Last month I wrote that ChatGPT became a distribution channel for personal finance. Plaid unlocked the transaction layer, Credit Karma plugged in approval odds, and the personal finance super app started snowballing.

This aftermath of this development is less about the event itself and more about what you do with your distribution program because of it.

Here is the one idea every lending CMO needs to reorganize around. Consumers are about to delegate the decision to AI (the machine). They will arm an LLM with their transaction data, their goals, and their constraints. Then they will trust it to pick.

The old job was convincing a person to choose you: a psychological one. The new job is convincing a machine, loaded with context, to select you as the best among several reasonable options.

That one shift changes everything downstream. The game gets rational. It stops being emotional.

Your funnel survives. Your audience changes.

Good news first: the lending funnel does not disappear. Awareness, consideration, application, approval, funding: all of it still applies. However, who (or what) you are speaking to at every stage changes completely.

When an agent shops on a consumer’s behalf, it’s weighing the same things your funnel always measured. It just calls them something else, and evaluates the same questions with different logic.

How relevant is this product to this specific person? That is your click through rate.

How much information does the lender ask for, and how much do I already have? That is your application rate.

How likely is this person to actually get approved? That is your approval rate.

Your scorecard is intact. You’re simply optimizing it against a machine reader instead of a human one. Lenders who internalize that early will get a head start.

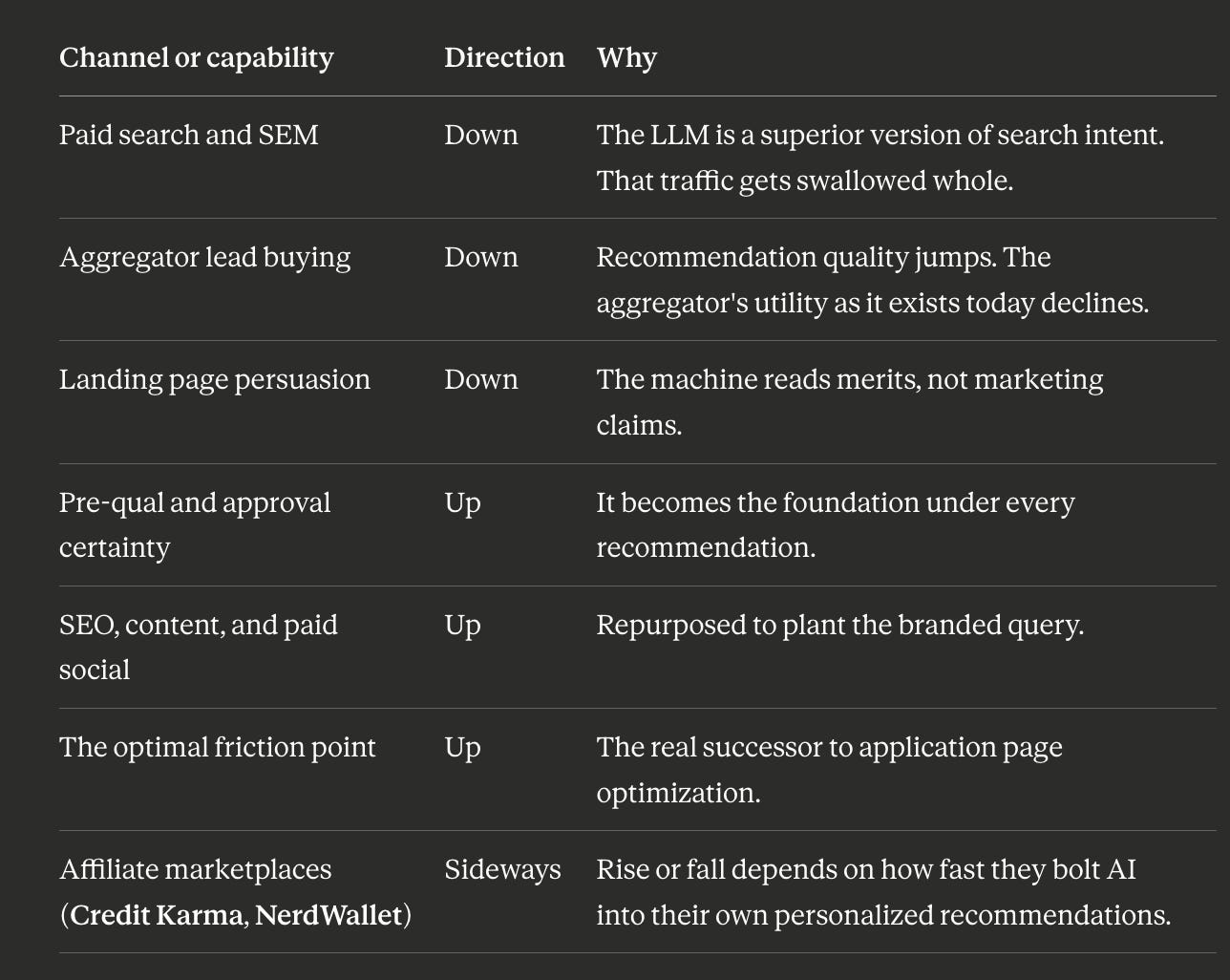

Changing dynamics in distribution channels

Here is how I see the major channels and capabilities moving.

