Affirm Submits FDIC Application Through ILC

Affirm’s quest for a bank charter, OnePay’s post-purchase swipe.

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

Affirm is officially making a play to become its own bank by submitting applications to establish Affirm Bank through a Nevada-chartered Industrial Loan Company (ILC). This strategic shift aims to strengthen and diversify their platform, allowing them to scale operations and offer FDIC-insured products directly to consumers.

OnePay is leveling up its rewards game through a new partnership with the Rakuten Card Linked Offer Network to make saving frictionless. We are also closely tracking a massive wave of earnings reports from heavy hitters like Ally, BofA, Capital One, and JPMorgan, which show record-breaking revenues despite a tightening credit landscape. Other stories we’re watching this week include Credit Karma’s ChatGPT integration, PayPal’s AI-driven acquisition of Cymbio, and the high-stakes political game of big banks weighing 10% interest rate cards.

Lots to break down. Let’s get toasting!

— Carlos Caro, Founder at New Market Growth

— Nick Madrid, Co-Founder of The Free Toaster and Uncovered Media

PS: To support us, please share our Newsletter in your internal Slack channels!

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers’ financial accounts.

Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand’s experience.

With many happy customers, including:

Affirm Submits FDIC Application to Establish Industrial Loan Company

Affirm is officially making a move to become its own bank, submitting applications to federal and Nevada regulators to establish Affirm Bank. This proposed industrial loan company would allow the honest financial products provider, which builds payment networks based on trust and transparency, to scale its operations and offer FDIC-insured products directly. Founder Max Levchin thinks this shift will strengthen and diversify the platform, especially since the company already boasts a track record of extending nearly $130 billion in credit without those pesky late fees. By ditching traditional revolving credit cards for Affirm, the company claims U.S. households could have saved a substantial $18 billion in 2024 alone. To lead this new venture, they’ve tapped John Marion, a veteran with over 25 years of experience from heavy hitters like JPMorgan Chase. This move represents a strategic step toward long-term growth by internalizing operations that previously relied on partner banks. If regulators approve the applications, Affirm plans to leverage the new structure to roll out a broader suite of financial products and services.

Toaster’s Take

By seeking a Nevada-chartered industrial loan company (ILC) license, Affirm executes a strategic playbook recently used by Block to transition from a fintech intermediary into a fully integrated, FDIC-insured financial powerhouse. This specific move already enabled Block to provide over $200 billion in credit and move Cash App Borrow originations entirely in-house. (Affirm)

The Free Toaster Podcast takes the biggest fintech, credit, and payments stories of the week and breaks down what they mean for growth, distribution, and product strategy. If you read the newsletter, this is the conversation behind it.

Listen on Apple Podcasts, Spotify, Substack, or wherever you get your podcasts.

Be sure to check out out our latest pod!

OnePay Announces New Rewards Partnership with Rakuten Card Linked Offer Network

OnePay, the all-in-one financial services platform that offers everything from high-yield savings to crypto, just leveled up its rewards game through a new partnership with the Rakuten Card Linked Offer Network. This strategic integration means you’ll soon find Rakuten card-linked deals directly inside the OnePay app, letting you stack savings without the usual headache of hunting for promo codes. You simply link your card, activate as many offers as you want, and watch the value effortlessly roll in while you shop at your favorite merchants. The company aims to drive deeper engagement by embedding these perks into the way you already spend, proving that the best financial tools are the ones that actually make saving fun. Jen Jia, General Manager of OnePay Wallet, thinks rewards work best when they don’t force you to change your behavior, and we couldn’t agree more. Expect these enhanced earning opportunities to hit your app in the coming months as OnePay continues its quest to make your money work harder than you do.

