Source: https://www.svb.com/trends-insights/reports/fintech-industry-report/

TL;DR - We summarize SVB's October 2025 fintech report. The Fed is expected to cut rates by 100-125 basis points over the next year, potentially boosting consumer demand for loans. However, student loan delinquencies have surged above pre-COVID levels, with borrowers under 49 holding more student debt ($1.2T) than mortgages ($1.0T), signaling caution for lenders. The regulatory environment has become more favorable for fintechs with a trimmed-down CFPB, while companies have shifted focus from growth to profitability. Meanwhile, VC funding requirements have increased, with Series A companies now needing $4MM in revenue versus $1MM in 2020-2021.

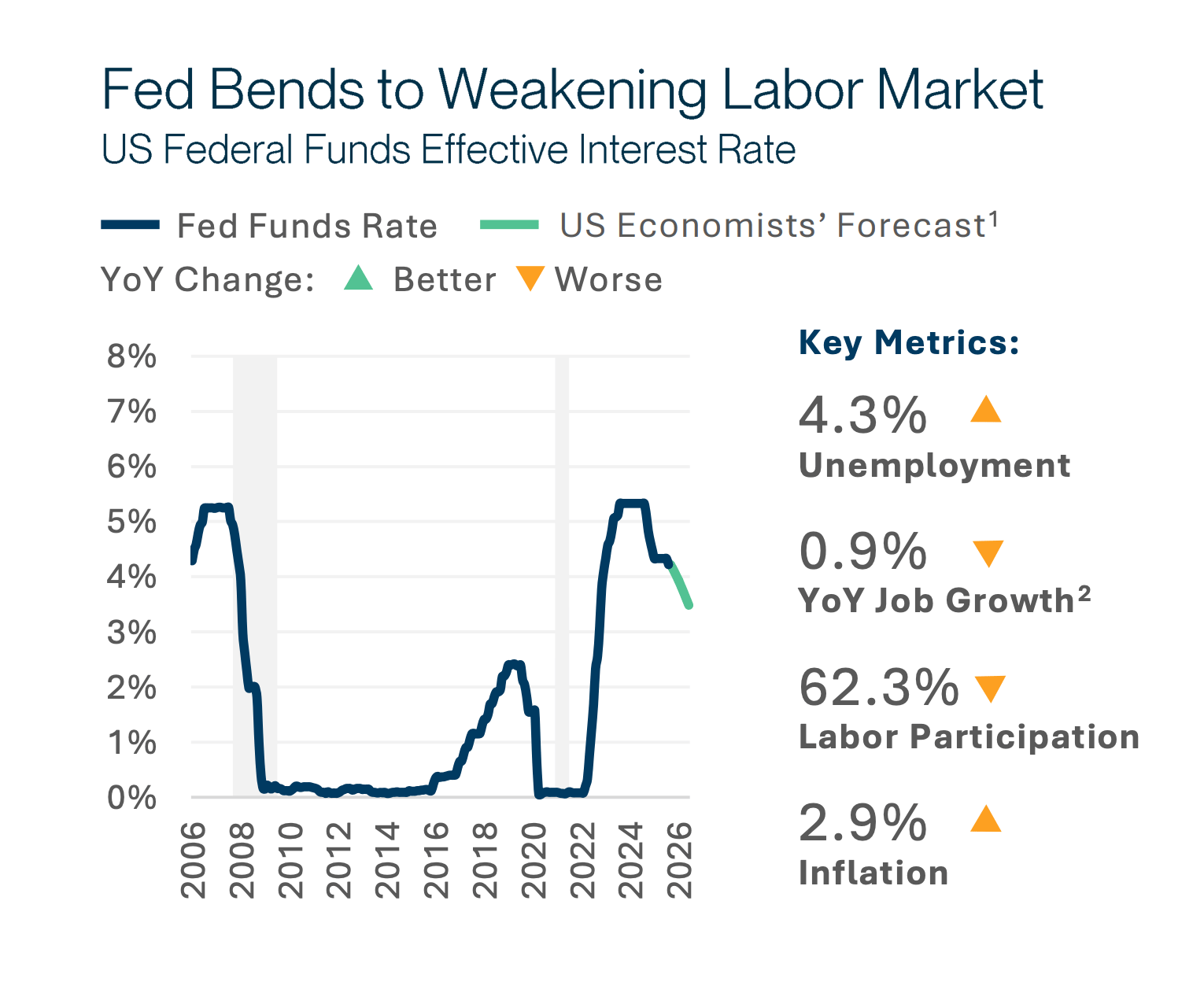

1. The market expects the Fed Funds Rate to drop, but by how much?

SVB’s The Future Of Fintech Report, Oct 2025

This charts tell us what been circulating in the news for months - the Fed is going to cut rates.

But, by how much?

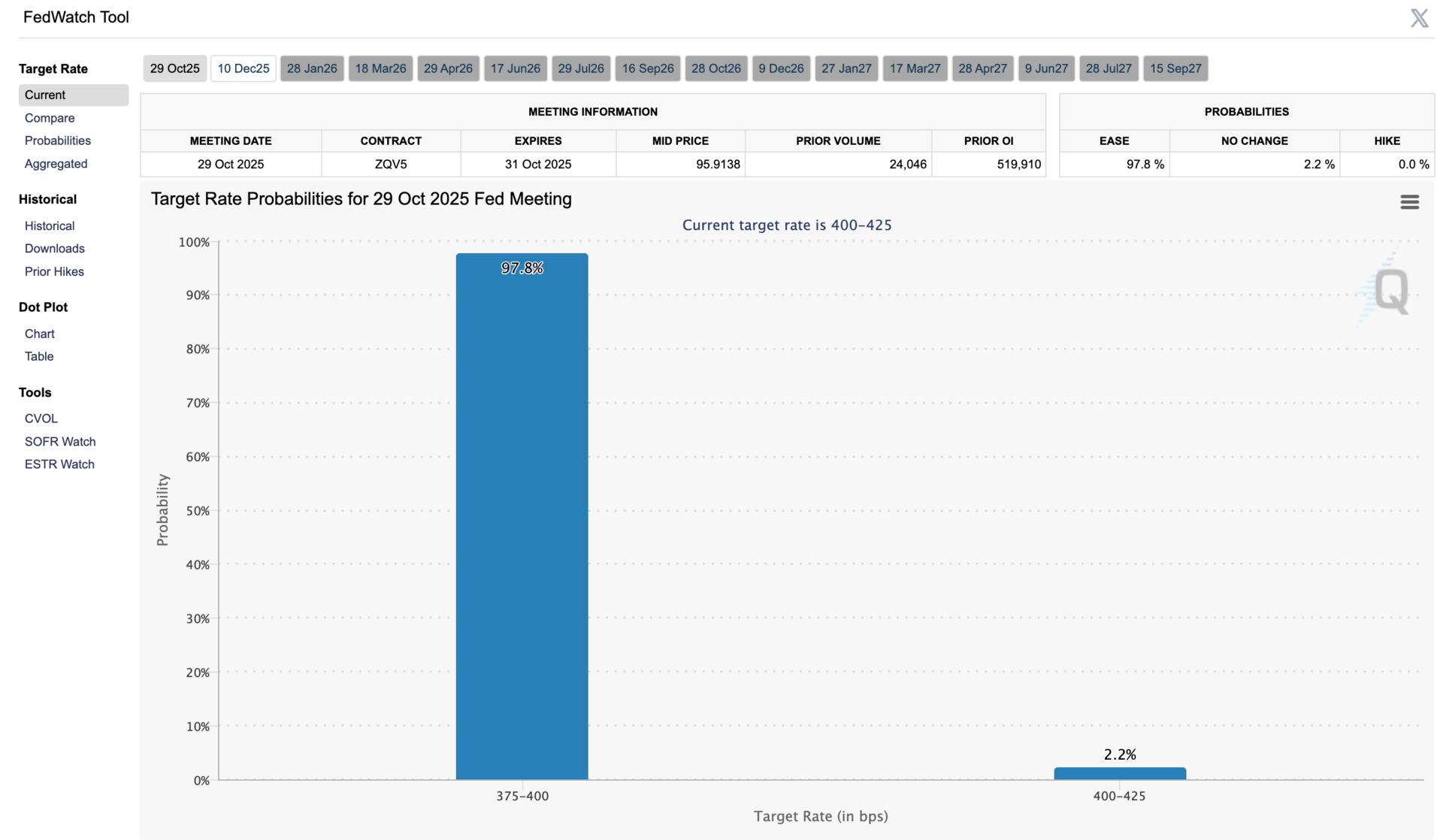

To measure this, we looked at CME FedWatch.

