Intuit Taps OpenAI, Klarna Secures $6.5B, JPMorgan Rewrites Data Terms

Also inside: rising credit stress, new compliance standards, shutdown aftershocks, and a full breakdown of earnings from Experian, Klarna, Mastercard, FIS, FICO, Enova, and Bread Financial.

Hey Toaster Readers,

This week is sponsored by our friends at Fintel Connect.

Intuit just opened the door to a new kind of financial guidance by bringing its AI platform directly into ChatGPT through a long-term partnership with OpenAI. Klarna secured a $6.5 billion forward-flow deal with Elliott to ramp up its U.S. Fair Financing business, giving it a cheaper, scalable funding pipeline. And JPMorgan locked in paid data-access agreements with Plaid, Yodlee, Morningstar, and Akoya, a shift that could reshape how banks, aggregators, and fintechs negotiate data rights in the year ahead.

Capital One’s Discover migration is testing how much network perception still matters. Amscot and Green Dot are pushing modern banking tools into physical service centers. Credit access is tightening as rejection rates hit highs and auto delinquencies climb to record levels. CFES rolled out new lending standards that aim to bring bank–fintech partnerships onto the same compliance page. And even with the federal shutdown resolved, households and regulators are still working through the fallout.

Experian raised its outlook on steady growth, Klarna posted its strongest quarter to date, and Mastercard, FIS, FICO, Enova, and Bread Financial all reported firm spending trends and improving credit results as fintechs head into the final stretch of the year.

Here’s what’s happening across fintech right now.

PS: To support our Newsletter, please share it with one colleague!

Webinar: LLM Playbook with Profound: How Financial Marketers Can Win in AI-Driven Discovery

Join leaders from Profound and Fintel Connect for an interactive live discussion on how large language models (LLMs) are reshaping digital discovery - and what it means for your acquisition strategy. Unpack what signals drive LLM visibility, the role affiliates and publishers play in this new ecosystem, and the practical steps financial brands can take today to stay discoverable and competitive.

When? Tuesday, December 2 | 10 AM PST / 1 PM EST | Microsoft Teams

You'll learn:

How LLMs are transforming digital discovery - and what that means for SEO and acquisition in financial services.

Practical insights into how banks, fintechs, and affiliates can future-proof their acquisition strategies in the age of LLMs.

The evolving role of affiliates in supporting visibility, sentiment, and performance in a “no-click” world.

The fundamentals of achieving LLM visibility and best practices for optimizing financial content for LLM discovery.

Featuring:

Josh Blyskal, Answer Engine Optimization Strategy & Research, Profound

Nicky Senyard, CEO and Co-Founder, Fintel Connect

Alana Levine, CRO and Co-Founder, Fintel Connect

Whether you’re experimenting with generative AI or building your 2026 acquisition roadmap, this session will give you the practical insights-and real-world examples - to help future-proof your growth strategy and win in the age of LLMs.

Intuit and OpenAI Join Forces to Revolutionize Financial Intelligence, Powering Every Person, Business, and Dream with Personalized Experiences

Intuit, the global financial technology platform behind TurboTax, Credit Karma, QuickBooks, and Mailchimp, just announced a multi-year, strategic partnership with OpenAI to revolutionize "Financial Intelligence." This collaboration will bring Intuit's AI-driven expert platform to ChatGPT, allowing users to get secure, personalized, and "actionable financial insights and recommendations" through new Intuit-powered apps inside the chat experience. Consumers can look forward to finding the best credit cards or getting personalized tax answers, while businesses will gain access to tools that "increase revenue and profitability". Intuit is deepening its commitment to AI with a new "$100M+ multi-year contract" to utilize OpenAI's frontier models in its proprietary generative AI operating system (GenOS). The goal is to power AI agents that can "understand complex questions, surfacing insights instantly, and helping to complete tasks" like forecasting cash flow or preparing taxes through natural conversation. This major partnership aims to both deepen relationships with Intuit's existing 100 million customers and extend its reach to new audiences. [Intuit]

Klarna Strikes $6.5 Billion Loan Deal With Elliott Funds to Boost US Push

Klarna, the Swedish fintech firm and one of Europe's biggest, just struck a major deal to "boost its U.S. push," agreeing to sell up to "$6.5 billion of loans" to funds managed by Elliott Investment Management over a two-year period. The agreement allows Klarna to sell a portion of its existing Fair Financing portfolio and continually transfer newly originated receivables to Elliott funds starting in October. This strategic "forward flow agreement" provides Klarna with a "capital efficient and highly scalable funding source" to rapidly expand its buy-now-pay-later (BNPL) business in the U.S.. Klarna's Fair Financing product, which lets customers spread "large-ticket purchases into fixed monthly installments," has become "significantly popular in the U.S.," seeing gross merchandise value growth of 244% compared to 139% globally. Despite selling the loans, Klarna will retain "all consumer-facing functions, including underwriting and servicing". The company's CFO stated this deal will help them "reach even more Americans who are moving on from traditional credit and choosing fairer ways to pay". [Reuters]

