Oportun's Bank Partner Held No Loans. And That Just Changed.

A case study in why your bank partnership, not your media, could be your real growth constraint.

Hey Toaster Readers,

This week is sponsored by our friends at Fintel Connect.

Quick housekeeping first. The last few weeks have been a slow news cycle, so we’ve been trying something new: taking a single story from the week and going deeper than we normally would. Please let us know if you like this format or not by replying to this email.

We want to hear from you.

This week’s story is “Oportun and Column Announce New Lending Partnership to Expand Access to Responsible Credit.”

At first glance, not that exciting. Just a new partner bank.

Then we dug into the filings and found something strange: for the past nine months, Oportun had a bank partner that wouldn’t hold a single one of its new loans. Pathward originated them, and Oportun bought back 100%. Meanwhile, a growing acquisition machine in consumer lending (referrals in Q1 2025 up 352% year over year) sat idling with nowhere to run.

This is why the Column deal is more than a routine bank partner transaction. It might be the moment Oportun’s marketing team finally got the green light.

TOASTER EVENT ALERT 🚨

The Affiliate Marketing Summit For Lenders & Publishers

New Publishers & Lenders are signing up every week

September 23, 2026 - San Francisco

Day 2 (relationship building in wine country) is almost sold out

Learn more at events.thefreetoaster.com

Thank you to our event sponsors! Experian, Engine by Gen, & Prism Data

Backstory: A Phantom Bank Partnership 👻

Here’s an arrangement that should make any marketer queasy.

Under a September 2025 amendment, Pathward stopped retaining Oportun’s loans. From October 1, 2025, Oportun bought 100% of everything Pathward originated. Then it bought back Pathward’s existing book too, $115.0 million on October 3, 2025, with the remainder acquired on February 4, 2026.

Oportun was renting a charter from a bank partner who wouldn’t hold a single loan.

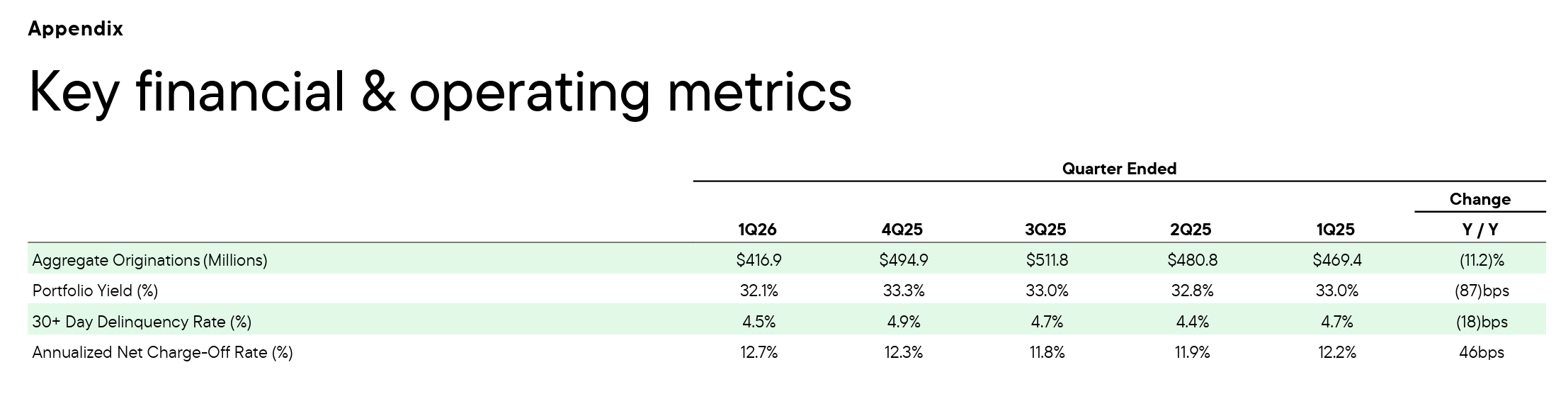

The impact of carrying all of that shows up in the numbers:

Originations fell 11% Y/Y in 1Q26 under what the company calls a “tight credit posture”

FY26 originations guidance sits at just mid-single-digit growth

Sponsored by Fintel Connect

Webinar: Cross-border conversions: winning in Canada’s credit card market

Canada is a high-potential acquisition market, but U.S. affiliates and financial brands need more than a U.S. playbook to win.

