Chime S1: Why Their Flywheel is So Fly

Reverse-Engineering Chime's Success: Unpacking Their ARPAM-Boosting Strategies

Housekeeping Note

We send a separate jobs edition at the end of the week. You can always view it at thefreetoaster.com or, click here if you want to receive the jobs edition via email

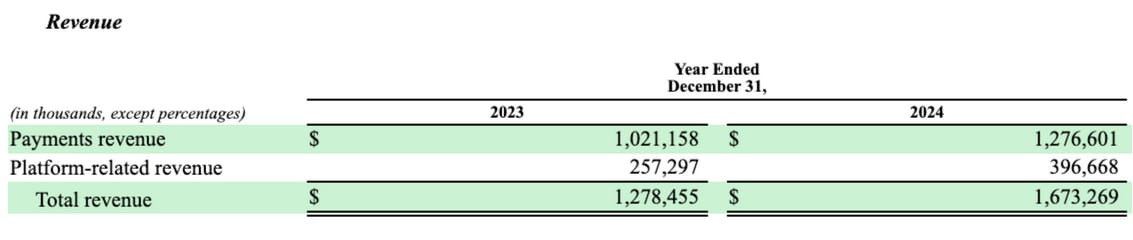

Chime, the digital bank known for its no-fee consumer financial products, officially filed its IPO paperwork, revealing strong growth. Revenue soared to $1.67 billion in 2024, while losses shrank to just $25 million—down from $203 million in 2023. With $519 million already banked in Q1 2025, Chime looks poised to hit $2 billion this year and flirt with profitability. Investors may be circling, but the S-1 still leaves plenty of blanks, including share pricing and insider sell-offs. [TechCrunch] [BusinessWire] [S1 Filing]

/

Chime’s ARPAM Machine

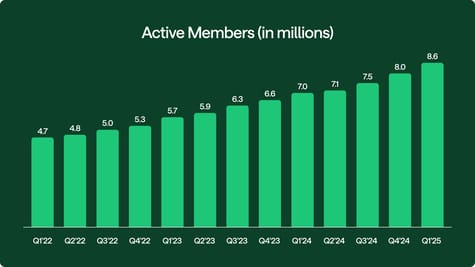

Chime is not just a “neobank” or a slick app for the underbanked. It’s a $115 billion purchase volume engine (as of 2024), quietly eating the lunch of incumbent and regional banks, one direct deposit at a time. In fact, its 2024 purchase volume was surpassed by only five other U.S. debit card issuers.

But here’s the real play: Chime isn’t just winning on acquisition. They’re building a flywheel that systematically increases Average Revenue per Active Member (ARPAM)—and it’s not an accident. It’s the result of distribution-first thinking, relentless product attach, and a willingness to do the unsexy work that most fintechs ignore.

Let’s break down how the machine works—and why every fintech marketer should be taking notes.

The Chime Business: Facts and Figures

Chime’s core business is simple: capture your direct deposit, become your “top-of-wallet” card, and monetize the hell out of your everyday spend.

Interchange is the engine, at least for now.

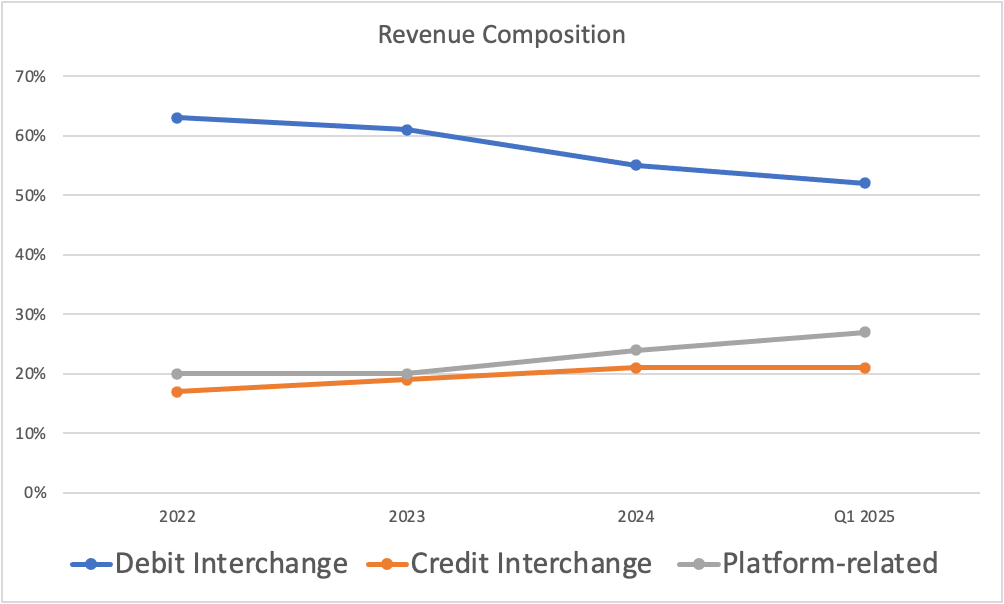

In 2024, Chime processed $115.2 billion in purchase volume with 8.6 million active members. This payment-driven revenue, primarily interchange fees, accounted for 76% of total revenue in 2024 and 72% in Q1 2025. While debit cards drove the bulk of this volume (84% of Purchase Volume in Q1 2025), their strategic push for products like Credit Builder (its secured credit card) is critical.

