How Dave Scaled to $163.7M in Q4 Revenue After Nearly Being 'Left for Dead'

Plus, Spinwheel becomes a CRA, Robinhood's "Actual" Platinum Card, and much more...

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

We’ve got a packed edition for you this week, starting with Dave’s Q4 results where quarterly revenue jumped 62% to $163.7 million. While Dave rebounds, the traditional credit system may be showing cracks; a new analysis from ProPublica, a non-profit investigative newsroom, reports that Experian, TransUnion, and Equifax are increasingly failing to correct errors on consumer credit reports. Meanwhile, the race for premium users is heating up with Robinhood’s new Platinum card, and Chime is aggressively rewiring its operations by using AI to handle 70% of member support. We’re also looking at the dawn of agentic commerce as Mastercard, Google, and Affirm build the framework for AI assistants to safely handle your shopping.

Lots to break down. Let’s get toasting!

— Carlos Caro, Founder at New Market Growth

— Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please ask 1 of your colleagues to subscribe!

How Dave Went From "‘Left for Dead’ to $554M in Annual Revenue

Dave, a neobank that provides mobile cash advances and banking services, finished Q4 2025 with revenue up 62% to $163.7 million and a 50% increase in loan originations, signaling a period of continued growth for the platform. Full-year 2025 revenue hit $554 million, capping a turnaround that would have seemed absurd two years ago. In 2023, Dave's stock was trading under $10 after a SPAC debut that cratered over 90% from its peak. The company was burning cash, cutting staff, and widely written off as another pandemic-era fintech flameout. Net income for the quarter rose 292% to $66.0 million, which suggests the business model is finding its footing. While Monthly Transacting Members (MTMs) reached 2.9 million, CEO Jason Wilk noted this is still a "small fraction" of the 185 million people in their target market. Management also increased the share repurchase authorization to $300 million to return capital to investors. For 2026, Dave expects revenue growth between 25% and 28% along with expanding profit margins. (Dave)