Join leaders from Fintel Connect, Finder, and FinlyWealth for a focused 30-minute webinar on how banks, credit unions, and fintechs can use the right affiliate partnerships, localized content, and compliance-ready workflows to drive measurable growth.

What you’ll learn

Where affiliates see the strongest opportunities

What top publishers expect from brand partners

How to navigate Canadian disclosures, CASL, rewards language, and approval processes

Column N.A. Jumps In To Save The Day

Last week’s announcement reads like a funding story.

Column N.A., the nationally chartered bank spun up by Plaid co-founder William Hockey (he acquired and re-charted Northern California National Bank), with clients like Brex, Bilt, and Wise, will originate Oportun’s unsecured personal loans and put its own balance sheet to work through debt financing and loan purchases.

This is great news for Oportun.

And it shows they just overcame a growth blocker many fintechs learn the hard way:

Bank or capital markets partnerships, not media buying, are often the real cap on growth.

Oportun Is Operating With Two Partner Banks At Once

Oportun’s own state-licensing page now tells consumers in 32 states that their loan “may be originated by Pathward®, N.A. or Column N.A.”

Seven states remain Pathward-only (GA, IL, NH, NJ, PA, RI, SD).

NM and WI stay on Oportun’s own licenses.

The 8-K adds the fine print. The agreement “includes certain exclusivity provisions with respect to specified loan products and certain future financial products, subject to existing bank partner rights and other exceptions.” That last clause looks like a direct carve-out for Pathward.

And the deal has “an initial term of four years and renews automatically for successive one-year periods.”

Things got a little more interesting when we learned what business lines each partner bank is supporting.

Secured Personal Loans (SPLs) Will Stay In An 8-State Footprint

Here’s something we didn’t realize about Oportun’s SPL business.