JPMorgan Secures Deals With Fintech Aggregators Over Fees to Access Data, CNBC Reports

JPMorgan Chase, the largest U.S. bank, successfully secured deals with several major data aggregators, including Plaid, Yodlee, Morningstar, and Akoya, ensuring it will now receive payments for access to its customer bank account data. Data aggregators are intermediaries that link banks with fintech firms, which previously accessed customer data without paying, enabling apps to offer services like budgeting and payments. A JPMorgan Chase spokesperson stated that "The free market worked" and that the agreements make the open banking ecosystem "safer and more sustainable". These deals, which came after weeks of negotiation, involve the bank agreeing to a lower fee than initially proposed, while the intermediaries secured concessions on how the data requests are handled. This move is part of the ongoing debate surrounding "open banking" rules introduced by the Consumer Financial Protection Bureau (CFPB), which sets standards for data sharing. [Reuters]

Capital One Debit-Card Users Aren’t All Happy After the Switch to Discover

Source: WSJ

Capital One is shaking things up by moving its debit cards from the Mastercard network over to the Discover network following its acquisition of Discover earlier this year. While Capital One is banking on "considerable savings" from using its own network, some customers aren't thrilled, feeling like the switch is a downgrade because of the perception that Discover isn't as "widely accepted." Despite analysts noting that over 99% of U.S. merchants accept Discover cards, customer concerns are cropping up on social media, fueled by sporadic issues and unfamiliarity with the network. For instance, some users can't use the new cards at certain local stores or for "certain monthly subscriptions." Capital One admits that maximizing the network benefit will require investments, especially outside the U.S. where acceptance is lower, and is actively "working to expand the Discover network and address customer concerns." One key customer frustration is that Discover's debit-card network isn't accepted for all "instant transfers" in apps like Venmo, requiring customers to find workarounds. [WSJ]

Amscot Financial Partners with Green Dot to Offer Modern Banking to Customers

Source: Amscot Financial

Amscot Financial, a financial services company offering solutions through over 230 centers across Florida, announced a new partnership with Green Dot Corporation to expand its product offerings with demand deposit accounts (DDAs). This collaboration, powered by Green Dot's embedded finance platform, Arc, will bring "secure, seamless and affordable banking" services to Amscot’s customers, which includes many of the 19 million underbanked U.S. households. The new solution offers a comprehensive banking package, featuring a DDA, a "built-in secured credit card," and access to a network of "more than 25,000 free in-network ATMs." Amscot aims to enhance accessibility to "modern, affordable banking options" that help its "hardworking Floridians" build "strong financial foundations." Green Dot, which has a "long-standing commitment to supporting low- to moderate-income consumers," is providing tools that will "simplify and enhance their financial lives." [Green Dot]

Rising Rejections and Record Auto Stress Point to a Tougher Credit Cycle

Consumers are running into more closed doors when they look for credit. The New York Fed’s October Credit Access Survey shows overall rejection rates hitting a series high at 24.8%, with more borrowers calling themselves “discouraged.” Card applications nudged up and limit-increase requests matched prior peaks, but approval anxiety is doing real damage. Even households with solid incomes think they’ll be denied, creating a gap between perceived and actual rejection odds.

PYMNTS data reinforces that split. Forty-two percent of consumers doubt they’d get a new card, even though real denial rates for general-purpose cards are closer to fifteen percent for those without active accounts. Instead of taking the risk of a new inquiry, many are leaning on existing cards, asking for larger limits, or shifting toward BNPL. The Fed notes that a growing share of applications now comes from borrowers with sub-680 scores, where rejection sits above sixty percent, which helps explain why overall denials keep climbing even as card approvals hold steadier.