Toaster’s Take

This partnership shows fintech is moving toward a future where your bank acts more like a personal shopper than a vault. By removing the need for manual couponing or scanning QR codes, OnePay is betting that instant recognition and real-time value are the keys to keeping you in their app. (PR Newswire)

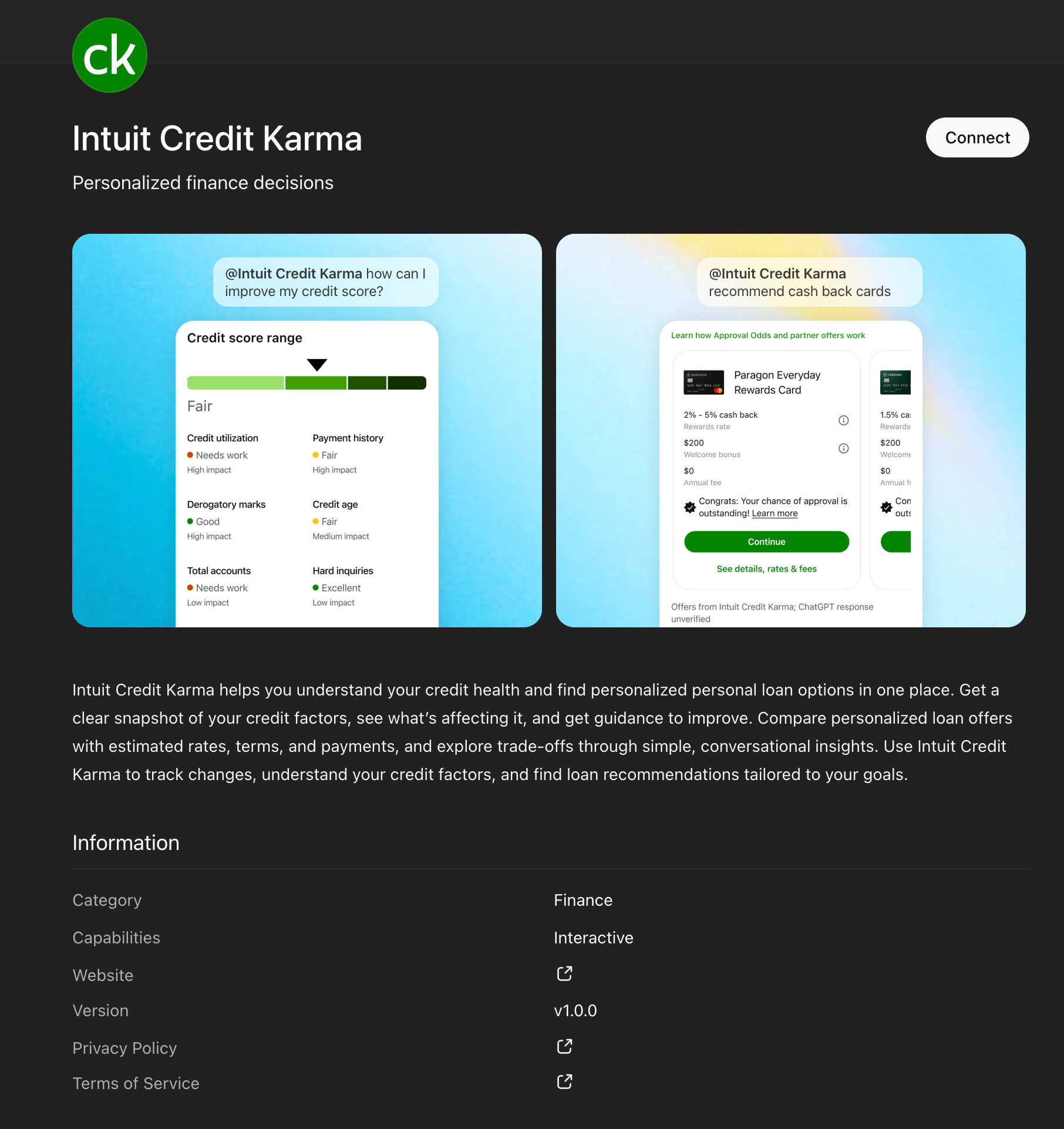

Credit Karma’s ChatGPT App Helps Consumers Improve Their Score and Shop For Products

In November of last year, Intuit and OpenAI announced they would partner on a a multi-year, strategic partnership with OpenAI to create the future of Financial Intelligence by bringing together leading platforms to drive the next era of growth with Intuit-powered apps in ChatGPT.

