Klarna Just Filed for a Bank Charter. So Did Affirm, PayPal, Upstart, and Six Others.

The year fintechs stopped renting charters.

Hey Toaster Readers,

Klarna wants to be a bank. So do 9 other fintechs. In 7 months, many fintech consumer lenders have headed for a regulator’s door, and the partner banks they’ve been renting for a decade should be nervous.

Inside: who’s filed, why the window opened, whether it stays open, and why bank and fintech marketers should be paying close attention.

This week is sponsored by Bulldog Media Group.

The Year Fintech Lenders Stopped Renting Banks

On July 6, Klarna announced in a press release (and disclosed in a Form 6-K filed with the SEC, with American Banker reporting the same morning) that it had filed applications with the Utah Department of Financial Institutions and the FDIC to establish Klarna Bank USA, a Utah-chartered industrial bank. “Banking is built on trust,” CEO Sebastian Siemiatkowski said in the announcement, calling a U.S. license “the natural next step” for a company that says 30 million Americans use its products every year and that has extended more than $91 billion in credit to U.S. consumers since 2019, all of it through partner banks.

Interesting timing, we think, given that just a few weeks ago, we covered Klarna launching an FDIC-insured high-yield savings account through WebBank and that Pagaya is suing the BNPL provider for allegedly stealing its underwriting model.