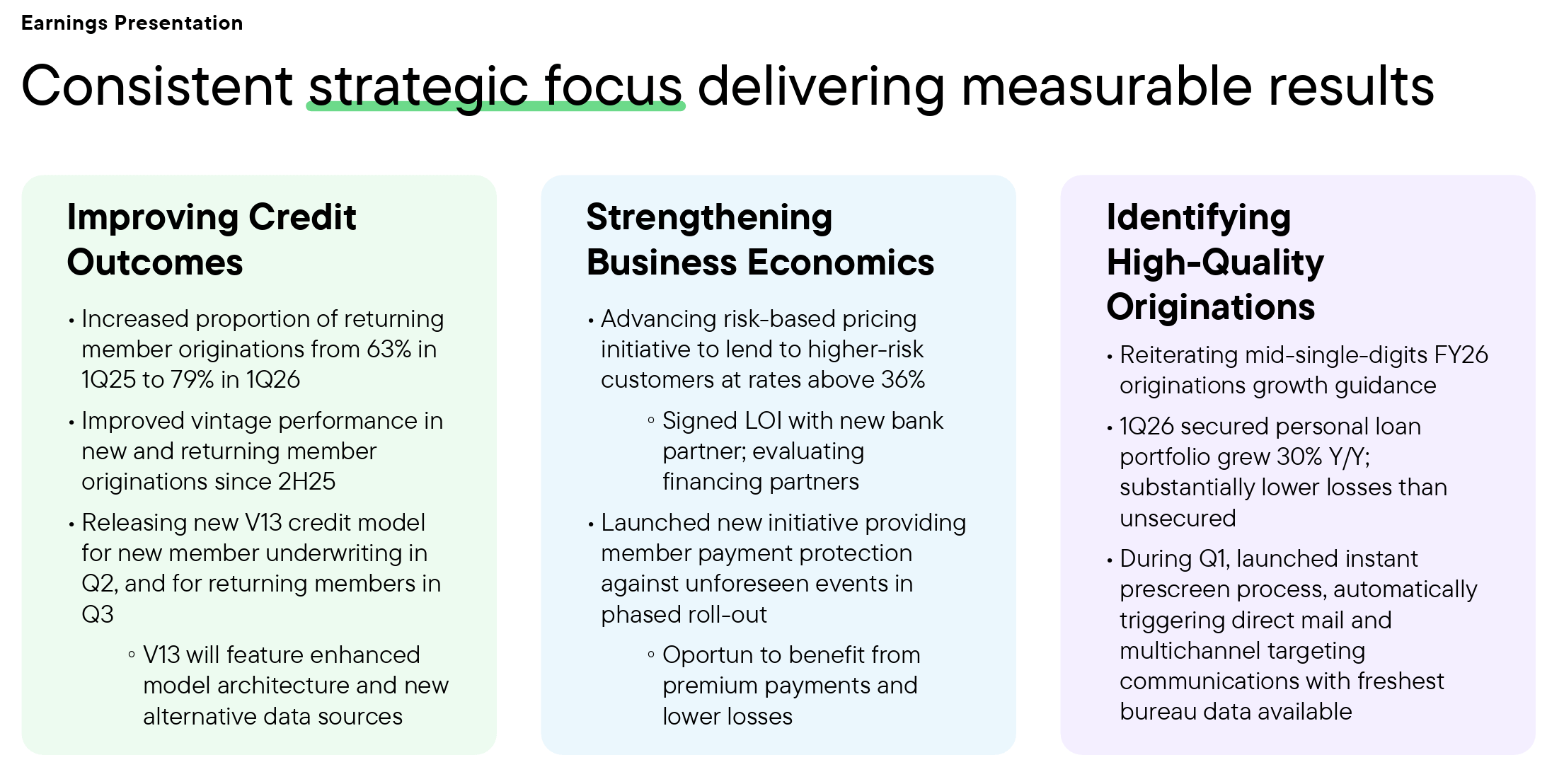

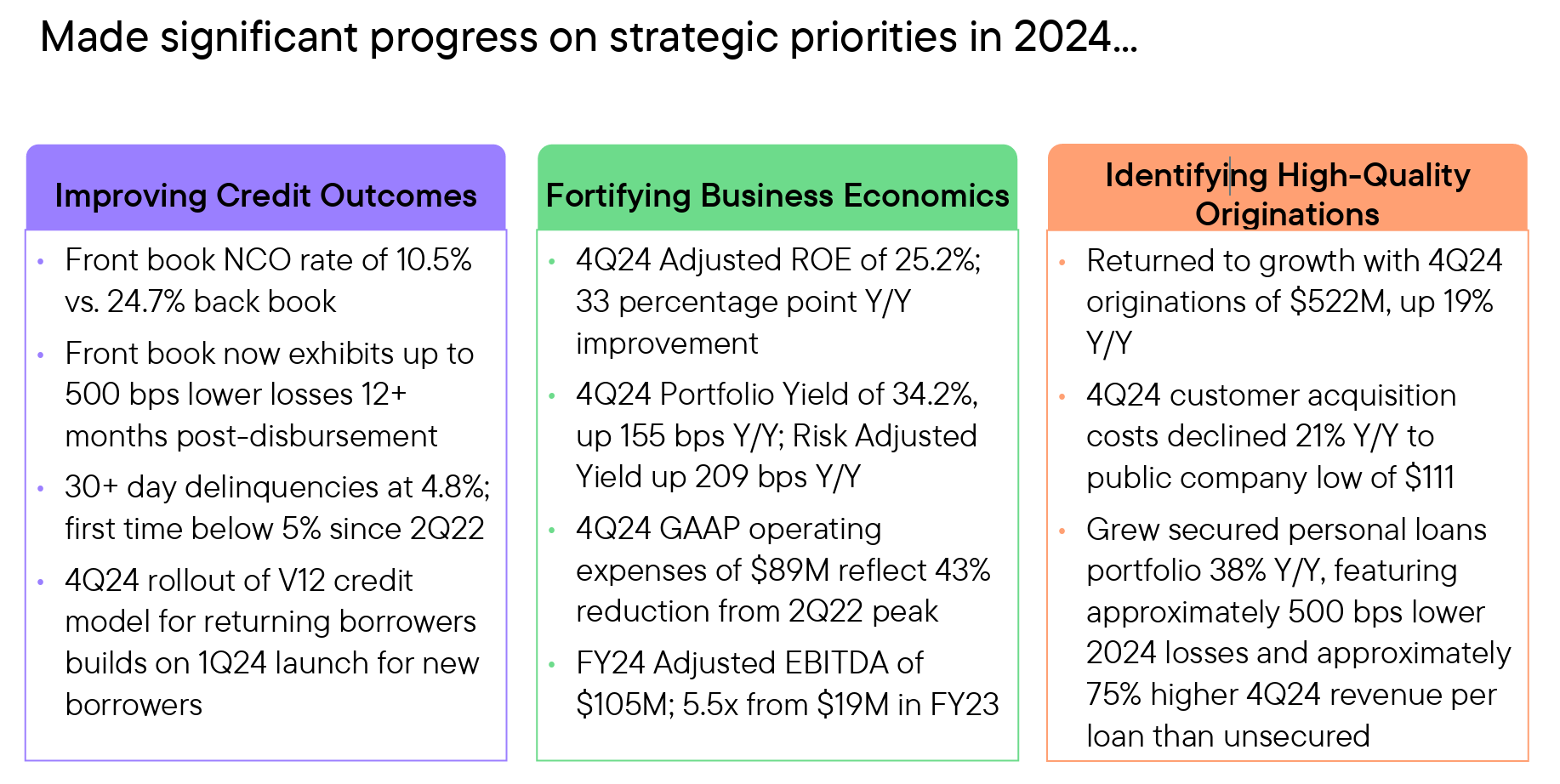

Secured personal loans grew 30% Y/Y in 1Q26 with substantially lower losses than unsecured. A deck from 4Q24 helps put that in context: approximately 500 bps lower 2024 losses and approximately 75% higher 4Q24 revenue per loan than unsecured.

It seems like SPLs are Oportun’s best-performing asset.

And the Column agreement covers unsecured loans only. Column “will originate certain unsecured personal loans for consumers in select states”. SPL is live in eight states (AZ, CA, FL, IL, NV, NJ, TX, UT), and its expansion path to roughly 33 more states runs contractually through Pathward.

One door is already written into the contract: the exclusivity provisions cover “certain future financial products,” which is exactly where an SPL program at Column would live.

SPLs will survive. Whether its national expansion goes through Column, Pathward, or nobody is the open question. The timeline to an SPL program beyond 8 states is the other unknown.

Oportun’s Marketing Metrics Were Looking Good…Until They Hit A Wall

Here’s what Oportun’s acquisition engine was doing while originations shrank:

CAC fell to $117 in FY2025, from $125 the year before, after touching a public-company low of $111 in 4Q24

Referral-driven originations grew 352% Y/Y to $35M in 1Q25

Instant prescreen launched in 1Q26

The machine seemed to be working.

But their bank partner didn’t want to keep funding the loans.

Now we need to watch Oportun’s Q2 earnings.

Will they raise FY26 originations guidance? That would tell us that Column’s capacity has given the marketing team the green light.

Support our Newsletter by sharing this edition with a colleague!

And, please check out our Newsletter sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

And, a big thank you to our September 23rd Event Sponsors!

Now They Can Lean Into National Channels, Like Affiliate Marketplaces

Lenders with big geographic gaps cost the marketplace real money. Between state-level eligibility logic they need build and maintain, unserved customer segments, and potentially wasted impressions, regional lenders aren’t exactly what publishers dream about.