The three “up” rows are where the real work happens.

Application page optimization is fading out. The friction tradeoff will replace it.

For two decades, the application page was sacred ground. You A/B tested button colors, trust badges, and form lengths to squeeze out conversion. When an autonomous software agent handles the form submission process, that front-end design work loses its utility.

What replaces it is harder and more valuable.

The new lever is friction management.

Specifically, how few incremental questions you ask, and how much agent supplied data you are willing to accept. A lender who says “I will take the Plaid verified income the agent already has” beats a lender who re-asks for a pay stub or W2. Less friction, higher application rate.

But there’s real tension here.

Lower friction can mean lower quality fraud and risk decisions. Accepting data you did not collect yourself is a fraud and credit risk call, not a simple UX tweak. The winning lenders are the ones who find the optimal friction point: easy enough to convert, but rigorous enough to keep fraud and bad credit out.

That tradeoff lives at the intersection of marketing, underwriting, data science, and fraud. If you already have a sharp cross functional team managing a channel like Credit Karma, that is the team. The LLM channel might just demand more of that same coordination.

The new top of funnel job is to plant the branded prompt.

This is where the emotional work of connecting to the human happens. Not on a landing page, but before the prompt itself is typed.

Picture the winning prompt.

A consumer opens their LLM assistant and says “here is my transaction data, here is what I want to accomplish, tell me what Chase has for me, then compare it to the rest of the market (unsaid: because I bank with Chase and I trust them)”

If your brand is not in that query, you are already a step behind. The agent might still surface you. But you did not earn the invitation from the human.

So a key job-to-be-done for your brand marketing is to get the consumer to invoke you by name when they put the LLM to work. You do that the only way you ever could. By being genuinely useful. Educate, entertain, inspire, and be trustworthy enough to be memorable.

There is no shortcut into the prompt.

Feed the super app. Do not try to become it.

Most lenders will wonder if they should build the super app themselves. I don’t think they should.

I would not trust a financial products super app built by a Fortune 500 bank brand. Neither would you. We would read it as self-serving, a storefront dressed up as an advisor. The trust goes to the independent brand that charges me a subscription and promises objective, data-based recommendations for my specific situation.

I think the winning LLM surface in financial services is subscription funded, not ad funded. The moment recommendations are paid for by advertisers, consumers will assume the payout shaped the answer. A surface that consumers pay for is a space they can trust.

So the lender’s job is not to win the surface.

It is to be the offer the surface picks. Feed the super app your real terms, your certainty, your machine readable offer, and your brand.

The machine is going to do the rest.

A key assumption

This whole thing depends on consumers handing an LLM the keys to their bank and bureau accounts.

I’m betting they will.

Consumers already gave their accounts to Mint a decade ago and to Monarch today. Mint had 20 million registered users at its peak, built on nothing but a spreadsheet in the cloud and a promise to make sense of your money. When people see value in sharing data, they share it.

The open question is which brand earns the finance-specific trust. Maybe it’s ChatGPT or Claude.

Maybe a purpose built finance assistant has to emerge first. The timing depends entirely how long it takes the provider to earn the trust.

I’m guessing we’ll start to see really kick-ass apps like this (with 5M+ consumer scale), in the next two years.

The one move to make this quarter

If you do one thing, start building your brand.

Too many fintech-lender CMOs are addicted to arbitrage. Spend a dollar on paid search, paid social, or an affiliate placement. Make two back. That muscle is going to atrophy, because the LLM is built to be immune to it.

Think about what LLMs do well: processing a mountain of information to make an objective, data-based decision.

Media arbitrage does the opposite.

It interrupts the consumer to put your thing in front of them and hopes proximity and clever copy sways the choice. LLMs are engineered to ignore exactly that.

Attention is getting harder to buy.

The assets that earn it are a brand the consumer already trusts and an offer that genuinely wins on merits. Both take years or decades to build.

Closing thoughts

No channel is safe forever.

Direct mail held up for five decades, and it’s at risk in a world where AI makes product recommendations frictionless and accurate.

I’m not telling you to kill anything today. What I am saying is to expect legacy channels to deteriorate slowly as humans start figuring out helpful LLMs will be in the context of shopping for financial products.

The lenders who win will stop trying to convince the human, and shift their energy toward winning the agent the human sends in their place.

The marketing funnel is the same, but your (new) buyer is a machine (or a human with a strong bias for doing what the machine says). And the only durable advantage is being the best real answer to the question the consumer actually asked.

That’s where the game is going now.