Source: New York Fed

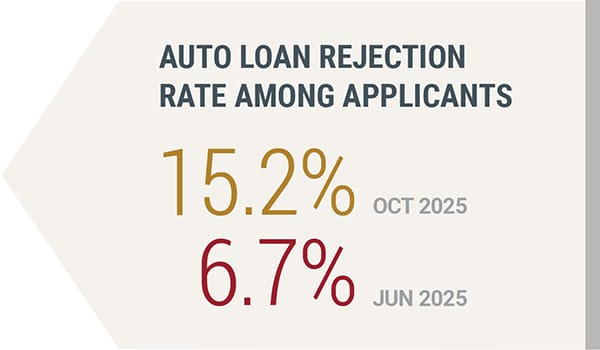

Auto credit tells the other half of the story. Fitch says subprime borrowers at least 60 days late on their car loans climbed to 6.65% in October, the highest level on record. Two subprime-focused auto lenders have already gone under, and more pressure is building as household budgets stretch. Prime borrowers remain mostly untouched, but the widening split highlights where risk is accumulating. For lenders and fintechs, the signals are aligned: demand for credit is firm, access is uneven, and consumer psychology is starting to shape the market as much as underwriting. [Reuters] [PYMNTS] [New York Fed]

Enjoying this week’s issue?

If you’ve been enjoying The Free Toaster, help us spread the word. Forward it to someone who lives and breathes lending, marketing, or fintech like you do. The best conversations in this space start with a good read.

Your shares help us reach more builders in consumer lending, and help us produce our Newsletter & Podcast.

CFES Releases Lending Standards to Strengthen Bank–Fintech Alignment and Provide Clarity in Lending Compliance

The Coalition for Financial Ecosystem Standards (CFES), an industry-led organization, just released its new Lending Module and an accompanying Lending Checklist to "strengthen bank–fintech alignment and provide clarity in lending compliance". Developed with industry leaders like FairPlay and Upstart, these standards offer "actionable guidance" across seven critical areas, translating complex lending regulations into clear frameworks for compliance and risk management. The standards are particularly timely as they address the unique challenges of technology-driven lending, providing dedicated guidance on "model risk management, validation processes, and governance frameworks" for AI and machine learning in credit decisioning. The goal is to create a "shared understanding" between bank and nonbank lenders on effective risk management and regulatory compliance. The new module builds on CFES's earlier Core Risk & Compliance Standards by adding more detailed expectations across the entire credit lifecycle, from marketing through servicing and collections, and including eight new standards for "credit model governance" and "AI explainability". This industry-led blueprint aims to create "consistency and accountability" during a time of "shifting regulatory posture". [Business Wire]

Zilch Raises Over $175 Million to Accelerate Growth

Source: Zilch

Zilch, the London-headquartered "consumer payments platform" and the UK and EMEA’s fastest-growing fintech unicorn, announced it has successfully raised "over USD $175 million" in a mix of debt and equity. This substantial raise included the expansion of its securitization led by Deutsche Bank, with the equity portion led by KKCG and participation from BNF Capital. Zilch intends to invest the new capital into "driving greater brand visibility" through increased "above-the-line (ATL) marketing spend," further product enhancement, and the "exploration of strategic M&A opportunities". The funding follows the recent launch of two major products: Intelligent Commerce, an "AI-powered platform" that has already become one of the business’s fastest-growing revenue streams, and Zilch Pay, a one-click checkout experience set to launch in H1 2026. Since its launch in 2020, the company has amassed "over 5.3 million customers" and has processed "over £5 billion of commerce" on its mission to eliminate high-cost credit. [Business Wire]

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need to accelerate your affiliate marketing? Chat with New Market Growth

Need to win on other growth channels? Chat with FIAT Growth

Growth Tracker: Earnings and New Investments

Experian reported a strong first half of FY26, with revenue from ongoing activities rising 12% at constant currency to $4.06 billion and organic revenue growing 8% as both Consumer Services and B2B gained momentum. Benchmark EBIT increased 14% to $1.15 billion, lifting margins by 50 basis points, while Benchmark EPS rose 12% to 85 cents. Consumer Services posted 9% organic growth and expanded to more than 208 million free members, and B2B grew 8% on steady demand for data, analytics, mortgage, and vertical solutions. All regions contributed, led by North America at 10% organic growth. Benchmark operating cash flow was up 25% year over year, cash conversion reached 77%, and statutory profit before tax climbed 36% to $975 million. Experian also raised its FY26 outlook to 11% total revenue growth and 8% organic growth at the top end of guidance. CEO Brian Cassin said AI-driven automation and personalization are reshaping customer experiences and internal processes, helping the business accelerate across every region. [Experian]