Now, we’re seeing tangible signs of what that looks like for the consumer.

After clicking the Connect button on the top right of the screenshot above, the user is prompted to authenticate into their Credit Karma account (presumably to receive personalized credit score advice and product recommendations).

It will be interesting to see if customers gravitate to this format.

Toaster’s Take

We’re not surprised to see Karma make moves following the November Press Release covering the Intuit Partnership with OpenAI. It’s exciting to see Karma continue to push on the frontiers of technology even as the clear leader in the consumer lending marketplace category.

OnePay Introduces Swipe to Finance, Powered by Klarna

OnePay, an all-in-one financial services platform providing tools like banking and high-yield savings to millions of Americans, just teamed up with global digital bank Klarna to save your bank account from those accidental splurges. The duo announced Swipe to Finance, a new feature that lets users convert recent debit purchases into fixed-term payment plans even after they leave the store. We have all experienced that moment of checkout regret, and this post-purchase flexibility aims to fix the timing of your money without the stress. While Klarna powers the backend of this smarter payment option, users manage everything directly within the OnePay app for a seamless experience. This broad roadmap follows their previous installment-loan partnership, signaling a significant push into flexible retail credit. Whether you overspent on a whim or a bill hit at the wrong time, these transparent payment options make managing your financial life feel a little less like a chore and a lot more like a win. It is a major step for both companies as they expand their reach to frontline workers and gig platforms alike. (PR Newswire)

Enjoying this week’s issue?

If you’ve been enjoying The Free Toaster, help us spread the word. Forward it to someone who lives and breathes consumer lending, marketing, or fintech like you do.

Your shares help us reach more builders in consumer lending, and help us make the Newsletter & Podcast better every day.

Hysteria vs. Reality: The Truth Behind the Auto Finance “Canary in the Coal Mine”

Car Dealership Guy Newsletter provides a deep dive into the auto retail world by breaking down top trends and insights for dealers in under five minutes. While scary headlines suggest an auto lending collapse is imminent, the actual data shows the industry is simply facing a long affordability squeeze rather than a total financial meltdown. Even though subprime delinquencies look undeniably ugly at record levels, prime loans still outnumber them 4:1 and perform in a boring and stable way. This indicates that unless the labor market rolls over, these delinquencies are just symptoms of broader economic inequality instead of a “canary in the coal mine” for a systemic crisis.

Buyers are clearly feeling the pinch as they stretch their budgets, with over 20% of new car purchases now requiring undeniably long 84-month loans just to make payments work. Interestingly, credit availability actually hit its best level since late 2022, signaling that lenders are refining their models for a competitive market rather than a desperate one. You also shouldn’t count on the new federal tax deduction to save the day since its impact on total sales will likely stay marginal at best. While dealers will certainly market the hell out of the deduction, it will likely serve as a patriotic talking point rather than a real closing tool for deals. (Experian) (Cox Automotive) (TaxAct)

PayPal Seeks an AI Edge by Buying E-Commerce Fintech Cymbio

PayPal is making a power move to own the future of shopping by snatching up Cymbio, a Tel Aviv-based fintech that specializes in e-commerce and artificial intelligence tools. By acquiring this 11-year-old firm, the payments giant, which processes billions in transactions as a global digital wallet, is bulking up its ability to connect merchants directly to AI bots. Cymbio’s team will now dive into Store Sync, a tool that ensures a merchant’s product catalog is discoverable when you’re chatting with an AI like ChatGPT or Perplexity. It’s a big win because it gives PayPal control over the product-detail page, which is basically the holy grail for making sure an AI agent actually buys the right pair of shoes for you. While everyone from Visa to Mastercard is racing to figure out agentic commerce, PayPal just took the single largest independent source of product data off the table for its rivals. It’s clear that PayPal isn’t just waiting for the future to happen; they are building the plumbing so that when your AI assistant goes shopping, it’s using their tech to close the deal. This acquisition shows that if you aren’t making your products readable for robots, you’re basically invisible in the next era of the internet. (American Banker)