Digging Deeper

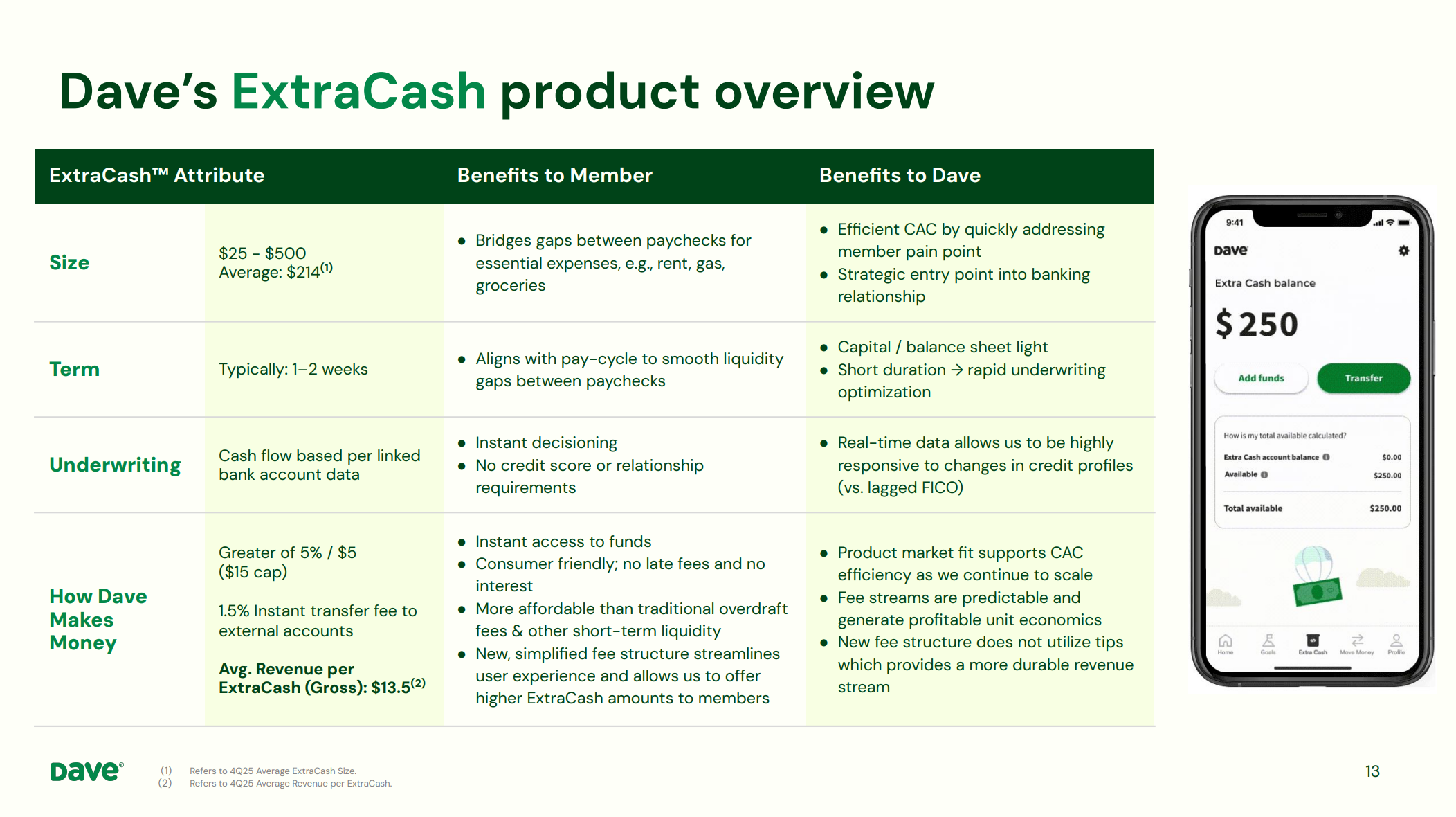

Management now talks a lot about their “growth algorithm”. The result: mid-teens MTM growth plus low double-digit ARPU growth. In 2025, both components outperformed. MTMs accelerated to 19% year-over-year, reaching 2.93 million. ARPU grew 36%, driven by a new fee structure that replaced the old tip-based model with a flat 5% fee (capped at $15) on ExtraCash advances.

Here’s where it gets interesting for marketers.

Dave acquired 867,000 new members in Q4 at a $20 CAC. But the company doesn’t optimize for lowest CAC. It optimizes for gross profit per member. Annualized gross profit per MTM hit $167, up $48 year-over-year, while CAC only moved from $16 to $20. Payback periods dropped to under 4 months.

How Dave Will Partner With CCB

Dave is moving ExtraCash receivables off-balance sheet through Coastal Community Bank. Receivables sat at $297 million at year end against $2.2 billion in quarterly originations. Once migration completes by mid-2026, Dave expects to free up $200 million-plus in liquidity and retire its $75 million credit facility.

Dave keeps full economic exposure but pays Coastal to hold the assets. The fee reduces non-GAAP gross profit but gets added back for EBITDA.

Dave Running BNPL Experiments

Dave is testing a BNPL product internally and expects customer testing in April. Limits will run 50% to 2x larger than ExtraCash. No compound interest, no late fees, CashAI underwriting.

Management expects some ExtraCash cannibalization but sees the products as complementary. ExtraCash covers bills, gas, groceries. Pay-in-4 targets discretionary spend where members already use competing BNPL products. Even if it monetizes at a lower rate, Wilk says the longer retention and higher LTV make it a net positive. It also opens a new acquisition channel. BNPL is an easier marketing message than cash advances.

No meaningful BNPL revenue expected in 2026. The focus is proving the unit economics before scale in 2027.

Wrapping Up

Dave’s 2.9 million MTMs sit at roughly 1.6% of what it estimates is a 185 million person TAM. The earnings supplement shows 66% of Americans now live paycheck to paycheck (up from 57% in 2021) with personal savings rates at 4%, half the pre-COVID level. Structural demand for short-term liquidity keeps expanding.

The cost advantage over legacy banks is notable. Per Dave’s management team, their cost to serve runs $56 per customer versus $300 at legacy banks. CAC is $19 versus roughly $500. Fewer than 300 employees, no branches, $2.3 million in annual revenue per employee (up from $1.5 million a year ago). Revenue per employee climbing while headcount stays flat is what AI-driven operations look like when the product and the underwriting model are the same thing.

Dave beat and raised every quarter in 2025. The 2026 guide implies deceleration from 60% to roughly 26% growth, which builds in room to do it again.

The DOJ still has an active case against Dave, alleging the company’s tipping model misled consumers about the true cost of its cash advances. The suit, filed in 2024, claims Dave pushed users toward tips that functioned more like hidden fees. A loss or settlement could force product changes and carry financial penalties. That risk hasn’t gone away. But $227 million in FY25 adjusted EBITDA from a company that was nearly left for dead two years ago may buy them a little extra time.

Sponsored by Spinwheel

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

The Free Toaster Podcast takes the biggest fintech, credit, and payments stories of the week and breaks down what they mean for growth, distribution, and product strategy. If you read the newsletter, this is the conversation behind it.

Listen on Apple Podcasts, Spotify, Substack, or wherever you get your podcasts.

Be sure to check out our latest pod!