There, we learned two things.

CME FedWatch

First, it’s a near certainly (97.8%) that the Fed will cut rates by 25 bps at its next meeting on October 29th, 2025 (that’s tomorrow!).

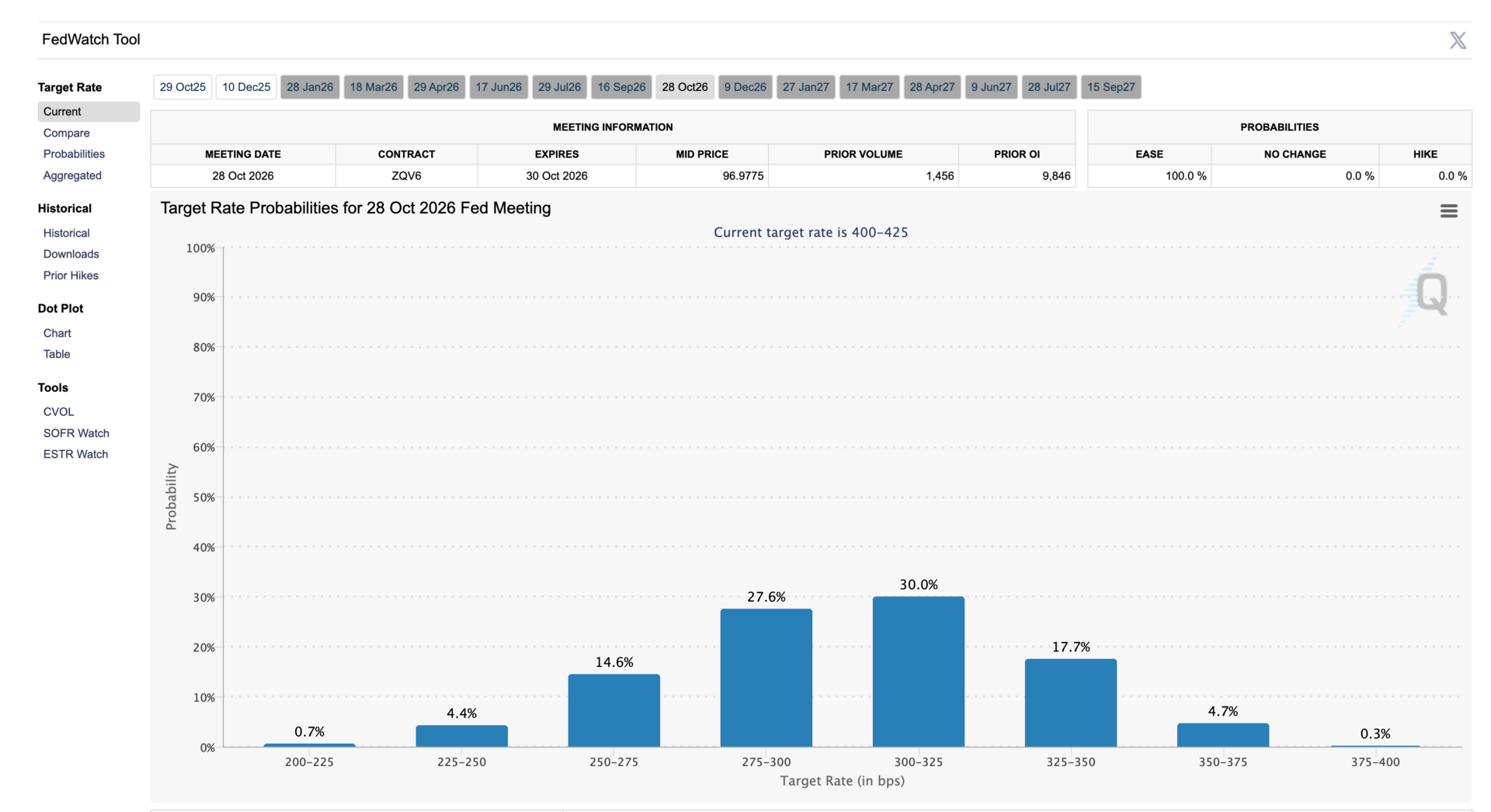

CME FedWatch

Second, it seems like rates will decrease by 100-125 bps one year from today, with a 57.6% probability.

Additionally, CME FedWatch shows a 19.7% chance of a greater than 150 bps reduction, and a 22.7% chance of a reduction of 75 bps or less.

This could drive consumer demand to rate-sensitive lending businesses like personal loans, auto refinances, and mortgages, assuming macro credit health (delinquencies and losses) don’t change.

So what does SVB’s report suggest about that?