Klarna delivered its strongest quarter yet in Q3 2025, with revenue up 26% like-for-like to $903 million and GMV rising 23% like-for-like to $32.7 billion as active consumers climbed 32% to 114 million and merchants reached 850,000. The Klarna Card kept its rapid momentum, adding more than four million signups since July and driving 92% GMV growth, while Fair Financing GMV surged 244% in the U.S. and 139% globally. Transaction margin dollars came in at $281 million, and margin dollars based on realized losses grew 25% even as upfront provisions pulled adjusted operating results to a $14 million loss. Credit quality held firm with realized losses at 0.44% of GMV, and take rate improved to 2.76%. New partnerships with Stripe, Worldpay, Nexi, JPMorgan Payments, Walmart, eBay, and Qatar Airways strengthened Klarna’s position across major retail and commerce channels. CEO Sebastian Siemiatkowski said AI-driven automation, the scale of Fair Financing, and the explosive adoption of the Klarna Card are reshaping the company’s economics as Klarna builds toward its vision of a global digital bank in an AI-driven market. [Klarna]

Mastercard posted a strong third quarter, with net revenue up 17% to $8.6 billion and GAAP net income rising 20% to $3.9 billion, as gross dollar volume grew 9%, cross-border volume increased 15%, and switched transactions rose 10% on a local currency basis. Adjusted net income reached $4.0 billion and adjusted EPS came in at $4.38, up 13%. Value-added services delivered another standout quarter, climbing 25% on the strength of security, digital authentication, and data-driven marketing tools, while the core payment network grew 12% as rebates and incentives matched higher volumes and renewed deals. Operating income rose 26% to $5.1 billion, expanding margin to 58.8%. Mastercard ended the quarter with 3.6 billion cards in circulation and continued to invest in new capabilities, launching its Commerce Media network and new cyber intelligence products while expanding agentic commerce partnerships. CEO Michael Miebach said the company’s service portfolio and global spend trends are driving durable growth as Mastercard deepens its position across payments, data, and merchant solutions. [Mastercard]

FIS posted steady momentum in Q3 2025, with adjusted revenue up 6.3% to $2.7 billion and adjusted EBITDA rising 7.1% to $1.1 billion for a 41.8% margin, while adjusted EPS increased 7.9% to $1.51. Recurring revenue grew 6.4% across the company, and margins improved by roughly 200 basis points sequentially as Banking Solutions delivered 6.2% adjusted growth and Capital Markets accelerated to 7.6% adjusted growth with 12.6% recurring growth. Free cash flow came in at $929 million, up 75% year over year, driving a 142% adjusted FCF conversion rate and supporting $509 million in Q3 capital returns. Management raised full-year guidance for revenue, EBITDA, and cash conversion, citing stronger pricing tailwinds, resilient debit and credit spending, and renewed bank IT investment in digital, payments, and AI. CEO Stephanie Ferris said the company’s upgraded pipeline, improving recurring ACV, and expanding payments portfolio position FIS for stronger growth heading into 2026. [FIS]

FICO closed Q4 2025 with solid top-line expansion, posting $515.8 million in revenue, up 14% year over year, as Scores revenue grew 25% and Software held steady. Non-GAAP operating margin reached 54% and non-GAAP EPS came in at $7.74, up 18% year over year. Software ARR increased to $747.3 million, up 4%, while ACV bookings accelerated 48% to $32.7 million, marking the strongest quarter of the year. Adjusted EBITDA reached $286.6 million, up 18%, and free cash flow remained strong. Segment performance was led by Scores, where B2B revenue rose 29%, B2C increased 8%, and mortgage and auto originations climbed 52% and 24% respectively. Platform ARR grew 16% year over year and now represents 35% of total ARR as customers continue shifting to FICO’s modern decisioning platform. The company reaffirmed confidence heading into FY26 with guidance calling for $2.35 billion in revenue and non-GAAP EPS of $38.17. CEO Will Lansing said strong demand for Scores, expanding platform adoption, and disciplined execution are shaping another year of durable growth. [FICO]

Enova delivered another strong quarter in Q3 2025, with revenue up 16% to $803 million and originations rising 22% to $2.0 billion as combined loans and finance receivables reached a record $4.5 billion. Net income climbed to $80 million, or $3.03 per diluted share, up 93% year over year, while adjusted EPS increased 37% to $3.36 and adjusted EBITDA rose 27% to $218 million. Credit performance remained solid, with a net charge-off ratio of 8.5%, 30-day delinquencies improving to 7.2%, and the portfolio fair value premium holding at 115%. Net revenue margin came in at 57%, and liquidity totaled $1.2 billion at quarter-end. The company also repurchased $38 million of common stock. CEO David Fisher said the quarter reflected consistent demand and stable credit across both SMB and consumer portfolios ahead of Steve Cunningham’s transition to CEO in January. [Enova]

