Pagaya Sues Klarna for (Allegedly) Stealing Its Underwriting Model

Plus: Visa plugs into OpenAI, Experian moves loan shopping into ChatGPT, and the stablecoin war heats up

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

Pagaya just sued Klarna for allegedly stealing its AI underwriting model, building a competing one with four years of proprietary data, then dropping Pagaya the moment it no longer needed them. Partnership teams, take notes.

Also this week: Visa hooks into OpenAI, Experian moves loan shopping into ChatGPT, Klarna launches a high-yield savings account, and Visa and Mastercard take aim at Circle’s stablecoin dominance.

There’s a lot to unpack. Let’s get toasting!

Carlos Caro, Founder at NMG, Co-Founder of The Free Toaster

Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please subscribe or forward this email to 1 of your colleagues!

Mark Your Calendars For September 23rd!

Affiliate Marketing Summit for Lenders

Proudly Sponsored by Experian & Engine by Gen

Interest in our inaugural edition of The Affiliate Marketing Summit for Lenders is heating up 🔥. Thank you!

So far, we have senior leaders from the following organizations registered: Experian, Engine by Gen, Credit Karma, Bankrate, LendingTree, Credible, QuinStreet, Bulldog Media Group, Lending Club, SoFi, Pagaya, One Main Financial, Perpay, Happy Money, Atlanticus, LendingPoint and FICO.

Learn more about the event here!

If you’re a senior leader that buys or sells affiliate media, this is the one event this year you won’t want to miss.

The room is capped at 150 guests and early-bird pricing is active, so consider registering today!

Pagaya Sues Klarna Over Alleged Trade Secret Misappropriation

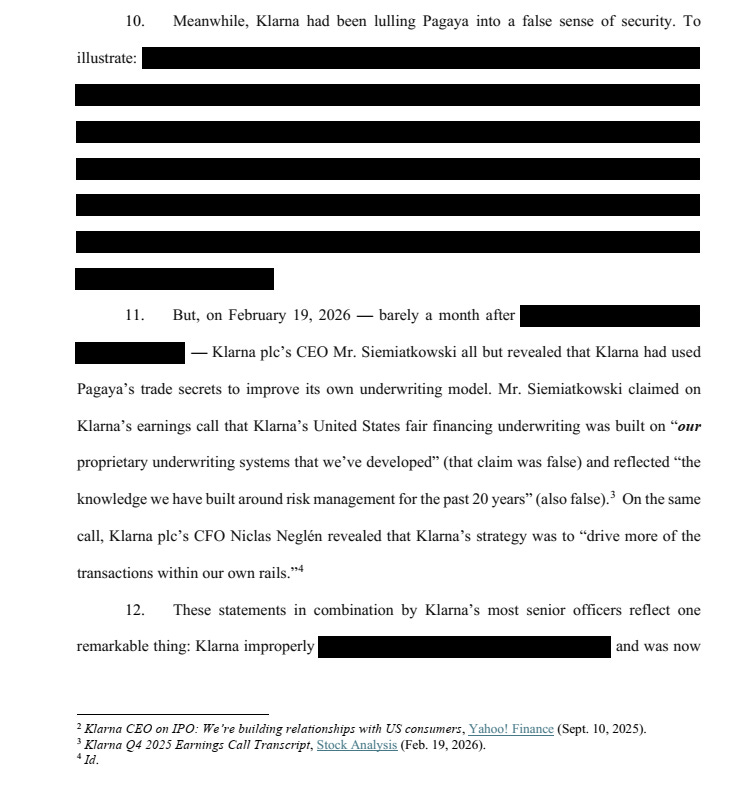

On IPO day, September 10, 2025, a reporter asked Klarna CEO Sebastian Siemiatkowski directly: when assessing loan risk, you’re doing that yourself? Not outsourcing it?

“Nope,” he said.

According to a lawsuit filed in Delaware federal court, that was false. And page 5 of the complaint shows exactly where Pagaya intends to prove it.

