TU Acquires Monevo, Signaling A Move Into The Affiliate Marketing Space

TransUnion increases its stake in the business from 30% to 100%

TL;DR

TransUnion doubles down on fintech by acquiring Monevo and signals a push into affiliate marketing for lending, while CFPB's new credit card comparison tool challenges "pay-to-play" practices, saving consumers hundreds annually. Fintechs like Brex and Mercury are ramping up marketing and expanding products, showcasing the sector's maturity, but defaults on credit cards hit a 14-year high, with consumers stretched thin by inflation and rising costs. Meanwhile, fintech players continue to innovate: Yendo offers subprime borrowers car-secured credit cards, and "hyperscalers" like Nubank disrupt traditional banking with AI and embedded finance. On the regulatory front, Bernie Sanders and Donald Trump may align on a bold credit card interest cap, threatening banks’ profit margins.

News

(1/8) TransUnion will acquire the remaining shares of Monevo, a UK-based credit prequalification platform, to meet the growing demand for personalized online credit experiences. TransUnion, a global information company, already owns 30% of Monevo and aims to enhance financial inclusion and responsible lending through this acquisition. Greg Cox, CEO of Monevo, calls it a "natural next step" for future growth. The deal is expected to close by Q2 2025, subject to regulatory approvals. [TransUnion]

The Toaster team finds this particularly interesting because it signals, at least to us, TU's intent to become a player in the affiliate marketing space for lending.

Monevo is one of five fintech businesses owned by Quint Group Limited. Greg Cox met with Robin Amlot of IBS Intelligence back in August 2024 and shared a few things we found interesting.

The Quint Group’s portfolio of 5 businesses has generated revenues totaling half a billion pounds since its inception. Monevo is their biggest business.

All were bootstrapped with an initial investment of 25,000 pounds, over a decade ago.

Never taken venture capital. TU’s minority acquisition in 2021 marked their first and only source of external investment.