Bread Financial posted a strong third quarter, delivering $188 million in net income and $3.96 in diluted EPS, up sharply from $0.05 a year ago, as revenue held steady at $971 million and adjusted net income reached $191 million. Average loans slipped 1% to $17.6 billion, but credit sales rose 5% to $6.8 billion, driven by new partner growth and stronger spending trends across apparel, beauty, and general-purpose categories. Credit performance improved with delinquencies down to 6.0% and net loss rate easing to 7.4%, while the reserve rate fell to 11.7%. CET1 increased to 14.0%, up 70 basis points year over year, and tangible book value per share climbed 19% to $56.36. Non-interest expenses dropped 17% year over year, helped by lower impacts from prior debt repurchases and ongoing operational discipline. The company repurchased $60 million in stock across September and October and increased its authorization by another $200 million. CEO Ralph Andretta said strong capital generation, improving credit trends, and new home-category partnerships position Bread Financial for continued growth as it enters the final quarter of the year. [Bread Financial]

Looking for your next fintech role?

Stay ahead of where the industry is hiring. The Free Toaster Jobs newsletter curates standout openings in fintech marketing, product, data, and risk each week, along with insights into the trends shaping hiring across leading lenders, neobanks, and fintech startups.

Subscribe to The Free Toaster Jobs to get the latest roles and hiring insights delivered straight to your inbox (Toaster subs that don’t opt-in won’t get the Friday jobs Edition).

Missed last week’s edition? Check out the most recent job listings here.

Other News We’re Reading

(Digital Identity) Apple Introduces Digital ID, a New Way to Create and Present an ID in Apple Wallet [Apple]

(Payments / Crypto) Cash App Unlocks Bitcoin for Everyday Payments, Adds Stablecoin Support [Cash App]

(AI / Compliance) AI in Financial Crime & Compliance: Charting the Path from Pilot to Maturity, Payments & FinTech Edition [Hawk AI]

(Stablecoins) Stablecoins: How Visa’s Pilot Improves Global Payouts [FinTech Magazine]

(Identity) Trulioo Expands KYB Leadership With Launch of Credit Decisioning to Power Smarter Risk Insights [Trulioo]

(Crypto / VC) Crypto Startup Seismic Raises $10 Million to Help Fintechs Protect Customer Data [Fortune]

(Regulation / AI) Fed’s Barr Calls for Guardrails as Financial Sector Adopts AI [Bloomberg]

(Regulation) U.S. Deregulation May Spark New State-Level Rules [Fintech Global]

(Insurtech / AI) Chubb Launches AI-Powered Embedded Insurance Engine [Chubb]

(Crypto / Payments) Mastercard Adds Self-Managed Crypto Wallets [PYMNTS]

(M&A / Data) Equifax Announces Acquisition of Vault Verify [Equifax]

(BNPL / Cards) Gen Z Fuels 20 Percent Surge in Store Card Installments [PYMNTS]

(AI / Commerce) Google Augments AI Shopping With Conversational Search, Agentic Checkout and an AI That Calls Stores for You [TechCrunch]

(Digital Assets) BNY Launches Stablecoin Reserves Fund, Further Expanding BNY's Leadership in Digital Assets [BNY]

(Stablecoins / Payments) Mastercard and Thunes Bring Stablecoin Payouts to the Mainstream [Mastercard]

(Lending / SMB) From Credit Scores to Cash Flows: How Fintech Is Reshaping Small Business Lending [Empower]

Spot something worth sharing with your team? Drop this week’s edition in their inbox: https://www.thefreetoaster.com/p/intuit-taps-openai-klarna-secures-6-5b-jpmorgan-rewrites-data-terms

Catch you next week,

The Free Toaster Team

p.s. If you’re working on anything new in acquisition or credit, we’re always curious to hear about it.

About Us

Welcome to The Free Toaster! The newsletter for marketing pros at fintechs, banks, and lenders.

Inspired by the free toasters banks used to give to each new customer, we’re here to help you acquire more customers at scale. We deliver fresh news, data, and insights to help you acquire more customers, minus the breadcrumbs.

Want to follow the authors on social media?

Carlos Caro is the founder of NMG, an agency that helps lenders build affiliate programs.

Nick Madrid is the co-founder of Uncovered Media and a co-founder of Ghostmode (a media company that builds Newsletters, Podcasts, and communities in high-value B2B niches).