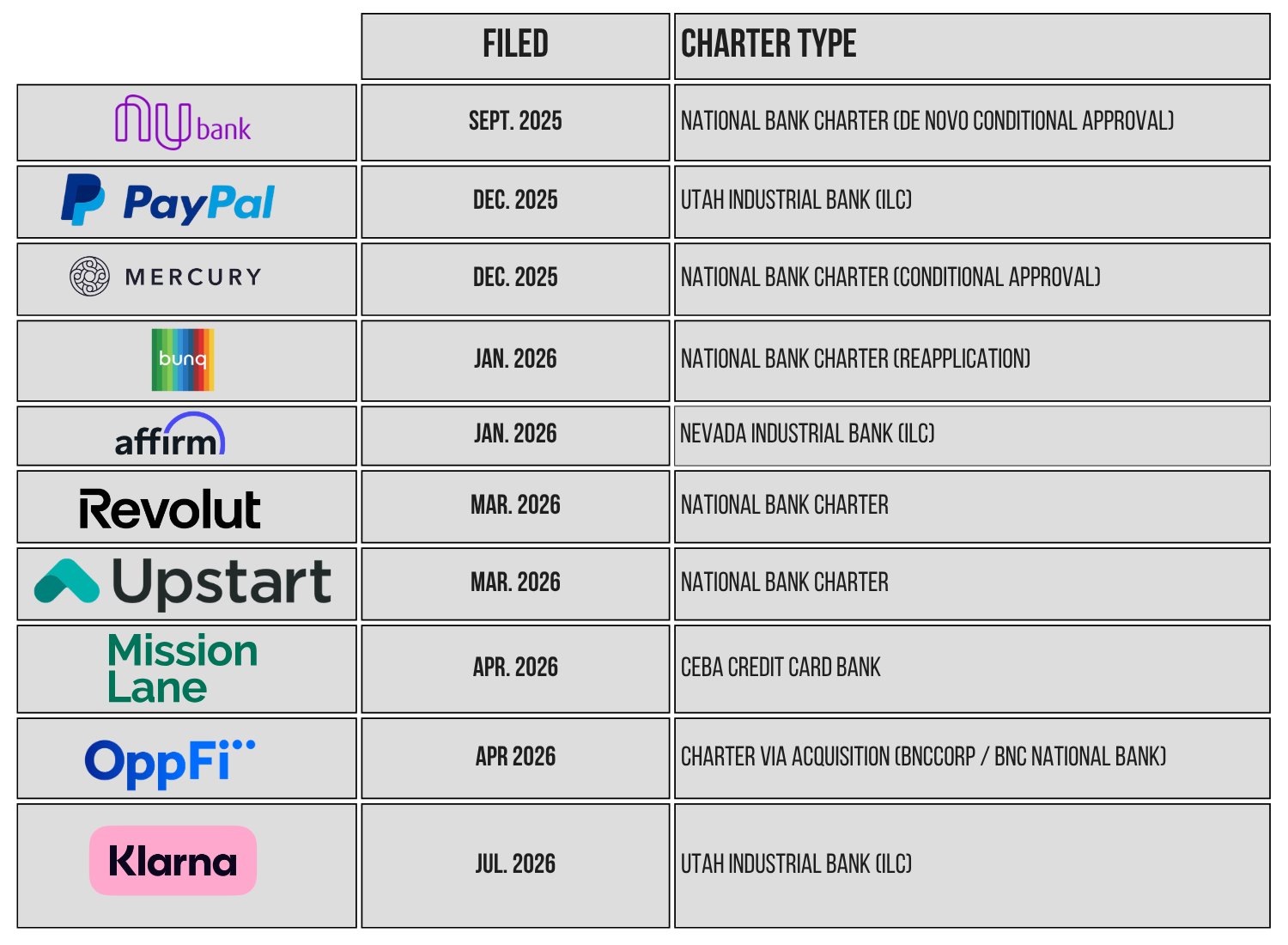

And Klarna is not an outlier. Since December 2025, it’s the ninth major fintech to file for (or buy its way into) a U.S. bank charter. Insured deposits and direct access to the payment rails, the banking industry’s forbidden fruit, are being handed out application by application. The companies queuing up are the same brands that already sit between banks and tens of millions of consumers.

(Don’t Miss Our First Big Toaster Summit)

Affiliate Marketing Summit for Lenders and Publishers

Proudly Sponsored by Experian, Engine by Gen, and Prism Data

Heads up: our Day 2 experience is going faster than we planned, with fewer than 20 spots left.

Our Day 2 is where lenders and publishers trade the conference hallway for a vineyard and build real relationships, not a pocket full of business cards.

We’re spending the day at Ridge Vineyards in Healdsburg, a legendary Sonoma estate that’s been championing single-vineyard winemaking since 1962. It’s designed to be both impactful and entertaining, giving you the time and setting to build partnerships that don’t happen in a Money 20/20 crowd.

Learn more and grab a spot: events.thefreetoaster.com

So…who’s filed for Bank Charters?

The filings cluster into three routes: the industrial loan company (ILC) charter favored by balance-sheet-hungry lenders, the full national bank charter, and, in one notable case, a charter type nobody had touched in two decades.

The OCC saw 18 de novo charter applications in 2025 (that’s nearly equal to the previous four years combined). Klaros Group co-founder Michele Alt expects roughly 25 novel applications in 2026. Approvals are flowing too. The FDIC has conditionally approved ILC bids from Ford, GM, Stellantis and Edward Jones since January; the OCC has granted conditional charters to Mercury and Nubank’s U.S. unit, alongside a wave of crypto-focused national trust banks.

OppFi took a different route, acquiring BNC National Bank in April rather than filing de novo.

And while we have zero insider knowledge of impending applications, we wouldn’t be surprised to see a number of other fintechs join them. Chime is the most obvious contender, their leadership basically pre-announced it in April. Then there’s Robinhood and Wealthfront, two giants wearing software costumes while a bit portion of their revenue is interest income.

The fence is getting increasingly crowded. Walmart-backed OnePay is expanding aggressively, Dave and Current face the exact same partner-bank margin pressures as Chime, and SMB powerhouses Ramp and Rho are feeling the heat after Mercury’s conditional approval. Even Cash App is a wildcard. This could be a now-or-never regulatory window, and few want to be left behind renting someone else’s banking license.

Sponsored by Bulldog Media Group

Reach the Borrowers Others Miss

Bulldog Media Group specializes in connecting consumer lenders with less than perfect borrowers — a massive, underserved market that requires precision targeting to get right. With 25 years of financial services marketing experience, they deliver qualified leads through affiliate marketing, targeted email, and data-driven acquisition strategies built for this exact audience.

If you’re a lender looking to scale, these are your people.

Why are they all filing now?

Three factors converge to make this window imperative.

Funding: insured deposits are the cheapest, most stable money in finance, and a lender that funds receivables through securitizations and warehouse lines can cut its cost of funds materially by taking deposits. “You get access to low-cost funding in the form of insured deposits. That’s pretty cool,” Michele Alt puts it.

Control: a charter removes the sponsor banks that currently sit in the middle of every loan, with their fees, their oversight and their concentration risk. Affirm’s Max Levchin framed his company’s Nevada ILC application as a long-term play for “regulatory clarity” rather than near-term growth.