PayPal Turns to AI to Boost Branded Checkout

PayPal is betting big on agentic commerce to revive its branded checkout business, which currently accounts for about 29% of its total payment volume. The payment fintech recently teamed up with Microsoft to integrate its digital wallet into Copilot, allowing shoppers to find products and pay without ever leaving the AI app. It is a savvy move for the company, which provides digital payment processing and peer-to-peer transfers, especially since its stock has taken a flagging 40% hit over the last year. While the top 10% of earners keep the economy humming, PayPal is banking on the 44% of Americans who are ready to let an AI assistant do their browsing. This shift aims to protect and empower its market share against rivals like Visa, Mastercard, and Stripe who are also rushing into the AI space. Analysts are watching closely, as intensifying competitive pressure means PayPal needs this partnership to deliver more than just a cool demo. If they can make spending money as effortless as chatting with a bot, they might just find that sustainable fun in their bottom line again. (American Banker)

ChatGPT Checkouts to Take 4% Cut of Shopify Merchant Sales

Shopify, the commerce platform that helps millions of businesses sell products online and in person, is letting AI chatbots handle the shopping cart starting this month. While shoppers can soon buy gear directly through Google Gemini and Microsoft Copilot for free, OpenAI plans to take a 4% cut of sales made through the ChatGPT checkout feature. Shopify merchants must opt in if they want to pay that extra fee, though their products will appear in AI responses by default across all platforms. This rollout follows a data-sharing setup that allows these AI apps to pull product details directly from the digital storefronts. Most sellers will see their inventory go live in these AI apps beginning January 26, marking a big shift in how we might discover our next favorite pair of shoes. If a merchant finds this new world of bot-driven commerce a bit too unusual or expensive, they can toggle individual platforms off or block web crawlers to keep their listings private. It’s a bold bet that consumers actually want to shop while they chat, turning OpenAI and its peers into the newest digital storefronts on the block. (The Information)

AFC Slams Profit-Driven State Mandate Proposals for EWA, Warning of Serious Privacy Risks

The American Fintech Council (AFC), a premier industry association representing responsible fintechs and innovative banks, is sounding the alarm on some harmful state database mandates. They just released a white paper slamming proposals that would force Earned Wage Access (EWA) providers to hand over sensitive info to outdated systems meant for payday loans. AFC argues that these profit-driven mandates by a single vendor, Catalis, create serious privacy risks and do absolutely nothing to help workers. It feels like a classic case of trying to fit a square peg in a round hole, especially since EWA isn’t even a loan, it’s just people getting their own money early. The council points out that these overwhelming deficiencies in current databases lead to higher consumer costs and technical glitches rather than real protection. We should probably ask if regulators are actually having fun yet, or if they’re just stuck in a conflict of interest loop that wastes taxpayer dollars. Instead of helping, these rules might just jeopardize consumer privacy and stifle the very tools that give underserved folks a financial leg up. (American Fintech Council)

Big Banks Play Ball: BofA and Citi Weigh 10% Cards to Score Points with Trump

Bank of America, the retail banking giant that provides everything from checking accounts to investment management, is weighing the launch of new credit cards with a 10% interest rate to play ball with President Trump’s recent demands. Citigroup, another massive global lender known for its diverse financial services, is also reportedly considering these low-rate cards as a potential workaround to a broader interest rate cap. Trump recently asked Congress to green-light a one-year cap, sparking some serious backlash from industry groups who fear it will curb economic growth. While banking execs warn that such a move might force them to restrict access to credit, some experts think these highly profitable cards actually have plenty of room for lower rates. To keep things moving, lenders might just roll out no-frills cards that hit the 10% mark but ditch the usual fancy perks and benefits. It’s a bit of a high-stakes game of chicken, especially since credit cards serve as a strong profit engine that usually offsets the higher risk of unsecured lending. Whether this becomes a reality or just a political compromise remains the big question for your wallet. (Reuters)