2. Delinquency rates look healthy (with one big exception)

SVB’s The Future Of Fintech Report, Oct 2025

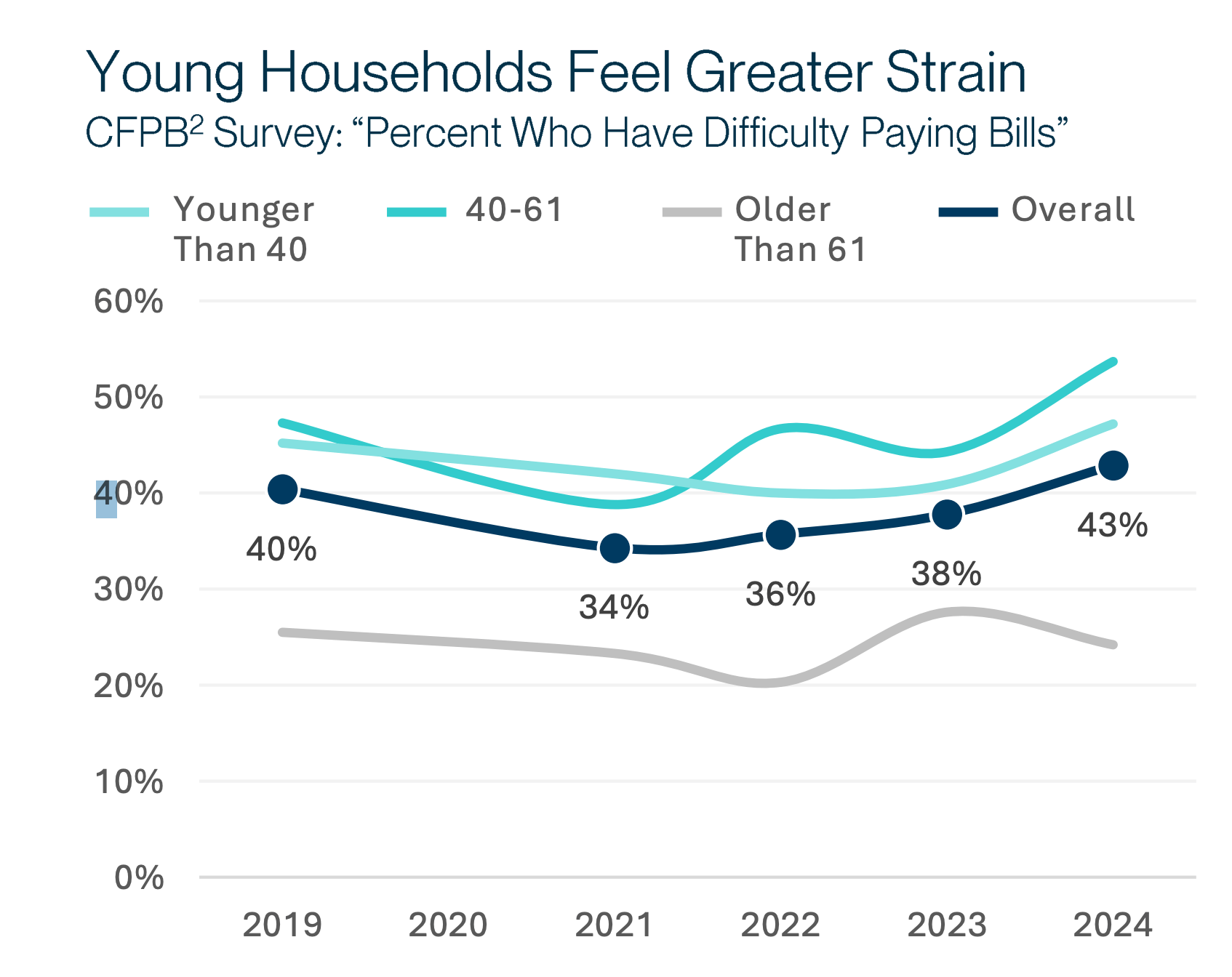

The CFPB’s survey, though a little dated, is showing increasing financial strain among households less than 61 years old.