An Open Door: “Many fintechs and blockchain companies especially did not really have a hope or a prayer of obtaining a bank charter during the Biden administration,” Alt told The Financial Brand. “But they are thinking strategically now and trying to go for the window of opportunity now that it’s open.”

Will regulators keep saying yes?

Credible arguments run both ways, and the outcome will likely be decided application by application.

The argument for continuity is strong. Comptroller Jonathan Gould has called the application boom “a return to the norm for the OCC,” arguing the surge “signals healthy competition, a commitment to innovation and should be encouraging to all of us,” and has blamed years of “anemic chartering” for gaps in credit access. FDIC Chair Travis Hill unfroze the ILC pipeline his predecessors had left dormant and has said a fintech holding deposits inside a regulated bank may pose less risk to the insurance fund than one scattering deposits across complex partner arrangements. Ford, GM, Stellantis and Edward Jones approvals establish live precedent that the FDIC will insure new ILCs, the very question that stalled the class for 15 years.

But there’s a case for caution, too. The Independent Community Bankers of America and the Bank Policy Institute jointly urged the FDIC to reject Affirm’s application and to freeze all ILC approvals until Congress closes what they call the “ILC loophole,” arguing such banks escape consolidated Federal Reserve supervision while leaning on nonbank parents. Senators John Kennedy and Andy Kim have reintroduced the Close the Shadow Banking Loophole Act (S. 3734) to do exactly that. And the OCC itself fired a warning shot in June, publicly reminding applicants it can return filings as “materially deficient.” “The OCC has been getting bad applications from applicants who assume, in the current environment, they don’t have to do the hard work of designing a credible business plan,” Alt said. These reviews routinely run 12 to 18 months, meaning applications filed today may be decided by a differently constituted FDIC board, in a different political moment — and the picture sharpens: the window is real, but it is neither unconditional nor guaranteed to outlast the administration that opened it. Well-capitalized, mono-line lenders with seasoned portfolios and experienced bank management are positioned to get through; thinner applications may simply run out the clock.

Mission Lane: the most interesting filing of the year

Klarna got the headlines, but Mission Lane’s April 2026 filing is also interesting. The Virginia-based issuer, spun out of LendUp in 2018, now serves more than three million cardholders with credit lines of $300 to $3,000 for near-prime and subprime borrowers. Mission Lane applied to the OCC for a CEBA credit card bank charter. It was the first credit card bank charter application in roughly 20 years, according to Michele Alt, whose firm advised on it.

The CEBA charter, a 1987 creation, is a limited-purpose national bank that can issue credit cards nationwide but cannot take demand deposits or deposits under $100,000 (except as secured-card collateral) and cannot make general commercial loans. Its parent escapes Federal Reserve holding-company supervision, and more importantly, it can export its home state’s interest rates to customers in every state.

This is favorable timing for Mission Lane, specifically, due to four factors:

Regulatory receptivity to novel charters. A charter type dormant for two decades only gets dusted off when agencies are visibly approving unusual structures. In 2026, they are.

This limited charter fits the business. Mission Lane does one thing: credit cards. It doesn’t need (and doesn’t care to be examined for) the full universal-bank toolkit an ILC or national charter implies. A limited charter means a narrower application and, plausibly, a faster path.

Its partner-bank model is under structural pressure. Mission Lane originates through Utah’s TAB Bank and WebBank, exporting Utah rates to other states. This is the very “rent-a-bank” architecture that state legislatures and consumer advocates keep attacking. A national credit card bank exports rates under the National Bank Act in its own name, taking that legal risk largely off the table.

Funding economics. Subprime card books are expensive to fund through securitization. Large time deposits, which CEBA banks may accept, are cheaper and steadier — a durable margin advantage in a segment where funding cost is the whole game.

There’s also a layer of competitive necessity worth noting. If Klarna and Affirm become banks while Mission Lane remains a borrower in the wholesale markets, it fights the next decade at a structural cost disadvantage.

Why is Upstart taking the harder road with a de novo filing?

While Mission Lane plays the specialized CEBA angle, Upstart went the other direction entirely. In its March 2026 de novo filing for Upstart Bank, the company applied for a full national charter under a traditional Bank Holding Company framework, voluntarily signing up for OCC, FDIC, and Federal Reserve oversight all at once. That’s the most supervision available in Washington, and Upstart asked for it.