Although a smaller portion of volume (16% in Q1 2025), credit card transactions generate higher interchange rates and significantly impact revenue, with credit interchange (Credit Builder) making up 21% of revenue in Q1 2025. To put Credit Builder's impact in perspective, in 2024 alone, it generated $18.4 billion in Purchase Volume and $358.4 million in revenue.

Platform-related revenue is also growing, from 24% of total revenue in 2024 to 28% in Q1 2025.

Data from S1 Filing

Data from S1 Filing

But the real story isn’t just the volume. It’s the depth of relationship with members.

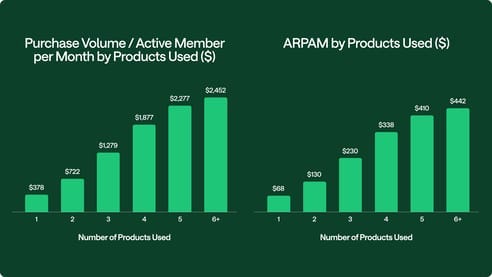

Chime’s ARPAM hit $251 in Q1 2025—up a 6% average annualized growth rate (CAGR) since Q1 2022. Members who use six or more Chime products? They generate 1.8x the ARPAM and significantly higher purchase volume compared to the average member (as seen in Q1 2025).

This is the compounding effect of funnel efficiency and product attachment. Every step multiplies the next. Chime isn’t just acquiring users—they’re stacking products, data, and engagement to drive up ARPAM cohort after cohort.

Customer Acquisition: The Referral Flywheel

Here’s where most fintechs get stuck: they spend a fortune on paid channels, then watch CAC spiral as they chase the same Google/Facebook audience as everyone else.

Chime’s approach is different. Since 2022, over half of new Active Members are acquired through organic and member-driven channels—word of mouth, referrals, and peer-to-peer payments via Pay Anyone. In 2024, referrals became Chime’s single largest acquisition channel. This organic pull is powerful: a 2024 survey showed Chime captured 17% of new or switching direct deposit relationships among adults earning up to $100,000.

Why does this work? Because Chime’s core product actually delivers on its promise: faster paychecks, no hidden fees, and real liquidity when you need it. 85% of new members who set up direct deposit came from an existing bank. 97% of members say Chime “unlocked their financial progress.” That’s not just marketing fluff—it’s the foundation of a viral loop.

And the economics show it. Acquisition cost per new Active Member was $109 in 2024 (just $91 excluding broader brand marketing), with payback in about 7 quarters for 2022 cohorts, and even faster for Q1 and Q2 2023 cohorts.

The kicker: members who use more products refer more new members. Those with six or more products referred 1.6x as many friends as the average. The product flywheel drives the referral flywheel, and vice versa.

Retention: The Compounding Game

Chime’s retention stats are the envy of the fintech world. Approximately 50% of Active Members are retained through their first year (for those active 2016-2023), and around 90% of those remaining Active Members continue each year thereafter. But the real magic is in the dollar retention: approximately 97% net dollar Purchase Volume retention and, crucially, an astounding ~104% net dollar transaction profit retention for the year ended March 31, 2025. This means retained customers are becoming more profitable over time.

Why so sticky? Because Chime is not a “sidecar” account. Once they get your direct deposit, they’re your primary bank. That means recurring, non-discretionary spend—food, gas, utilities—making up 70% of transactions. This isn’t the “cherry-picking” problem that kills most challenger banks. Chime is the hub, further evidenced by high engagement: Active Members interacted with the app 141 times per month in Q1 2025.

And as members stick around, they adopt more products. In March 2025, the average Active Member had 3.3 Chime products. The product attach rates speak volumes (as of March 2025): Debit Card at 90%, High Yield Savings at 69%, Pay Anyone at 54%, SpotMe at 49%, Credit Builder at 37%, and MyPay at 26%. The more products, the better the economics: higher ARPAM, higher retention, higher referral rates.

The ARPAM Engine: MyPay, SpotMe, Instant Loans

Let’s talk about how Chime actually drives ARPAM up and to the right.