SVB’s The Future Of Fintech Report, Oct 2025

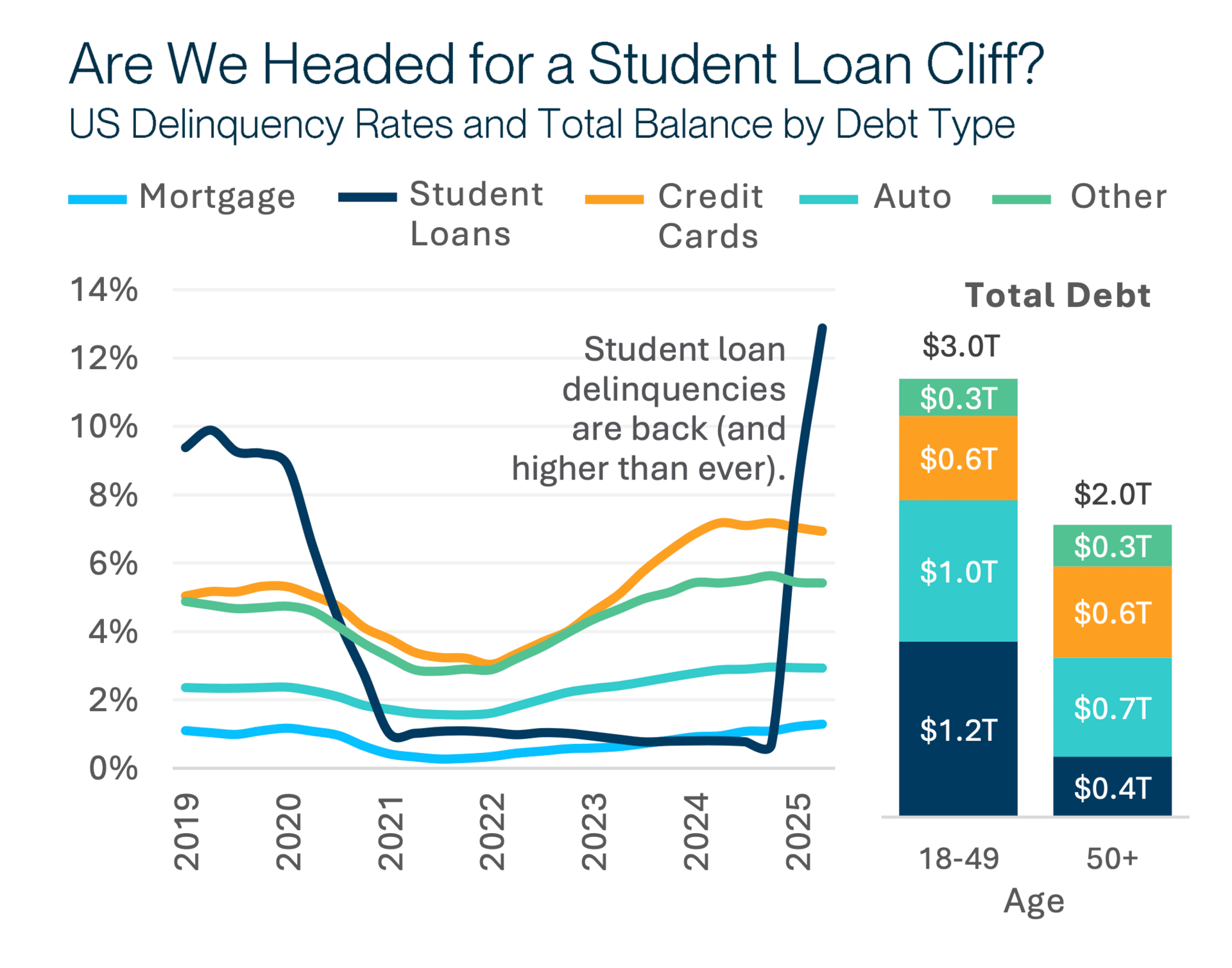

With that color from the CFPB survey, we look to the delinquency rate. There we see DQs more or less steady in the credit card, auto, and “other” categories, with mortgages showing an increase from 2024 to 2025.

What jumps off the page is the student loan data.

We’re now above pre-COVID era delinquency rates in student loans, with people under 49 (according to this chart) holding more student loan debt ($1.2T) than mortgage debt ($1.0T)! 1