(And if you have a strong opinion on anything in today’s Edition and would like to be on the show - we record at 1:30pm ET on Fridays - reply to this email to let us know!)

Credit Bureaus Are Leaving More Mistakes on Frustrated Consumers’ Reports Under Trump’s CFPB

ProPublica, a non-profit investigative newsroom, reports that Experian, TransUnion, and Equifax are increasingly failing to correct errors on consumer credit reports. These companies generate revenue by collecting and selling financial data, yet a ProPublica analysis indicates they now provide relief to consumers roughly half as often as they did in previous years. Under current federal oversight, the Consumer Financial Protection Bureau has drastically curtailed its enforcement, and the rate at which Experian resolves disputes fell to less than 1% compared to nearly 20% just one year ago. TransUnion also saw its relief rates plunging starting in mid 2025 as the companies changed how they handle consumer complaints. The bureaus attribute these shifts to widespread misuse by credit repair firms, but this change in policy often leaves individuals with documentation of errors unable to fix their scores. Without active regulatory pressure, many consumers remain trapped with incorrect data that prevents them from securing housing or loans. (ProPublica)

Toaster’s Question To Our Readers: It strikes us that as complaint volume increases, a higher % of those complaints might come without merit or justification. We’d love to unpack this further. In anyone in our audience close to this trend and willing to come on the Podcast to discuss? Reply to this email to let us know.

Why Spinwheel Chose to Become a Consumer Reporting Agency

Spinwheel recently transitioned into a consumer reporting agency, a move that changes how the debt and liability data aggregator handles financial information. The company operates a platform that helps lenders and fintechs access fragmented credit data to assist with underwriting and account management. By adopting this status, Spinwheel now follows the Fair Credit Reporting Act to address a substantial gap between modern data tools and traditional credit bureaus. This shift requires the company to maintain rigorous accuracy standards and provide formal dispute processes for users. Lenders can now integrate this data into regulated decision-making workflows with greater regulatory alignment. Sean Anderson, the company's Chief Operating Officer, stated that operating as a consumer reporting agency allows them to bridge that gap by delivering more comprehensive liability intelligence. Consumers potentially see better loan rates when financial providers use more accurate, consumer-permissioned data. (Spinwheel)

Looking for some sunshine, good vibes, and even better fintech discussion this April?

The Free Toaster will be at CardCon in Phoenix and would love for you to join us! The schedule just dropped and promises a wide range of marketing and AI topics.

How Robinhood’s New $695-a-Year Credit Card Stacks Up in a Crowded Market

Robinhood Markets is entering the premium credit card market with a new product that attempts to challenge Amex’s flagship product. The digital brokerage operates a platform for stock trading and retirement accounts and now wants to attract a demographic of higher spenders. This new card carries a $695 annual fee and offers various cash-back incentives for travel and dining. Critics point out that some of these benefits require specific spending hurdles or additional purchases to actually function. Robinhood aims to convert its existing app users into cardholders to compete with established players like American Express and Chase. CEO Vlad Tenev described the card as being annoyingly heavy at a recent launch event. The strategy relies on the high engagement levels of current brokerage customers who already check the app frequently. (WSJ)

When AI Starts Buying For You, Trust Becomes The Product

Mastercard recently collaborated with Google to launch Verifiable Intent, a new technical framework designed for AI-driven commerce. This global payments company provides the infrastructure that allows AI agents to buy products for users without a manual click for every transaction. Since industry experts describe the adoption of these agents as skyrocketing, the company wants to ensure digital assistants do not exceed their spending authority. They are building a record intended to be tamper-resistant that links user identity and specific instructions to every transaction the AI makes. This move aims to keep autonomous purchases authorized and secure. It essentially gives everyone a shared source of truth so merchants know the bot has permission to spend money. If we are going to let bots handle our errands, we need to know they are sticking to the script. By open-sourcing the technology, they are inviting other developers to help build out the standards for agentic commerce. (Mastercard)

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Happy Money Introduces Partner-Branded Program to Help Credit Unions Drive Lending and Membership Growth

Happy Money launched its Partner-Branded Program to help credit unions and banks manage personal loan offerings without building their own internal systems. As a consumer finance finance company, Happy Money operates a lending platform called Hive that connects individual borrowers with loans funded by various financial institutions. This new setup lets partners like MSU Federal Credit Union offer loans under their own brand while Happy Money handles the behind-the-scenes marketing and loan management. The program aims to help local institutions find new borrowers and maintain member loyalty as traditional acquisition costs rise. MSU Federal Credit Union currently uses the system to reach people through direct mail and digital ads to fuel its lending activity. Happy Money manages the underwriting and servicing, which allows these credit unions to add high-yield assets to their portfolios with less operational work. The company has originated more than $6.5 billion in loans since it started, showing a substantial reach in the digital lending space. It is an interesting move because it lets smaller lenders use outsourced tech to compete for personal loans that usually require a significant investment in digital infrastructure. (PR Newswire, Happy Money)