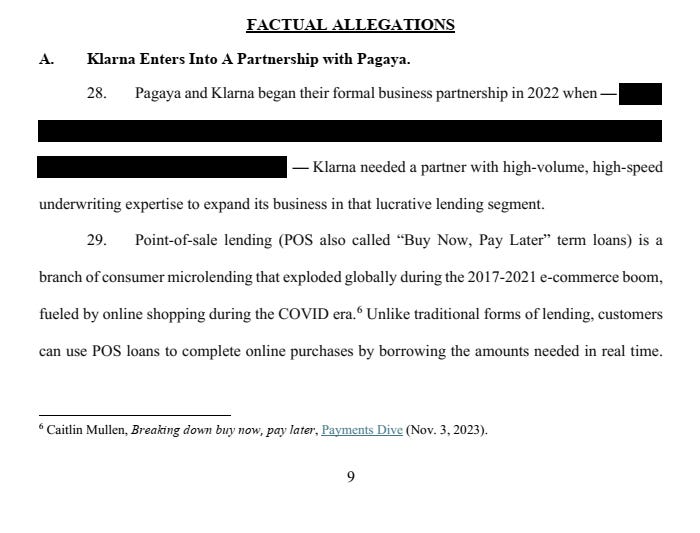

Pagaya Technologies, the AI underwriting firm that powered Klarna’s subprime point-of-sale lending since 2022, filed suit on May 13, 2026 alleging trade secret misappropriation and breach of contract. The core claim: Klarna used Pagaya’s proprietary ML credit model and the years of real borrower performance data it generated to build competing underwriting capabilities internally, then terminated the partnership once it no longer needed Pagaya.

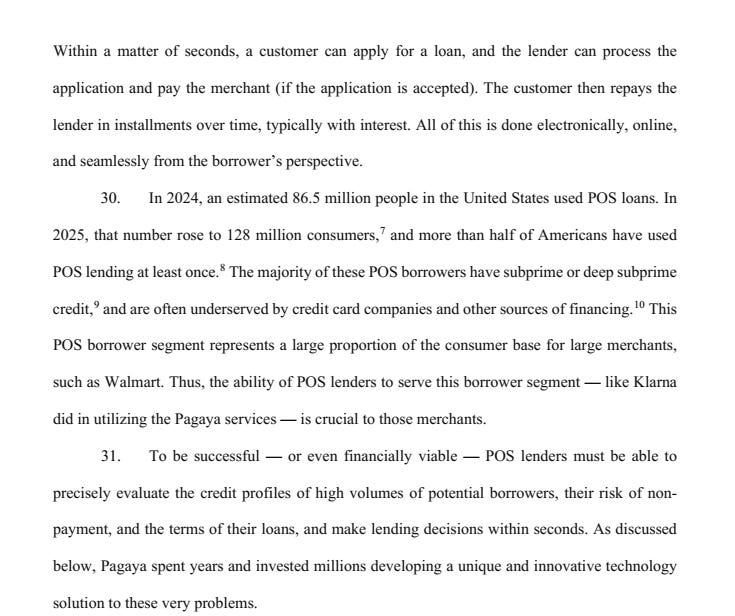

The market Klarna wanted access to is not small. Per TransUnion data cited in the complaint, 128 million Americans used BNPL in 2025, up from 86.5 million the year before. The majority are subprime or deep subprime, exactly the segment Klarna could not profitably underwrite before Pagaya.

Before the partnership, the complaint states plainly, Klarna lacked the technical capability to underwrite this borrower segment. Pagaya invested over $100 million developing the model. By May 2025, it had launched a $1B+ securitization program with Klarna as the sole originator. By March 2026, Klarna had quietly signed a deal with a new financing partner and pulled the plug, reportedly while still telling Pagaya and WebBank the existing deals were “good to move forward.”

What Pagaya is actually fighting to protect breaks into three categories, laid out clearly on page 16 of the complaint.