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to accelerate your affiliate marketing? Chat with New Market Growth

Growth Tracker: Earnings and New Investments

Record 15.5 million consumer auto applications powered Ally Financial to a $7.9B full-year revenue performance , anchored by a $43.7B origination volume. Fourth-quarter Adjusted EPS reached $1.09 on $386M in pre-tax income , as a 3.48% NIM—up 18 bps YoY—reflected disciplined deposit pricing and balance sheet optimization. The firm's strategy remains its massive retail deposit base, which grew to $143.5B across 3.5M customers , maintaining a 92% FDIC-insured profile. Credit quality stayed resilient with retail auto net charge-offs falling to 2.14% , down 20 bps YoY , while the Corporate Finance wing maintained a stellar 29% ROE. CEO Michael Rhodes emphasized that strategic pivots, including the sale of the Credit Card business and a $2B share repurchase authorization , have fortified the balance sheet for a more neutral rate risk position heading into 2026. (Ally Financial)

Bank of America capped a banner year with 4Q25 net income surging 12% to $7.6B, fueling a YoY EPS spike of 18% to $0.98. Revenue climbed 7% to $28.4B, powered by a 10% jump in net interest income to $15.8B as fixed-rate assets repriced amid resilient loan and deposit growth. The efficiency ratio improved 194 bps to 61% despite a 4% rise in expenses for technology and people. Asset quality remained a primary differentiator, with provisions for credit losses falling to $1.3B while average deposits hit a record $2.01T. Within the segments, Global Wealth saw a 10% revenue lift on surging asset management fees, and Equities trading revenue soared 23%. CEO Brian Moynihan remains bullish on a resilient U.S. economy, citing positive operating leverage as the key driver for 2026 momentum. (Bank of America)

Capital One capped off 2025 with a significant strategic pivot, announcing a $5.15 billion acquisition of Brex Inc. while reporting fourth quarter net income of $2.1 billion or $3.26 per share. While Q4 revenue ticked up 1% to $15.6 billion, adjusted EPS reached $3.86 after accounting for Discover integration costs and a home loan portfolio sale. The full year story showed massive scale with revenue surging 37% to $53.4 billion, though profitability was tempered by an $8.9 billion spike in credit loss provisions. CEO Richard Fairbank cited solid top line growth and strong and stable credit performance as the foundation for the firm’s long-term returns. Despite a 10 bps dip in net interest margin to 8.26%, the company maintained a robust 14.3% CET1 capital ratio and grew its Domestic Card loan book by 3% to $262.4 billion. (Capital One)

Record $85.2B in full-year revenue fueled Citigroup's significant 2025 progress as Jane Fraser drove positive operating leverage across all five core businesses. Fourth-quarter reported revenue rose 2% to $19.9B, though results were dampened by a $1.1B after-tax loss related to the planned sale of AO Citibank in Russia. Excluding this notable item, quarterly revenue climbed 8% while EPS reached $1.81, outperforming the reported $1.19. The Services segment acted as the quarter's profit engine, surging 15% to $5.9B behind deeper client mandates and a 24% increase in assets under custody. Despite a 6% rise in expenses to $13.8B due to technology investments, the firm returned $17.6B to shareholders through buybacks and dividends throughout 2025. Fraser enters 2026 with visible momentum, targeting a 10-11% ROTCE as the bank pivots toward improved long-term returns. (Citigroup)

Experian clocked a 10% constant currency revenue jump for Q3 FY26, fueled by a 12% increase at actual exchange rates and a resilient 8% organic expansion that met internal targets. While North America maintained its role as the primary engine with 10% organic growth, Latin America stole the spotlight as Consumer Services revenue there surged 23% after reaching a landmark 100 million free members in Brazil. CEO Brian Cassin highlighted the firm's ability to leverage proprietary data and AI opportunities like the Patient Access Curator to offset softer economic activity in the UK and Ireland, where B2B organic revenue remained flat. Strategic acquisitions including ClearSale and KYC360 further bolstered the portfolio, contributing to a 15% total growth rate in Latin America. With momentum holding steady across its Financial Services and Verticals segments, management reiterated its full-year outlook as the company heads toward its May year-end results. (Experian)

