Cash App to Sell its Credit Score

Block is (attempting to) monetize the financial habits of 58 million monthly users, offering third-party lenders a unique view into the underbanked that traditional credit bureaus often miss.

Hey Toaster Readers,

This week is sponsored by our friends at Fintel Connect.

We’re looking at why Cash App thinks its ecosystem could be a better judge of credit than the big banks. Block, it’s parent company, is officially launching a waitlist for lenders to buy its internal consumer credit scores, betting that real-time data from Afterpay and Cash App Borrow is more predictive than a traditional FICO.

Credit Unions are arming themselves with AI to level the playing field. Between First Financial of Maryland’s new partnership with Scienaptic AI and the launch of the CU Lending Collective by Commonwealth and Zest AI, smaller institutions are finally getting the tools to compete with national lenders. We also have a must-read update on a sophisticated social engineering attack at Figure and a heated legislative battle in Oregon over a proposed 36% interest rate cap.

Lots to break down. Let’s get toasting!

— Carlos Caro, Founder at New Market Growth

— Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please share our Newsletter in your internal Slack channels!

Cash App to Sell its Credit Score

Block, the digital payments firm behind Cash App, just launched a waitlist for lenders interested in buying its internal consumer credit scores. By analyzing data from its buy now, pay later service Afterpay and its Cash App Borrow feature, the company provides a window into how people handle non-traditional finance. This move targets a massive audience, as Cash App reports 58 million monthly active users who often skip traditional banks. While Block is not disclosing the exact price for this data yet, it is already talking to several parties about integrating the scores into their underwriting processes. The expansion follows a period where the firm loaned consumers more than $100 billion since 2022. This strategy reflects a broader shift in the market, as players like Experian and FICO also began tracking installment loan data recently. Block is betting that its unique view of borrower behavior will be a valuable asset for third-party lenders looking to reach a younger demographic. (Payments Dive)

Making Sense of What’s Going On

Prithvi Prabhu, a Free Toaster reader, helped us make sense of this story in last week’s News Pod.

Block is selling a unique view of the underbanked, but Prithvi suggested this view might be through a filtered lens. A 97% repayment rate for sub-580 FICO borrowers looks like a fintech miracle on a slide deck — the reality, though, is more mundane.

The Short-Term Trap

The fundamental issue is duration mismatch. Cash App Borrow is a three-week cash advance, not a multi-year installment loan. Prithvi pointed out that in the payday and cash advance world, a 97% repayment rate is actually pretty ordinary. Comparing that to a FICO score designed for an 18-month horizon is like judging a marathon runner’s stamina based on their first 100-meter dash.

The Lagging Disaster Risk

There is a specific danger for lenders eyeing Block’s claim of approving 30% more auto loans at identical loss rates. If those lenders use short-term data to underwrite multi-year debt, the early results will look fantastic. This often leads to doubling down on volume just before the long-term risk surfaces 6–9 months later. We’ve seen this movie before, lenders building models on payday data often end up with a massive book of bad loans once the honeymoon phase ends.

The Structural Ceiling

Beyond the risk, there are two major hurdles for Cash App’s scoring ambitions:

Pre-screening: Credit bureaus allow lenders to target creditworthy people before they apply. Cashflow data requires the user to already be in the ecosystem, making it an ancillary tool rather than a FICO killer.

The Recession Test: Cash App’s data hasn’t survived a true, sustained recession. Its 580-FICO user base is historically the most vulnerable during a downturn, and we don’t yet know how that 97% repayment holds up when the macro environment truly sours.

Block is successfully productizing its ecosystem, but for third-party lenders, buying these scores might mean buying into a short-term signal that lacks long-term staying power.

Big shout out to Prithvi for helping us contextualize this story!

The Free Toaster Podcast takes the biggest fintech, credit, and payments stories of the week and breaks down what they mean for growth, distribution, and product strategy. If you read the newsletter, this is the conversation behind it.

Listen on Apple Podcasts, Spotify, Substack, or wherever you get your podcasts.

Be sure to check out out our latest pod!

(And if you have a strong opinion on anything in today’s Edition and would like to be on the show - we record at 12pm ET on Fridays - let us know!)