Chime Is Using AI To Rewire How Brands Show Up In Culture

Chime recently announced a multi-year partnership with Major League Soccer, acting as the league's official retail banking and credit card partner. This digital banking platform provides fee-free financial services and now uses internal AI tools to manage its branding and customer outreach. Chief Growth and Marketing Officer Vineet Mehra moved creative production in-house, using AI to reduce campaign development timelines by 60%. The company also replaced its creative agency of record with these automated tools. Mehra estimates AI will save the company millions in agency costs over the next couple of years. On the operational side, AI now handles 70% of member support interactions through voice and chat systems. These efficiencies dropped the cost to serve customers by 60% while reducing repeat inquiries. By automating repetitive tasks, Chime reallocates its budget toward high-profile sports sponsorships to reach younger, digitally active consumers. (Forbes)

Klarna and Stripe Team up to Offer Flexible Payments and Seamless Processing Globally

Klarna and Stripe recently expanded their long-standing partnership to make flexible payment options more accessible to small and medium businesses globally. As an AI-powered payments network and shopping assistant, Klarna provides buy now, pay later services and instant bank transfers for over 100 million customers. This updated integration allows Stripe users in 25 countries to add Klarna to their checkout flows without a complex technical setup. The data shows some merchants experienced a substantial 67% increase in average order value after adopting the service. Stripe provides the underlying payment processing and reliable security that keeps transactions moving during high-volume periods like Black Friday. By upgrading their shared API, the two companies now offer a seamless experience that mirrors a direct integration. This move helps Klarna move beyond its traditional roots in fashion and beauty into new areas like healthcare and auto repair. Both companies seem focused on making it easier for shoppers to choose how they pay while helping merchants track those sales more effectively. (Klarna)

Affirm Expands Stripe Partnership to Support Shared Payment Tokens for Agentic Commerce

Affirm is expanding its partnership with Stripe to integrate its installment lending service into AI-driven shopping platforms. Affirm operates a payment network that offers fixed-term loans for consumer purchases without charging late fees. The new technical setup uses Shared Payment Tokens, which allows AI agents to suggest and initiate purchases with a user's permission. By using these tokens, the system avoids exposing sensitive account credentials during the transaction process. Shoppers see the total cost of their purchase upfront and select a specific repayment plan before the AI assistant completes the buy. Stripe handles the backend processing between the merchant and the lender, even for businesses that do not use Stripe as their primary payment processor. This move follows a collaboration that began in 2021 and aims to standardize how pay-over-time options function within automated commerce. While the tech is evolving, the core goal remains providing a clear payoff date for individual transactions rather than a revolving credit line. (Affirm)

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(AI) Splitit and Google Prepare Installment Payments for AI Shopping Agents (PYMNTS)

(AI) TransUnion Advances AI-Driven Credit Intelligence with Google Cloud (TransUnion)

(Fintech) Current And Former Block Workers Say AI Can’t Do Their Jobs After Jack Dorsey’s Mass Layoffs: ‘You Can’t Really AI That’ (The Guardian)

(Lending) Gradbridge Launches Second-Look Private Student Lending Program And Partnership With Hatch Bank (PR Newswire)

(Lifestyle/Travel) American Express Opens First-Ever Sidecar By The Centurion® Lounge (American Express)

(Crypto/Banking) Zerohash Applies For A National Trust Bank Charter To Further Strengthen Regulated Stablecoin & Digital Asset Infrastructure (GlobeNewswire)

(Fintech/Banking) Revolut Seeks US Banking License As Fintech Eyes Expansion (Bloomberg)

(Fintech/Banking) Tech And Finance Layoffs: Oracle, Block, Morgan Stanley, Capital One Headline Brutal Week For Job Losses (Fast Company)

(Payments) Strategic Imperatives Expands Gocardless Integration To Automate End-To-End Billing And Disbursements (GoCardless)

(Cards) Talucard Launches New Biometric Payments Card With Idex Biometrics (FinTech Futures)

(Payments) Sofi And Mastercard Partner To Enable Sofiusd Settlement Across Mastercard’s Global Payments Network (Mastercard)

(Payments/Saas) Stripe Thinks The Subscription Model Needs A Usage-Based Upgrade (PYMNTS)

(Cards) Capital One Ignites Competition With Shift To Discover Network (PYMNTS)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/how-dave-scaled-to-1637m-in-q4-revenue

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.