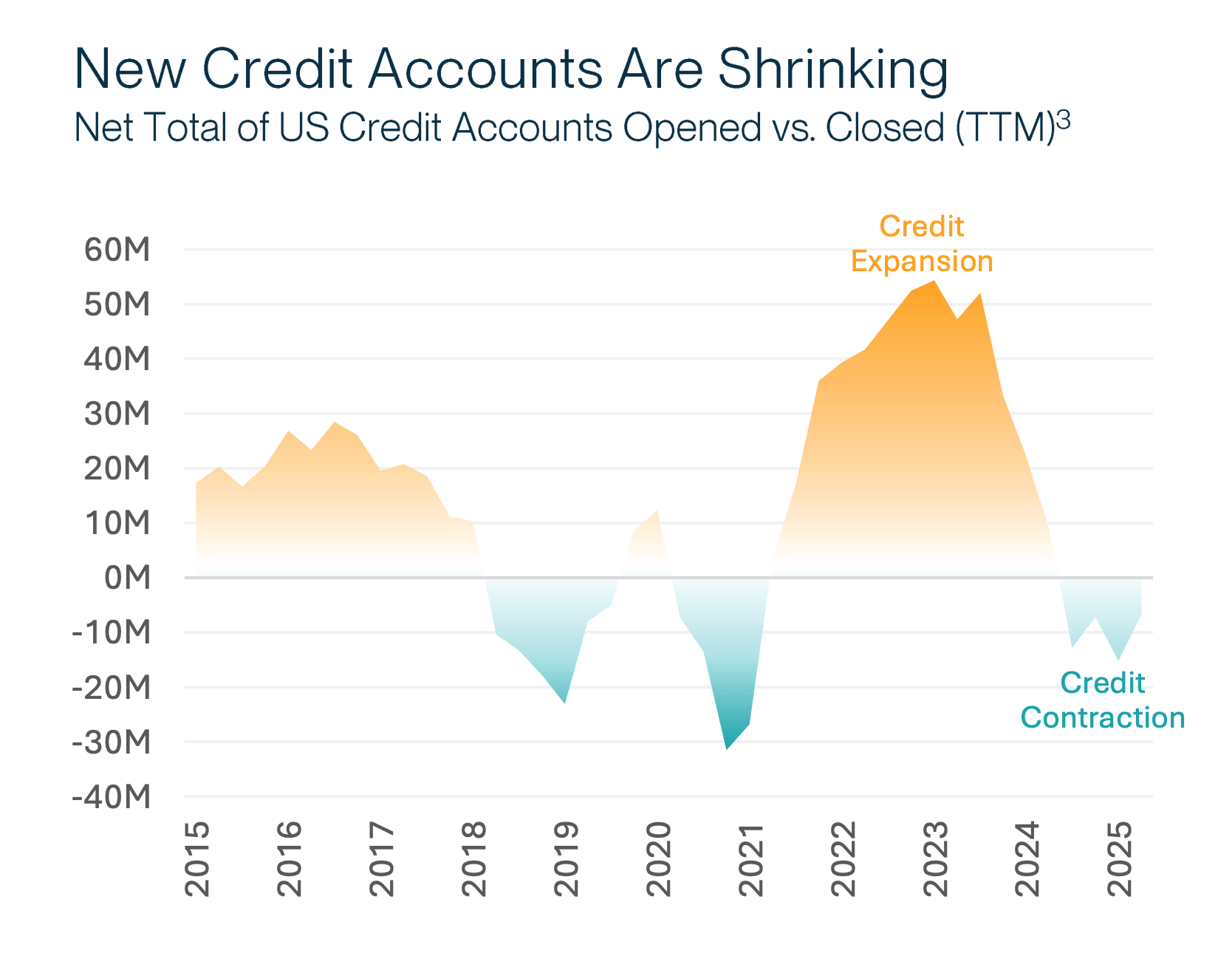

This implies lenders should be cautious, and the chart below supports that:

SVB’s The Future Of Fintech Report, Oct 2025

Lenders I speak with comment that the credit expansion that started in 2021 led to higher than expected losses in some cases.

Today, we’re seeing a more prudent approach reflected, which likely bakes in macro uncertainties (what will the Fed do?, will the consumer stay strong?) with a cool-off that you’d expect following a period of major expansion.