A national bank program makes Oportun’s offer easier to integrate, easier to promote, and more valuable to publishers like Credit Karma, Experian, and NerdWallet.

The national footprint makes life easier in other channels, too.

Direct mail, prescreen lists, digital targeting, telesales licensing, and retail distribution locations were all limited by geographic constraints.

The new partnership with Column unequivocally provides oxygen to Oportun’s growth effort.

But, a separate question remains unanswered about all of this.

Why Isn’t Oportun Part Of The Bank Charter Craze?

Last week, we wrote about the parade of fintechs filing for their own bank charters and moving away from the bank partner model.

Oportun might have been too early to the party.

Oportun began its OCC application for a de novo national bank in November 2020, seeking, in its own words, to “offer additional products and services, provide us with new sources of lower cost funding and give our business regulatory clarity”. It withdrew in October 2021 with a stated plan to refile.

It never did refile.

While Klarna, Affirm, and Upstart took what seems to be the popular path, Oportun chose a different road.

We wonder if it’s because Oportun’s business has historically focused on thin files/credit invisibles, with a focus on underserved hispanic audiences, and a products that were north of 36% APR before 2020.

All of these factors could influence a regulator’s likelihood to approve a bank license.

None of those real-life considerations are easy to talk about, but they lurk in the shadows of this new partnerships between Oportun & Column.

Put differently, is Oportun seeing a strategic advantage to sticking with the bank partner model while others move to secure their own charters, or were there structural reasons that took this option off the table?

If you have a POV on this, we’d love to have you on our News Pod to discuss. Reply to this email if you have a hot take you’d like to share.

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. Reply to this email or write us at info@thefreetoaster.com.