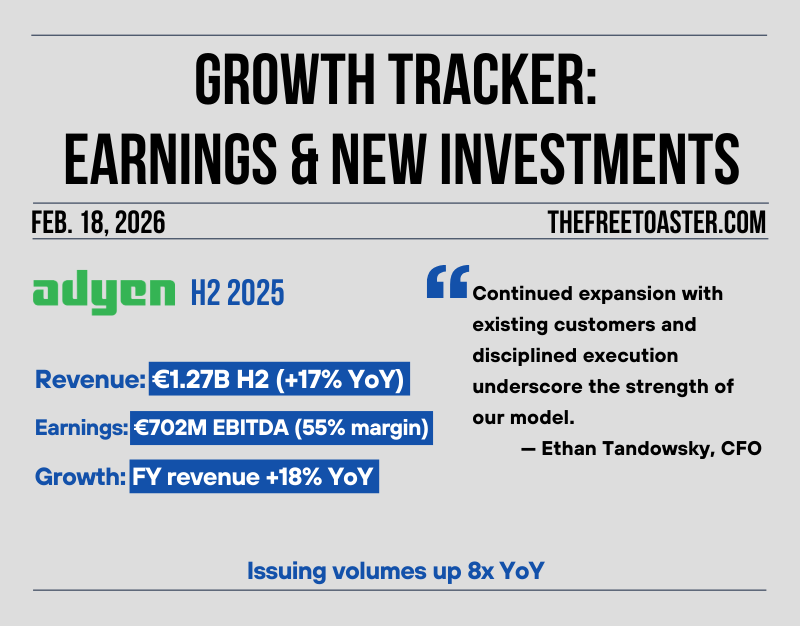

TransUnion Announces Strong Fourth Quarter and Full-Year 2025 Result

TransUnion reported its fourth quarter results with revenue climbing 13% to $1.17 billion. The company exceeded its own financial guidance, supported by a 16% revenue increase in its U.S. Markets segment. Much of this growth came from the financial services sector, which saw a 19% surge. For the full year 2025, the company brought in $4.58 billion in total revenue, up 9% from the previous year. TransUnion also bought back $300 million in shares over the course of the year and increased its quarterly dividend to $0.125.

The company issued a 2026 forecast expecting revenue growth between 8% to 9%. CEO Chris Cartwright attributed the recent momentum to a multi-year strategy involving credit and fraud solutions. Cartwright stated, “TransUnion finished the year strongly with results that again exceeded financial guidance,” noting that commercial momentum is driving the business. While the firm is watching variables like inflation and interest rates, it plans to detail its technology updates at an upcoming Investor Day. (TransUnion)

First Financial of Maryland Federal Credit Union Adopts Scienaptic AI to Automate Credit Decisions

First Financial of Maryland Federal Credit Union, a member-focused institution managing over $1.3 billion in assets, teamed up with Scienaptic AI to update its lending process. First Financial serves over 77,000 members and wants to ensure that every member feels understood and supported while modernizing its credit decisions. By plugging in the Scienaptic AI platform, a tool for automated credit decisioning, the credit union can now analyze more data points to approve more loans while managing risk. Scienaptic AI already supports decisions for over $250 billion in loans and specializes in helping lenders reach underbanked communities through machine learning. This partnership aims to increase speed and consistency while maintaining the member-first focus of the credit union. It represents a shift for the Maryland community because these analytics help people access credit who might have been overlooked by traditional methods. After all, banking is a lot more practical when the software actually helps you get the green light on your next loan. (Scienaptic AI)

Want To Reach Our Readers In Person?

The Free Toaster is betting big on live events in 2026.

If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. Think coffee meetups, lunches, dinners, 1-day events, golf outings, wine tastings.

Our events team can help you bring it to life. Contact amanda@thefreetoaster.com for more information.

Commonwealth Credit Union and Zest AI Partner to Launch CU Lending Collective

Commonwealth Credit Union, a financial institution that provides banking services to its members, is partnering with Zest AI, a company that develops automated underwriting software, to launch the CU Lending Collective. This new organization aims to help smaller credit unions implement automated lending tools without the high costs or operational hurdles usually found with this technology. After Commonwealth Credit Union grew its own loan volume by more than 14% using these tools in 2025, it decided to provide a blueprint for other small lenders to follow. Zest AI will build custom models to analyze credit risk for auto loans, personal loans, and credit cards more accurately than traditional scoring methods. The program focuses on keeping small lenders competitive by giving them access to the same machine learning tech used by larger firms. It also includes built-in features to help these institutions meet regulatory and fair lending requirements. By sharing operational expertise and technology management, the collective helps community lenders approve more members while managing risk. (Zest AI)

Happy Money Deepens Partnership with Edge Focus to Further Expand Access to Responsible Credit

