B in net income for Q1 2026, up 13% year-over-year, on managed revenue of $50.5B. Average loans grew 11% YoY, card sales volume jumped 9%, and the Card Services net charge-off rate held at 3.47%. Card Services & Auto revenue hit $7.8B, up 13%, driven by higher revolving balances. The Payments business brought in $5.1B, up 12%, on deposit growth and fee expansion. Active mobile customers grew 7% YoY, and the bank opened over 450,000 net new checking accounts in the quarter. CEO Jamie Dimon credited broad-based performance across the franchise, noting that "we continued to acquire new customers at a robust rate," but was measured on the macro outlook: "There is an increasingly complex set of risks, such as geopolitical tensions and wars, energy price volatility, trade uncertainty, large global fiscal deficits and elevated asset prices." (JPMorgan Chase & Co.)

Citi Q1 2026: Cards and Payments Fuel $5.8B Net Income Surge

Citigroup’s Q1 2026 numbers came in strong: $5.8B in net income, up 42% year-over-year, on $24.6B in revenue. The card business is the number to watch. U.S. Consumer Cards pulled in $4.8B in revenue and opened nearly 2.95 million new accounts in the quarter, while net credit losses dropped 11% YoY on improved performance across both general purpose and private label portfolios. Spend volume was up 5% and returns came in just under 20%. On the payments infrastructure side, Treasury and Trade Solutions hit $4.6B, up 17%, with commercial card spend up 8% and cross-border transaction value growing 12%. CEO Jane Fraser described it as “an exceptionally strong start,” noting that “U.S. Consumer Cards saw 4% revenue growth and returns of nearly 20%.” One deal worth flagging for anyone tracking co-brand distribution: the forward purchase commitment of the Barclays American Airlines card portfolio drove a meaningful portion of the ACL build this quarter, suggesting Citi is still actively expanding its co-brand footprint even as others pull back. (Citi)

News Pod #13 - Experian No Ding Decline, American + Citi CoBrand, and Cash App P2P News

In the latest episode of The Free Toaster, Carlos and Nick welcome Capital One veteran Amanda Braslow to break down Experian’s massive “no-ding” expansion into personal loans and why 40% of marketplace volume has already shifted to these rails. The crew dissects the Citi and American Airlines exclusive renewal as a high-stakes play for premium lounge dominance and reacts to Cash App bringing BNPL to P2P transfers.

Catch us on Apple Podcasts, Spotify, Substack, or your favorite player.

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

JetBlue and Barclays Add Companion Passes and Status Accelerators to Premier Card

JetBlue and Barclays added several statement credits and status accelerators to the JetBlue Premier World Elite Mastercard while maintaining the $499 annual fee. Cardmembers now receive a 25-tile bonus annually. This deposit completes 50% of the requirements for Mosaic 1 status. The update introduces a tiered companion pass system where $15,000 in annual spend earns a credit up to $500. Spending $75,000 unlocks an additional credit worth up to $1,500. JetBlue also added a 15% redemption rebate on TrueBlue points for award flights and up to $300 in annual credits for TrueBlue Travel bookings. A new partnership with ClassPass provides up to 14 monthly credits for fitness and wellness services. These changes coincide with the airline's expansion of its BlueHouse lounge network. A second location opens at Boston Logan International Airport this summer following the recent opening at JFK. (JetBlue)

NFL and U.S. Bank Expand 20-Year Relationship with Official League Sponsorship

The NFL named U.S. Bank its official bank and wealth management sponsor in a new multi-year agreement. The bank becomes the presenting sponsor of the Super Bowl MVP Award starting with Super Bowl LXI. It also takes a top-tier sponsorship role for the NFL FLAG Championships. The partnership centers on U.S. Bank Financial Edge, a program providing financial education to players regarding cash flow and long-term wealth. Prospect Fernando Mendoza will advise the bank on tailoring these services for athletes navigating NIL contracts. Both organizations will launch a joint corporate social responsibility initiative in the coming months. This deal formalizes a relationship between the two entities that has lasted over 20 years. (US Bank)

Upcoming Toaster Events:

CardCon, April 21-23, 2026 - Amanda, Toaster’s GM of Events, will be at CardCon in Phoenix, Arizona, before heading to The Fintech Summit on April 28, 2026, as part of the action-packed Fintech Week NYC. Whether you are looking to talk shop, explore new partnerships, or simply catch up over coffee, we invite you to connect with us during these events. Contact amanda@thefreetoaster.com

Eliminating Funnel Friction, Private Dinner, April 27th in NYC - We’re hosting a curated dinner in New York City. Our objective is simple: facilitate a high-level exchange on what’s actually working to eliminate friction in your marketing funnel. No presentations. No conference booth vibes. Just 15 marketers, great food, and candid discussion on smart design and better tech to convert your customers. Learn more about the event here.