The model itself, the data it generated across four years of live lending decisions, and the operational and structural knowledge required to package subprime POS loans into rated ABS deals. That third category is the one people underestimate. Getting investment-grade ratings from Kroll on a subprime consumer ABS requires having actually done it. Pagaya had. Klarna, allegedly, learned how by watching.

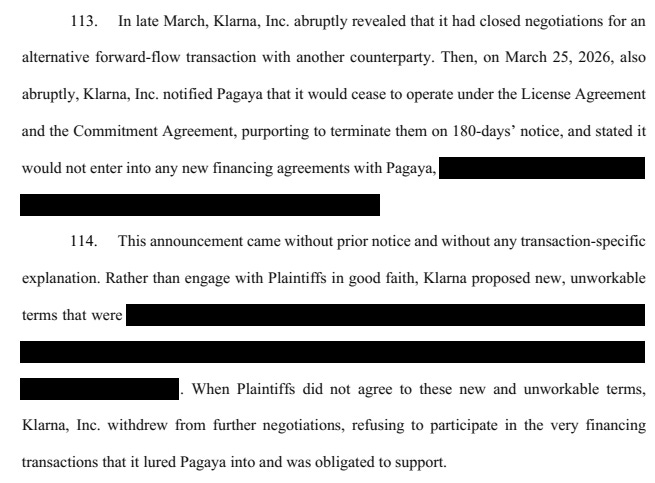

The ending was abrupt. Page 37 shows how fast it moved.

On March 25, 2026, Klarna notified Pagaya it was terminating the license and commitment agreements on 180 days’ notice and would not enter any new financing arrangements. No transaction-specific explanation. Klarna had already signed with another counterparty before making the call.

A few things worth thinking through for partnership and lending teams:

The complaint calls Klarna’s alleged conduct “unlawful distillation,” a concept borrowed from AI/ML, where using model outputs to train a competing model exceeds the scope of a limited license. Expect this framing to show up in future fintech data-sharing agreements.

The fintech that signs the merchant deal isn’t always the one doing the underwriting. Klarna owned the Walmart relationship. Pagaya owned the credit intelligence.

Klarna’s IPO filings described its underwriting as proprietary. That disclosure question isn’t part of this lawsuit, but it won’t stay invisible.

Pagaya is asking for injunctive relief that could force Klarna to stop using any model built with Pagaya’s data. If granted, that hits Klarna’s U.S. lending business directly.

Early days here. Klarna called the suit “without merit” and says termination was contractually permitted. No answer filed yet, and discovery hasn’t started. The internal communications around model training are where this gets interesting. [Court filing] [Banking Dive]

Sponsored by Spinwheel

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

Visa Partners with OpenAI to Power the Next Generation of AI Commerce

Visa plugged its payment network directly into OpenAI. The partnership, announced at the Visa Payments Forum in San Francisco, gives OpenAI access to Visa’s global network, tokenization infrastructure, and real-time fraud monitoring to support agent-initiated purchases. Transactions run within user-defined spending limits and merchant category controls, using tokenized credentials with real-time authorization. Visa is building the checkout layer for a world where consumers stop browsing and start delegating purchases to AI agents.

The more pressing question is what happens to affiliate marketing, paid search, and comparison sites if AI agents become the primary way consumers discover and buy financial products. Visa’s Chief Product Officer said AI will transform commerce more profoundly than the internet or mobile ever did. Card issuers and lenders have spent years optimizing for Google and Credit Karma. The next distribution problem may be getting your product surfaced, compared, and recommended by an AI agent before a human ever sees it. [VISA]

Klarna Launches High-Yield Savings Account, Turning Everyday Spend Into Everyday Savings

Klarna just launched a high-yield savings account in the U.S. The product is FDIC-insured through WebBank, carries no minimum deposit, no monthly fees, and opens at 3.28% APY. Klarna already holds over $12.3 billion in deposits across eleven European markets, so the U.S. launch is a proven model in a new geography, not a product experiment.