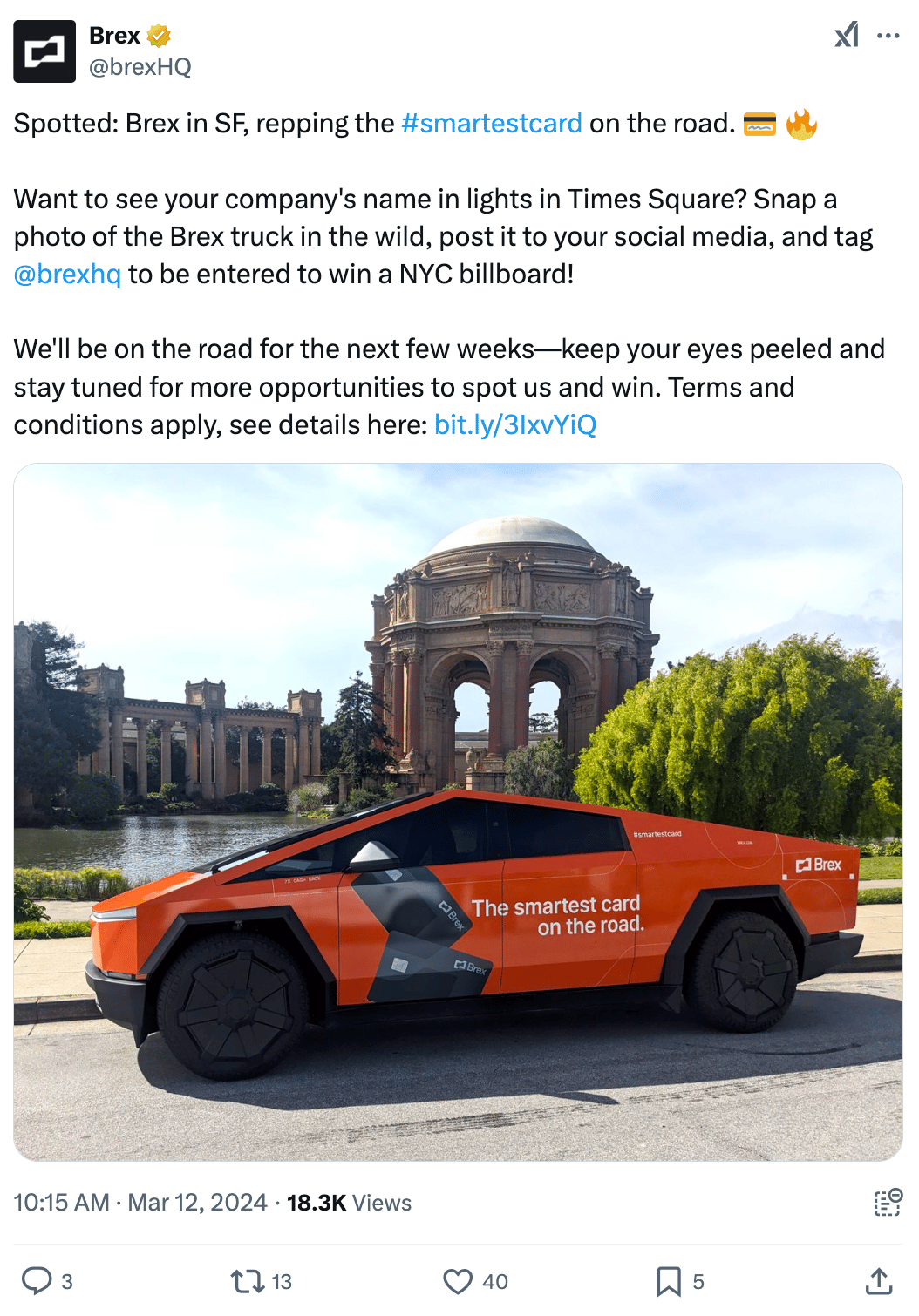

(1/5) Fintechs are splurging on ads, with spending soaring by an average of over 45% annually as they aim to capture a broader audience. Brex, known for its corporate credit cards, has ramped up its marketing budget by 30% each year, shifting focus from startups to enterprises. "Their addressable market is continuing to grow," notes Jeff Titterton from Stripe, highlighting the sector's maturity and IPO potential. Meanwhile, Mercury expands its offerings with new consumer banking products, aiming to redefine itself beyond just a startup bank. [Bloomberg]