We covered the filing when it landed in March, and the economics explain the choice. Upstart currently operates through 248 state licenses and roughly 100 bank partners, an infrastructure Morgan Stanley estimates costs $200 million a year, or about $135 per loan. A single federal charter cuts that to roughly $50 million. That’s $150 million in annual savings before Upstart changes anything else about how it operates.

The funding side is the bigger prize. Upstart keeps about 14.6% of originated loans on its balance sheet, funded through warehouse lines and securitization, the most expensive money in the room. Swap that for deposits and Morgan Stanley models another $67 million in net interest income versus 2027 consensus. Combined, savings plus income reach $217 million, roughly a 50% upside to 2027 adjusted EBITDA. The BHC route also gives Upstart something the ILC path chosen by Affirm doesn’t: a broader product set and deposit funding as a backstop when securitization markets seize up, the same playbook LendingClub has been running since 2021.

Then there’s the narrative layer. Pure fintech lenders trade at compressed, cyclical lending multiples, and a tech-driven deposit engine gives Upstart a story to tell about being a technology ecosystem rather than a balance-sheet-exposed lender. Klarna is attempting the same repositioning by calling itself a spend-centric business. But unlike the pure story stocks, Upstart filed with $217 million of modeled EBITDA improvement attached. Whether analysts reward the narrative or just price it like a bank, the cost savings clear either way.

Key takeaways for marketers in lending

At face value, this uptick could seem like a dry regulatory development. But for marketing and growth leaders at fintechs and non-bank lenders, it could become a looming distribution shakeup. Here’s what to prepare for:

Affiliate and comparison channel crowding: Expect immediate deposit-side pressure. While Klarna, PayPal, and Upstart spin up native, chartered savings products, they will likely begin aggressively marketing them into the exact same affiliate networks and financial comparison channels you buy traffic from.

Near-prime segment encroachment: As chartered specialists like Mission Lane leverage their newfound regulatory advantages to go after the 70 million underserved Americans traditional banks abandoned after 2008, non-bank lenders face a formidable competitor holding a native compliance moat.

Sponsor bank disruption and tenant churn: Anticipate a shakeup across legacy partner networks as their largest anchor programs migrate to native charters. As historic fee income dries up, these sponsor institutions could be forced to either absorb early-stage programs or pivot to building competing direct-to-consumer lending brands of their own.

A final word of wisdom from Michele Alt: against roughly 4,000 incumbent banks, the new entrants are “tiny,” and will not “go toe-to-toe with the megabanks” immediately. “The thing to watch for is how they grow over the next, say, five years.” The brands filing this year already own the customer’s phone screen. Now they’re coming for the balance sheet. The (maybe) five-year window to respond on brand, trust and relationship starts closing now.

Please support our Newsletter by sharing this edition with a colleague!

And, consider checking out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you.

Sources

Klarna press release: Klarna submits application for U.S. banking license (Jul. 6, 2026)

Banking Dive: Mission Lane applies to become a bank (Apr. 22, 2026)

American Banker: Credit card issuer Mission Lane applies for bank charter

Affirm: Affirm submits applications to establish industrial loan company (Jan. 23, 2026)

PayPal Newsroom: PayPal submits applications to establish an industrial bank (Dec. 15, 2025)

Revolut: Revolut files U.S. bank charter application (Mar. 2026)

American Banker: Dutch neobank bunq reapplies for a U.S. bank charter (Jan. 2026)

Banking Dive: Charter application boom a ‘return to norm’ for OCC: Gould

Banking Dive: FDIC conditionally approves Ford, GM ILC charters (Jan. 2026)

BPI & ICBA: Comment on Affirm Bank’s application for deposit insurance (Feb. 25, 2026)

ICBA: ILC loophole advocacy and Close the Shadow Banking Loophole Act (S. 3734)

Bloomberg: Fintechs call Klaros Group when they want bank charters (Jan. 2026)

Marketplace: Why fintech firms like Klarna want to become banks (Jul. 7, 2026)

Future Nexus: OCC hints at trouble for charters (Jun. 18, 2026)

Banking Dive: Inside the explosion of banking charter applications

The Financial Brand: Fintech banking suddenly advances on multiple fronts

FinTech Futures: OCC conditionally approves Mercury charter application