Bummed about missing CardCon this year? Join Jason Steele, founder of CardCon, and a select group of credit card marketing leaders to talk industry trends at an executive luncheon in NYC on May 6th. If interested, reach out at: jasondsteele@gmail.com.

loanDepot Integrates Figure Underwriting to Launch 5x5 HomeLoan Product

loanDepot and Figure Technology Solutions launched the 5x5 HomeLoan, a digital product offering mortgage approvals in five minutes and funding within five to seven days. loanDepot is a national retail lender that has funded $577 billion to consumers and operates a sales force of 1,800 licensed loan officers. The company integrated Figure’s blockchain-based underwriting engine into its mello technology platform to automate credit decisions. This partnership allows loanDepot to offer purchase, refinance, and equity lines ranging from $25,000 to $750,000 across all 50 states. The product eliminates appraisal fees, standard title costs, and standard closing costs for borrowers. Management expects the integration to reduce the cost to produce loans and increase market share. The loans feature fixed or variable rates with no prepayment penalties. (loanDepot)

Atlas Raises $40M to Pivot From Failed Debit Startup to $420M Billionaire Charge Card

Atlas closed a $40 million Series C funding round at a $420 million valuation led by Elad Gil and Verified Capital. The company operates a high-end charge card with a $999 annual fee and a text-based concierge service for travel and dining. This pivot follows the collapse of the founder's previous startup, Point, which lost its entire customer base after Column ended their banking partnership in 2022. Internal data showed 15% of users drove 90% of transaction volume, prompting the shift from mass-market debit cards to ultrawealthy spenders. Atlas now reports a gross revenue run-rate exceeding $20 million with approximately 2,000 customers. The business model relies on annual fees, 2% interchange fees, and commissions from hotel and airline bookings. Lead Bank currently provides the underlying banking infrastructure. The company competes with the American Express Centurion and JPMorgan Reserve cards by focusing on high-touch service rather than traditional reward points. Current investors include Eric Schmidt, Marathon, and 01 Advisors. (Forbes)

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading and Listening to

(Credit Card) Fed Data Signals Consumers Pulling Back on Credit Card Spending (PYMNTS)

(Lending) loanDepot Partners with Figure to Offer Express Path Loan Products to loanDepot Customers (loanDepot)

(Lending) Pagaya Issues AAA-rated $600 Million Personal Loan ABS Transaction (Pagaya)

(Lending) DuPage Credit Union Selects Upstart For Personal Lending (Upstart)

(Personal Finance) Computer Is Now Your Personal CFO (Perplexity AI)

(Credit) VantageScore Launches RiskRatio™ For Credit Benchmarking (VantageScore)

(AI/Shopping) Visa Opens The Door To AI-Driven Shopping For Businesses Worldwide (Visa)

(Credit) ClearScore Launches New Technical Standard For Agentic Credit Broking (FinTech Futures)

(Banking) Nymbus Launches Industry-Leading, Secure MCP Server For AI-Driven Core Banking Actions (Nymbus)

(Payments) New Loop Partners With Mastercard To Enable Seamless Payments For A Reusable Takeaway Packaging Return System (Mastercard)

(Fintech) Payments Fintech Pepper Pay Declares Bankruptcy (American Banker)

(AI/Banking) Ask, And AIR Makes It Happen (Revolut)

(Credit/AI) Moody’s Brings Credit And Compliance Workflows Directly Into Anthropic’s Claude (Moody’s)

(Payments) PayPal Embeds Payment Links Into Canva Designs (PYMNTS)

(Banking) Citigroup Says AI Helps Speed Account Openings And Systems Upgrades (Reuters)

(BNPL) Velera Wants Consumers To Turn To Credit Unions For BNPL (Velera)

(Financial Health) A Billion Connected: How We’re Empowering Even More People On The Road To Financial Health (Mastercard)

(Payments) Ahold Delhaize USA Introduces Pay By Bank Partnership With Fiserv To Expand Digital Payment Options For Online Grocery Orders (GlobeNewswire)

(Lending) Experian’s First-Of-Its-Kind Self‑Service Digital Onboarding Platform Helps Small Lenders Pull Credit Reports Quickly And Efficiently (Experian)

(Lending) Braviant Holdings Closes Two Revolving Asset-Backed Credit Facilities And A Forward Flow Facility (PR Newswire)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/wells-fargo-books-631000-new-credit

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.

Was just reading this. Are we not seeing the huge growth in accounts not show up in terms of balances and spend because it’s YoY increase in new accounts opened, not YoY increase in total customer accounts? In other words you could increase new additions by a big percent YoY but if it’s on a massive base the percent increase in the base is actually small