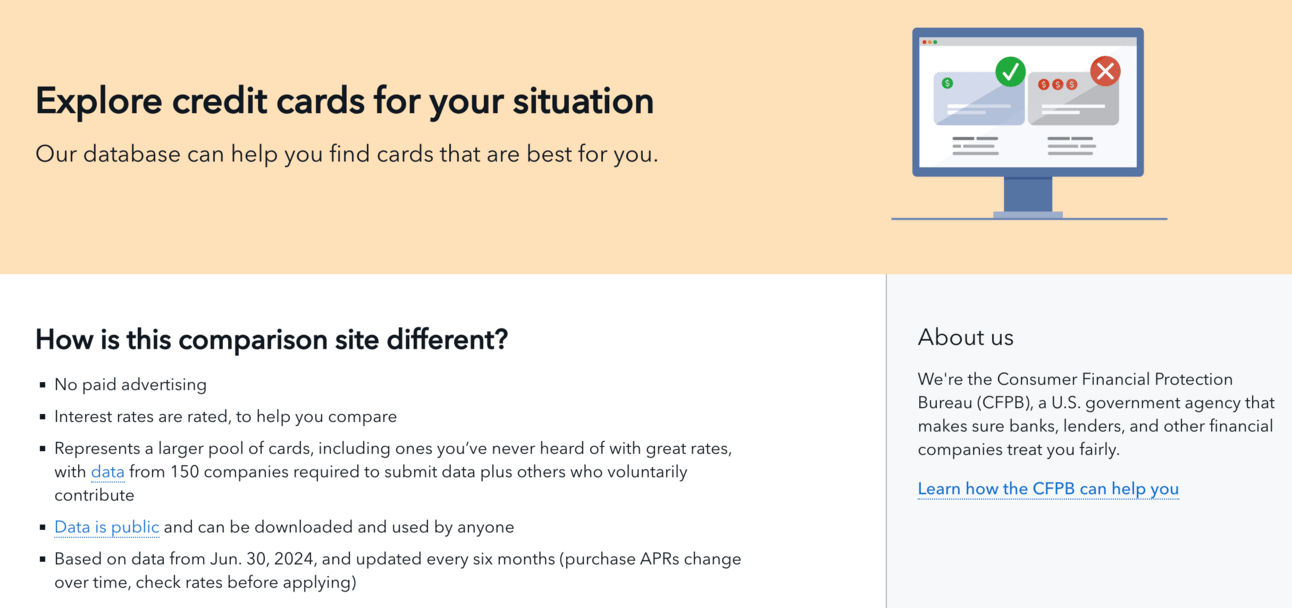

(12/18) The CFPB launched "Explore Credit Cards," a tool offering unbiased comparisons of over 500 credit cards, aiming to cut through "pay-to-play" noise and promote competition. It empowers consumers with data on interest rates, fees, and rewards, revealing that the 25 largest issuers charge rates 8-10% higher than smaller banks, potentially saving cardholders $400-$500 annually. The CFPB encourages smaller issuers to contribute data, leveling the playing field in this competitive market. Next data release: Spring 2025. [CFPB]

(12/31) Dave faces an amended complaint from the DOJ, adding civil money penalties and naming CEO Jason Wilk as a defendant. Dave calls this "government overreach" and vows to defend its compliance record, highlighting past positive reviews from other agencies. Meanwhile, Dave simplified its fee structure by removing optional tips and express fees for its ExtraCash product, a move lauded by customers and set to enhance member lifetime value. The company remains optimistic about its future. [GlobeNewswire]

(12/29) US credit card defaults have soared to their highest since 2010, with lenders writing off a staggering $46 billion in seriously delinquent loans in the first nine months of 2024. This marks a 50% increase from last year, highlighting how "consumers' personal finances are becoming increasingly stretched" amid high inflation and elevated borrowing costs. Capital One, a major credit card lender, reported a jump in its annualized write-off rate to 6.1%, up from 5.2% a year ago. As spending power diminishes, the outlook for consumers looks grim, with delinquencies still a percentage point higher than pre-pandemic levels. [Financial Times]