JPMorgan Chase capped off 2025 with a powerhouse fourth quarter, delivering $46.8B in managed revenue—a 7% YoY increase—even as a massive $2.2B credit reserve build for the Apple Card portfolio transition pulled reported net income down 7% to $13.0B. Excluding this significant item, net income reached $14.7B or $5.23 EPS. Performance was bolstered by a 17% surge in Markets revenue, particularly a 40% leap in Equity Markets, while Asset & Wealth Management hit record revenue of $6.5B on the back of $553B in annual net inflows. CEO Jamie Dimon highlighted the resilience of the U.S. economy and the firm's selective deployment of excess capital into high-growth opportunities like the Apple Card, though he cautioned that markets may be underestimating geopolitical risks and sticky inflation. The firm maintained a fortress balance sheet with a 14.5% CET1 ratio and a 20% full-year ROTCE. (JPMorgan Chase)

Synchrony Financial defied a tightening credit landscape, reporting a 4% surge in net interest income to $4.8B as strategic pricing and policy changes boosted loan yields. Despite a 3% dip in net earnings to $751M, diluted EPS climbed 7% YoY to $2.04, aided by $952M in aggressive share repurchases. The profit engine remained resilient with a net interest margin expansion of 82 bps to 15.83%, even as a $51M after-tax restructuring charge for early employee retirements pressured efficiency. Credit quality served as the quarter’s differentiator; net charge-offs plunged 108 bps to 5.37%, returning the portfolio to target ranges. CEO Brian Doubles signaled momentum for 2026, highlighting over 20 million new accounts and $182B in annual purchase volume as evidence of the company's deepening role at the center of American commerce. (Synchrony Financial)

Propelled by the removal of its long-standing asset cap, Wells Fargo delivered a robust fourth quarter with net income rising to $5.4B, or $1.62 per diluted share. Total revenue climbed 4% YoY to $21.3B, fueled by a 16% surge in Wealth and Investment Management interest income and a 14% jump in investment banking fees. While net interest income saw a slight 4% lift to $12.3B, the bank successfully managed expenses, which decreased 1% to $13.7B despite a $612M severance charge. Credit quality remained a focal point as net charge-offs declined 13% YoY, though the consumer charge-off rate ticked up to 0.75%. CEO Charlie Scharf emphasized a new medium-term ROTCE target of 17-18%, noting the company returned $23B to shareholders in 2025 through dividends and aggressive stock repurchases. (Wells Fargo)

Looking for hiring signals too?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Other News We’re Reading

(Lending) The Atlantic Federal Credit Union Becomes First Credit Union to Go Live with MANTL Loan Origination (PR Newswire)

(Lending) Rize Credit Union Partners with Upstart to Expand Access to Personal Loans in California (Upstart)

(Banking) Grow Financial Credit Union Chooses MANTL to Elevate the Member Experience (PR Newswire)

(Cards) Trump credit card plan would be a ‘disaster’, JP Morgan boss warns (BBC)

(M&A) Heartland Credit Union and Novation Credit Union Announce Intent to Merge (Heartland CU)

(Lending) Wonder Partners with FormPiper and LendingClub to Bring Enterprise-Grade Financing to Independent Furniture Retailers (GlobeNewswire)

(Fintech) Treasury Prime Adds Two Institutions to Industry-Leading Bank Network, Accelerating Embedded Finance Growth (Treasury Prime)

(Fintech) Credit Key lands $90m in growth capital and partnership with Barings (FinTech Futures)

(Cards) MEXC Partners with ether.fi to Expand Ecosystem Utility with a Co-Branded Card (MEXC)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

https://www.thefreetoaster.com/p/affirm-submits-fdic-application-through

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.