The savings account is the third piece of a product suite we’ve been watching come together in real time. In March, we covered Klarna‘s card hitting 5 million active users globally, pacing at roughly 270,000 new cardholders a month. Around the same time, Klarna reported scaling past $17 billion in U.S. volume. Now comes savings. BNPL built the top of the funnel. The card deepened the daily relationship. Deposits take it further, giving Klarna a reason to be in the app on days when nothing is being purchased. Together with the Klarna Card and Klarna Balance, the savings account is designed to create one place to manage the full picture of everyday financial life. That’s the full-stack consumer finance playbook, and Klarna is executing it faster than most competitors expected. [Klarna]

Visa, Mastercard $38B Swipe Fee Settlement Wins US Judge’s Approval

A federal judge granted preliminary approval to Visa and Mastercard‘s $38 billion settlement with merchants on June 9, resolving a case grinding through courts since 2005. The deal cuts swipe fees by 0.1 percentage points for five years and caps standard consumer rates at 1.25% for eight years. Swipe fees totaled nearly $119 billion in 2025 alone, so even modest rate adjustments move serious money across the ecosystem.

The headline number isn’t the $38 billion. It’s the “Honor All Cards” rule dying. Merchants can now decline premium rewards cards at checkout while still accepting standard credit and debit. That’s a direct hit on the interchange economics that fund co-brand programs, cashback offers, and acquisition campaigns. Issuers built entire customer acquisition machines on the assumption that rewards cards would always get accepted. That assumption just got a lot less certain. The Electronic Payments Coalition, which includes Bank of America, Capital One, Chase, and Citibank, backed the settlement, but the National Retail Federation remains opposed and plans further challenges. A fairness hearing still needs to happen before Judge Cogan grants permanent approval, so the uncertainty hanging over interchange economics isn’t going away anytime soon. [Reuters]

News Pod #22 – JD Power Sues Chime, Plus the Big Questions Facing Affiliate Marketing

In the latest The Free Toaster News Pod, we break down JD Power’s lawsuit against Chime over its “America’s #1 choice for banking” campaign and what the case could mean for fintech marketing claims, brand partnerships, and customer trust.

Carlos and Nick also preview the upcoming Affiliate Marketing Summit for Lenders, discussing the future of search, AI-native brands, human signal in a world flooded with content, lender unit economics, cross-channel attribution, and whether AI strengthens or replaces the partnership function.

Catch us on Apple Podcasts, Spotify, Substack, or your favorite player.

Please support our Newsletter by sharing this edition with a colleague!

And, consider checking out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Why Visa And Mastercard Are Building The Stablecoin That Could Sink Circle

Stripe, Visa, and Mastercard are reportedly building a shared stablecoin platform to take on Circle and Tether, which together control roughly 80% of the $325 billion stablecoin market. The moves have been telegraphed for over a year. Stripe paid $1.1 billion for stablecoin infrastructure firm Bridge. Mastercard spent up to $1.8 billion acquiring BVNK. Visa is already settling across nine blockchains at a $7 billion annualized rate. These aren’t exploratory bets. They’re the pieces of an issuance stack being assembled in real time.

The threat to Circle isn’t technical. Circle already solved the engineering. The problem is distribution, and that’s the one thing Visa and Mastercard have spent six decades perfecting. Visa runs more than 130 stablecoin-linked card programs across 50+ countries. Mastercard has direct bank and merchant relationships at a scale Circle‘s IPO couldn’t buy. The GENIUS Act (the federal stablecoin regulatory framework enacted in 2025) makes this worse for Circle: once a compliant dollar token becomes a commodity any licensed issuer can mint, the contest shifts entirely to who can place it in front of the most merchants and consumers. That’s not a race Circle is equipped to win. [Forbes]

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Spot something worth sharing with your team? Drop this week’s edition in their inbox.

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.