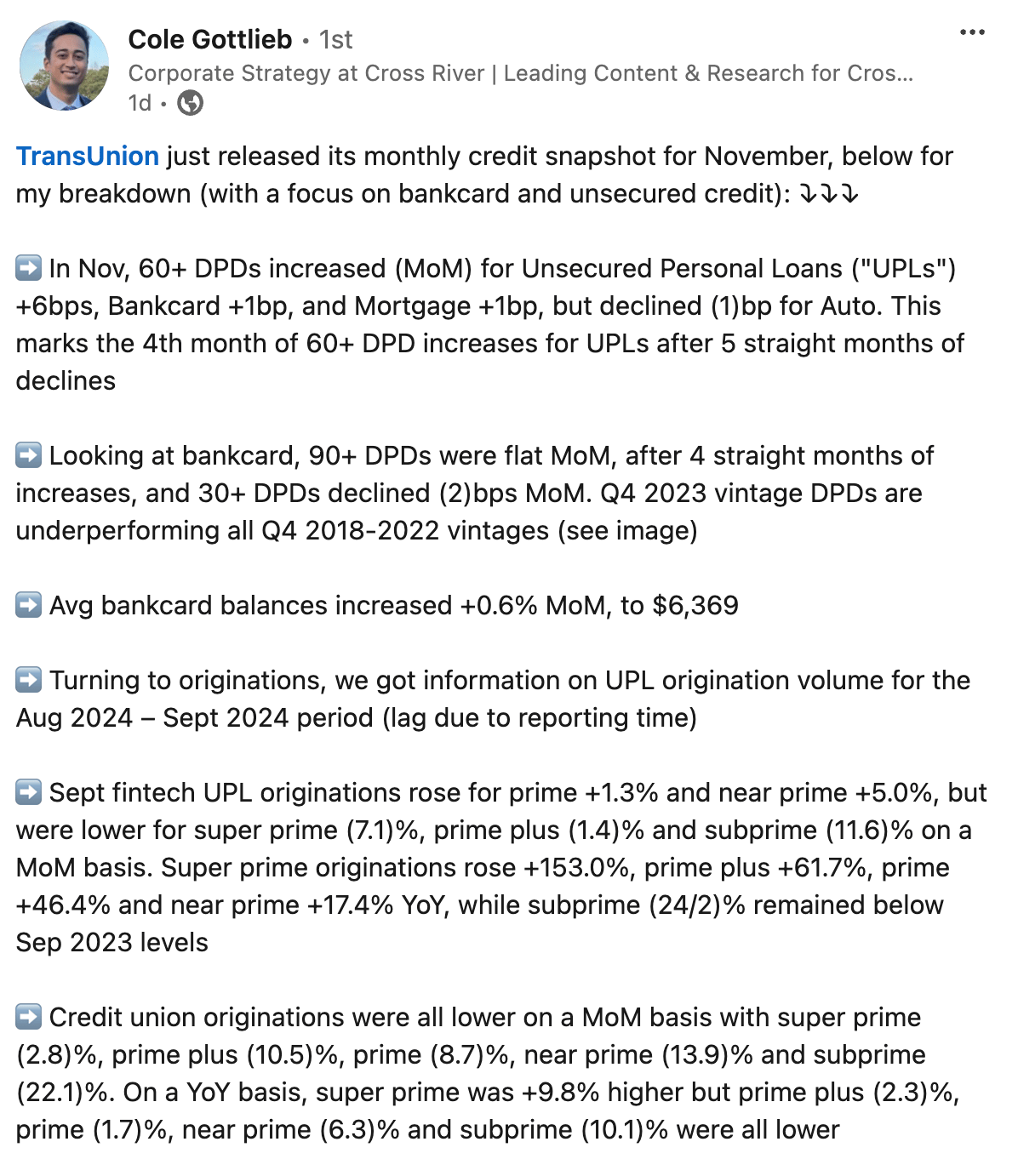

(1/6) TransUnion's latest credit snapshot reveals some intriguing trends in the world of bankcard and unsecured credit. Notably, "super prime originations rose +153.0%," while subprime originations dropped significantly. Average bankcard balances saw a modest increase to $6,369, highlighting a shift in consumer behavior. As Cole Gottlieb notes, "Q4 2023 vintage DPDs are underperforming all Q4 2018-2022 vintages," signaling potential challenges ahead. [TransUnion via Cole Gottlieb]

(12/15) The "State of Fintech 2025" report outlines the rise of "fintech hyperscalers" like Nubank and Revolut, which are disrupting traditional banks with massive customer bases and AI-driven innovation. Trends like embedded finance, stablecoins, and open banking are reshaping payments, with giants like Stripe and Visa leading the charge. Meanwhile, the "scamdemic" and regulatory hurdles pose challenges, but the ecosystem remains ripe for growth, particularly with AI and wallet wars transforming consumer experiences. [Fintech Brainfood Newsletter]

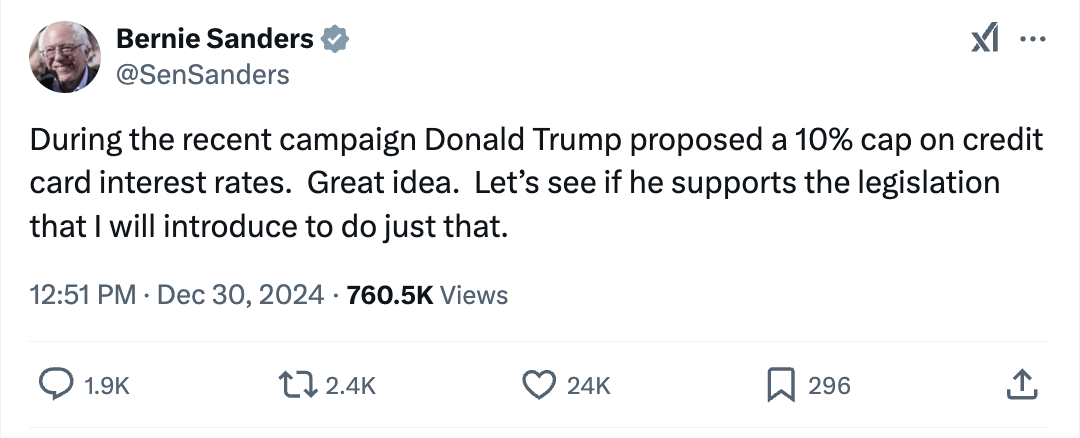

(1/7) Could a surprising alliance between Sen. Bernie Sanders and President-Elect Donald Trump lead to a cap on credit card interest rates? Sanders is ready to propose legislation, echoing Trump’s campaign promise of a 10% cap, a move that might shake up the banking world. Even Republican Sen. Josh Hawley supports the idea, calling current practices "classic collusive, monopolistic behavior." The American Bankers Association, representing bank card issuers, is less than thrilled, having opposed similar proposals in the past. [Payments Dive]