MyPay

Launched fully in July 2024, MyPay is instant earned wage access—get paid as soon as you clock out. By March 31, 2025, members had accessed $8.8 billion via MyPay. The attach rate hit 26% of Active Members using it monthly by March 2025. MyPay is a platform revenue monster, contributing $106 million to Chime's platform-related revenue growth in 2024. The economics? MyPay advances are typically repaid in under 14 days. While risk losses were below 1.75% of total dollars advanced from launch through Q1 2025, Chime noted that transaction and risk losses increased in Q3/Q4 2024 and Q1 2025 due to the full launch, contributing $54.2 million to this increase in Q1 2025 – a factor they are actively managing. Chime’s privileged repayment position (they see your paycheck first) lets them offer liquidity with minimal relative risk. That’s a moat.

SpotMe

SpotMe is Chime’s “no fee overdraft”—but really, it’s a short-term liquidity product dressed up as a feature. Since its 2019 launch through March 31, 2025, members have accessed $43.3 billion through SpotMe. 49% of Active Members used it monthly in March 2025. It even includes "SpotMe Boosts," a community feature allowing members to temporarily increase each other's limits. SpotMe advances are typically repaid in under 7 days, with risk losses impressively held below 0.40% of total dollars overdrawn (from 2022 through Q1 2025). Members can even “tip” Chime for the service, which shows up as platform revenue. The kicker: SpotMe and MyPay aren’t just features—they’re ARPAM accelerators. They increase engagement, retention, and cross-sell. And because Chime sits on top of the paycheck, they can price risk tighter than almost anyone.

Instant Loans

This is the next frontier. Instant Loans are small-dollar, short-term credit—think $100–$500, repaid on your next deposit. It’s asset-light (Chime’s bank partner, Bancorp, committed to retaining receivables and funding the loans), data-rich (Chime sees your income and spend in real time), and risk-managed (privileged repayment, short duration). As Chime scales Instant Loans, expect ARPAM to ratchet up even further. These products monetize the core distribution advantage—direct deposit—by layering on high-margin, high-attach products that competitors can’t easily copy.

Why Chime’s Model Works (and Most Don’t)

Chime is playing a different game than most fintechs. Here’s what sets them apart:

Distribution-first product design. They build for the channel (direct deposit, top-of-wallet), not for hypothetical “features.”

Funnel efficiency compounds. Every product attaches to the next, driving up ARPAM and lowering CAC via referrals. This is clear with an average of 3.3 products per active member and engagement like 141 app interactions per month.

Privileged data and repayment. Chime sees your paycheck, your spend, and your network. They can underwrite and cross-sell with an edge.

Unit economics at scale. 88% gross margin, 67% transaction margin, and the critical ~104% net dollar transaction profit retention. These are numbers most fintechs can only dream of.

Flywheel in motion. More products = higher ARPAM, higher retention, more referrals, more data, more products. The loop gets stronger every year.

The Takeaway for Fintech Marketers

If you’re building in fintech and you’re not thinking about ARPAM, you’re missing the plot. Chime’s model shows what happens when you align distribution, product, and data, then use that foundation to launch products that actually matter to your members.

The lesson isn’t “build another neobank.” It’s this: treat your acquisition channel like a living organism, build for deep product attach, and design every new feature to increase ARPAM, not just usage.

Chime’s not perfect, but they’re running the playbook at a level most fintechs haven’t even attempted. The opportunity is still huge—Chime targets an estimated $86 billion annual revenue opportunity with its current products for the 196 million Americans earning up to $100,000 annually, and they estimate they've penetrated less than 3% of this market. The product roadmap is just getting started.

If you’re not reverse engineering your ARPAM flywheel, you’re playing the wrong game.

Note: We’ve narrowed our analysis to things we know are important to fintech marketers. The newsletter Cautious Optimism also published a good piece on Chime today.

2nd note: A member of the Toaster team was a former Chime employee and owns equity in the company.

We couldn’t produce this newsletter without our sponsor (and friends) at Spinwheel (a QED-backed fintech)

Reduce friction in your lending application with only two required fields: phone number and birthdate! Seamlessly access real-time credit data and payment processing, and watch your application rates jump by 20-30%. Get started today!

Support The Free Toaster

Need to improve application page conversions? Chat with Spinwheel

Need to accelerate your affiliate marketing? Chat with New Market Growth

Need to win on other growth channels? Chat with FIAT Growth

None of the above? Share our Newsletter in your favorite Slack channel

About Us

Welcome to The Free Toaster! The newsletter for marketing pros at fintechs, banks, and lenders.

Inspired by the free toasters banks used to give to each new customer, we’re here to help you acquire more customers at scale. We deliver fresh news, data, and insights to help you acquire more customers—minus the breadcrumbs.

Want to follow the authors on social media? Find Nick Madrid and Carlos Caro on LinkedIn.