Happy Money, a consumer finance company that provides personal loans for credit card debt consolidation, recently expanded its partnership with Edge Focus. This move gives the lender access to an additional capital channel to reach more borrowers. After making updates to its Hive lending platform last year, Happy Money increased its monthly loan originations more than 400% while maintaining steady asset performance. Edge Focus, a firm specializing in private credit, indicated that it plans to use the partnership to increase the availability of personal loans. The deal comes as institutional interest in this specific asset class grows. By using a variety of funding partners, Happy Money aims to scale its operations across different market conditions. The company has originated over $6.5 billion in loans to date. (PR Newswire)

Figure Confirms Data Breach Following Social Engineering Attack

Figure, a financial technology firm that uses blockchain to provide home equity lines of credit, recently confirmed a data breach after a social engineering attack targeted an employee. This trickery allowed hackers to snatch a limited number of files, though the company has not specified the total number of people affected. The hacking group ShinyHunters claimed responsibility for the incident on their dark web leak site, releasing 2.5 gigabytes of allegedly stolen data after the company reportedly refused to pay a ransom. This cache includes sensitive details like full names, home addresses, and dates of birth. Figure is currently offering free credit monitoring to those affected as they manage the fallout. The hackers claim this hit was part of a wider campaign targeting users of the single sign-on provider Okta, a spree that also included Harvard University and UPenn. It is a blunt reminder that even in a high-tech lending environment, human error can leave the door open. (TechCrunch)

Oregon House Committee Passes Bill Designed to Curb High-interest Lending

The Oregon House Committee on Commerce and Consumer Protection passed House Bill 4116 to tighten enforcement of the state’s 36% interest rate cap on short-term consumer loans. This bill targets out-of-state companies that provide quick cash to borrowers by closing a loophole that currently allows them to use the higher interest rate limits of their home states. While 98% of licensed lenders in the state already follow the cap, state data shows that five companies have issued 22,000 loans with rates above the limit since 2020. The committee split along party lines with a 6 to 4 vote because Republicans argued the change would limit credit options for people in financial emergencies. Representative Nathan Sosa, a sponsor of the bill, noted that Oregon established this 36% limit 20 years ago and simply wants to ensure everyone complies. This year’s version of the bill has more than 20 sponsors, which gives it more momentum than a similar attempt that failed in the Senate last year. Supporters are focusing on affordability as a major issue for their constituents as the bill moves forward to its next hurdle. (The Oregonian) (Oregon Live)

Adyen Launches ‘Personalize’ to Tailor Checkout Experiences in Real-Time

Adyen, a financial technology platform that processes payments for companies like Meta and Uber, just launched a tool called Personalize to modify the online checkout process in real-time. This new addition to their Uplift suite uses AI to change checkout pages based on how a shopper behaves, essentially predicting a preferred payment method before they start typing. Since about 37% of people abandon their digital carts if the process takes too long, Adyen is attempting to reduce that friction to keep more sales moving. The company reported that businesses using this dynamic approach saw payment conversions rise by an average of 1.19%, with some reaching a 6% increase. Beyond just speed, the system highlights payment methods that are cheaper for the merchant to process, which helps address the significant pressure that 72% of businesses feel from high transaction fees. It is a straightforward attempt to make the chore of paying for things less annoying so shoppers actually finish their purchases. For merchants struggling with a clunky user interface, this functions as a strategic update to help protect profit margins. (Adyen)

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to accelerate your affiliate marketing? Chat with New Market Growth

Sources: Adyen

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(Banking) Truist Launches Secure Open Banking Experience (Truist)

(Legal) Civil Rights Division Secures $68M Settlement In Predatory Land Sales And Lending Lawsuit (Department of Justice)

(Cards) Wells Fargo Expects Credit Card Loan Growth To Continue This Year (Reuters)

(Marketing) Making Marketing More Human: How Chime Is Building An AI-Powered Brand With Empathy At The Center (Chime)

(Lending) Figure CEO Michael Tannenbaum On Partnering With Bed Bath & Beyond (HousingWire)

(Fintech) Pliant’s American Dream Takes Flight With Visa (FinTech Futures)

(Payments) Amazon: Payment Options To Include Pay-By-Bank And Prime (Fintech Magazine)

(Partnerships) NBA, American Express Announce Multiyear Partnership Extension (NBA)

(Regulation) Illinois Judge Rules In Favor Of Swipe-Fee Ban On Sales Tax And Tips (American Banker)

(E-commerce) Google Launches Agentic Commerce With Etsy And Wayfair (PYMNTS)

(Payments) Cash App Launches Payment Links: An Even Smpler Way To Request Money (Cash App)

(Savings) Experian Makes Saving Even Smarter With New High Yield Digital Savings Account (Experian)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/cash-app-to-sell-its-credit-score

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.