(1/7) Fintech startup Yendo is shaking up the lending scene with a novel credit card secured by your car, aiming to help subprime borrowers escape predatory loans. CEO Jordan Miller wants to "stamp out title lending and payday lending" by offering an alternative with fixed rates and no interest if paid on time. With credit limits from $450 to $10,000, demand for Yendo's product has been "enormous," quadrupling its member base in 2024. However, as Matt Schulz warns, losing your car is a real risk, so proceed cautiously. [Fortune]

Other stuff we’re reading

(1/7) CFPB Sues Experian for Sham Investigations of Credit Report Errors [CFPB]

(1/7) Biden Administration Moves to Ban Medical Debt From Credit Reports [NY Times]

(1/7) DigiFi Partners with Ascent to Optimize Loan Originations [PR Newswire]

(1/2) NerdWallet Announces Winners of Its 2025 Best-Of Awards [Business Wire]

(1/6) Affinity FCU Partners with a Greenlight Financial Technology to Boost Financial Literacy [Digital Transactions]

(12/31) The 2024 Recovery Signals a New Era For Fintechs [Fintech Primetime Substack]

(12/30) Intuit Credit Karma’s CEO says he got the top job by taking roles no one wanted [Fortune]

(12/30) The next big thing in 2025 will be... [NBT Substack]

(12/24) Are fintech loans a better deal for subprime customers? [American Banker]

(12/24) A Credit-Score Hangover Is Hitting America’s Riskiest Borrowers [WSJ]

(12/23) Fiserv to Acquire Payfare, Expanding Embedded Finance Offerings [Fintech.ca]

(12/13) Rocket Mortgage Gears Up for a Brand Restage [Adweek]

Jobs

Spotlight of the week:

Head of Growth Marketing (Origin Financial)

We are seeking an experienced Direct-to-Consumer (DTC) Performance Marketing leader to drive the next phase of user growth for Origin. In this role, you’ll be responsible for developing and executing strategies that enhance customer activation, engagement, and retention, with a strong focus on DTC channels. You’ll lead the creation of paid marketing strategies, experiment with innovative campaigns, and design incentives to effectively acquire and progress leads down the funnel.

The ideal candidate has a proven track record of scaling marketing spend efficiently, with experience across both web and app-based platforms. An agency background would be beneficial, as we’re looking for someone who understands the complexities of consumer acquisition across various challenges. We seek a leader who is comfortable taking calculated risks—one who can try multiple approaches, learn from what works (and what doesn’t), and iterate quickly.

This position is essential to building and scaling our performance marketing efforts and will report directly to the VP of Marketing. You’ll collaborate closely with marketing leadership and cross-functional teams, including product, engineering, and data science, to deliver a seamless customer experience and bring new products and campaigns to market effectively.

Other jobs:

Senior Product Marketing Manager (Credit Karma)

Product Marketing Director, Member Engagement (LendingClub)

Creative Director (Insurify)

Partnership Manager (London) (Monzo)

Director of Credit Risk (Relay)

Head of Customer Marketing (Moody's)

Vice President, B2B Marketing (Mastercard)

Innovation Lead (London) (Cleo)

Senior Marketing Manager (tastylive)

Specialist, Product Marketing (ProShares)

Director, Product Marketing (Thomson Reuters)

Director of Product Marketing (National Debt Relief)

Looking to 2025 (Subscribe to our Podcast!)

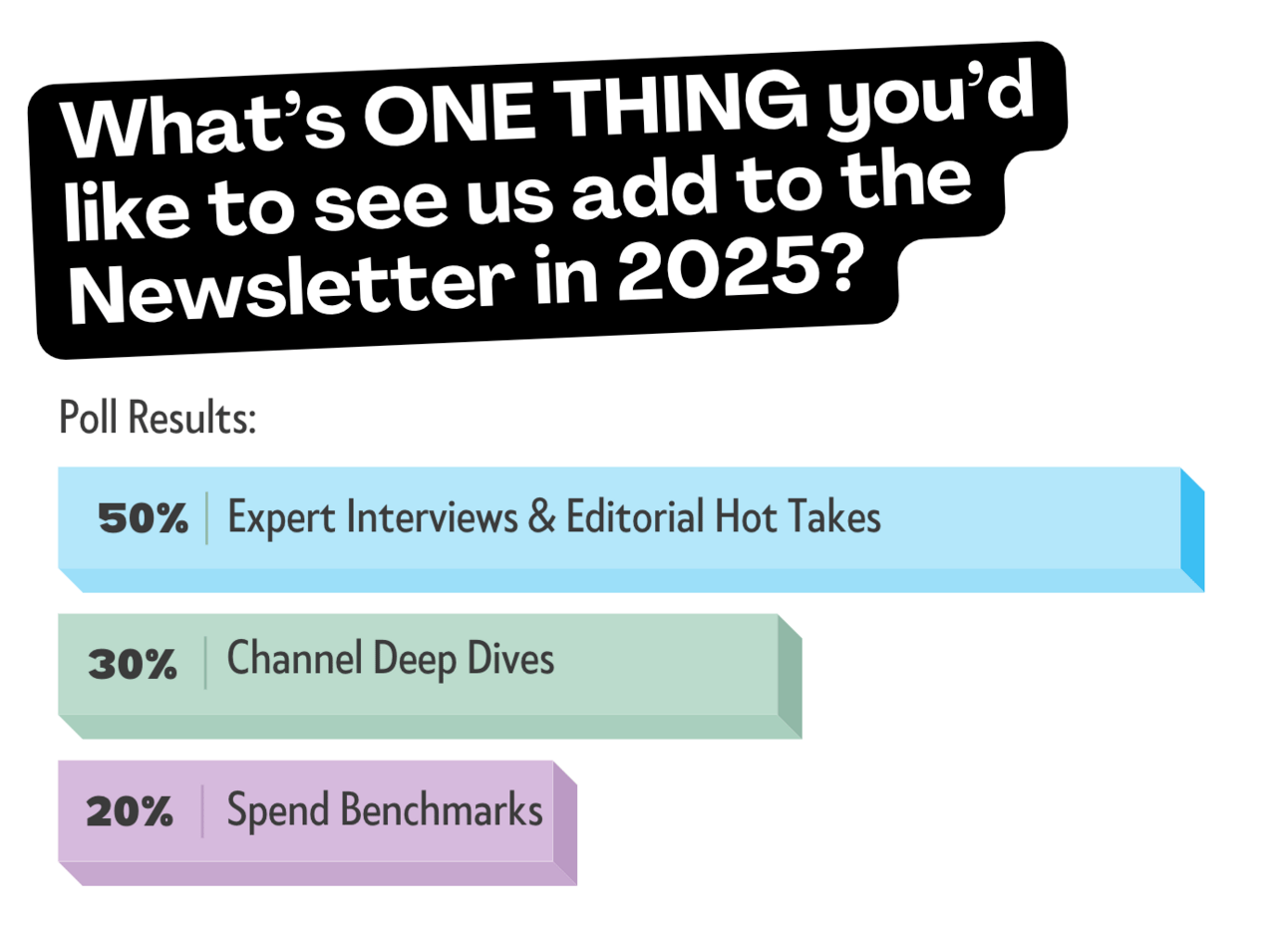

We reached out last week asking you all what you’d like to see more of. Here is a quick summary of the results:

We heard you loud and clear. And we’re excited to announce the launch of The Free Toaster Podcast. We figured this is the best place to address all three of these asks:

Expert Interviews

Editorial Hot Takes

Channel Deep Dives

Be sure to subscribe to the podcast (available on all major platforms!)

About Us

Welcome to The Free Toaster! The newsletter for marketing pros at banks and lenders.

Inspired by the free toasters banks used to give to each new customer, we’re here to help you acquire more customers at scale. We deliver fresh news, data, and insights to help you acquire more customers—minus the breadcrumbs.