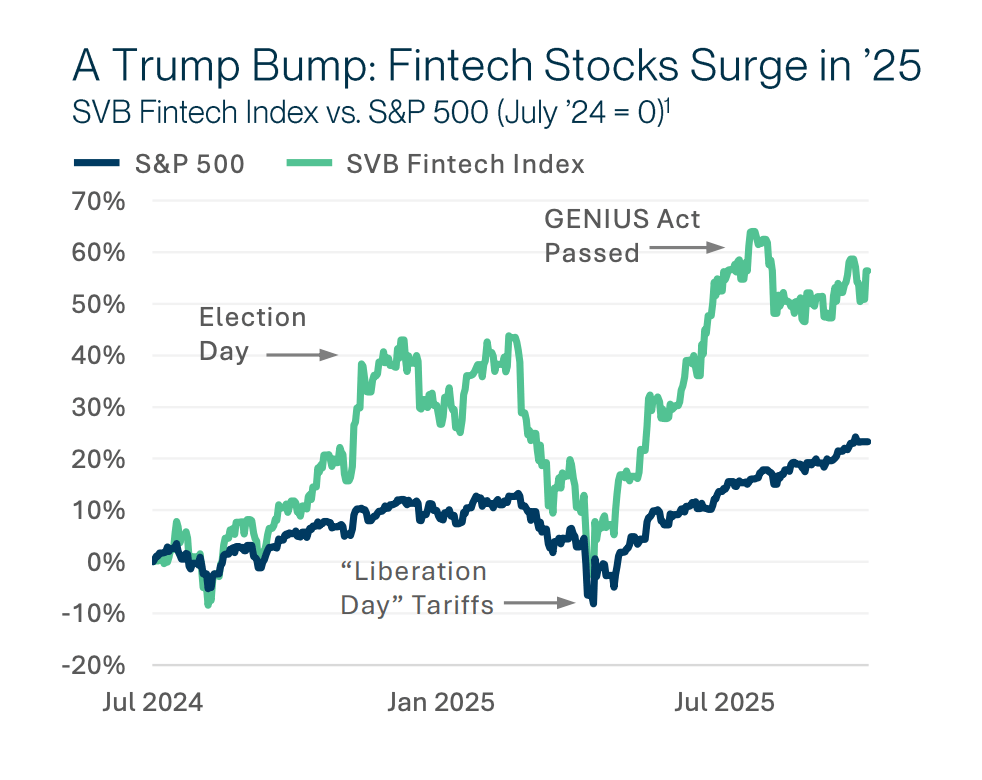

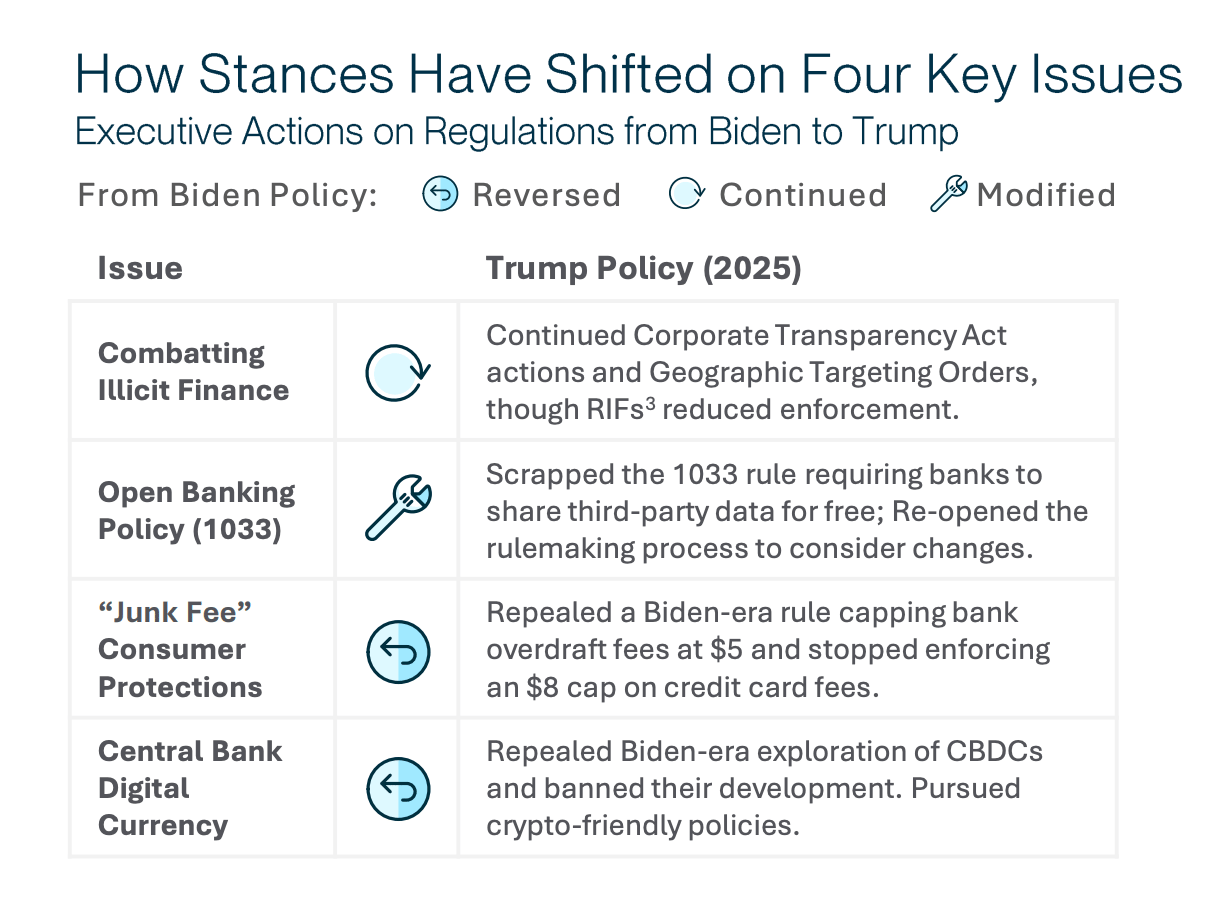

3. A more favorable regulatory environment for Fintechs

Setting aside your views about the current administration, investors have voted clearly in favor of the current environment for Fintechs:

SVB’s The Future Of Fintech Report, Oct 2025

For lenders specifically, a reduced-staff CFPB and a repeal of bank rate fee caps presents a more favorable operating environment.

SVB’s The Future Of Fintech Report, Oct 2025

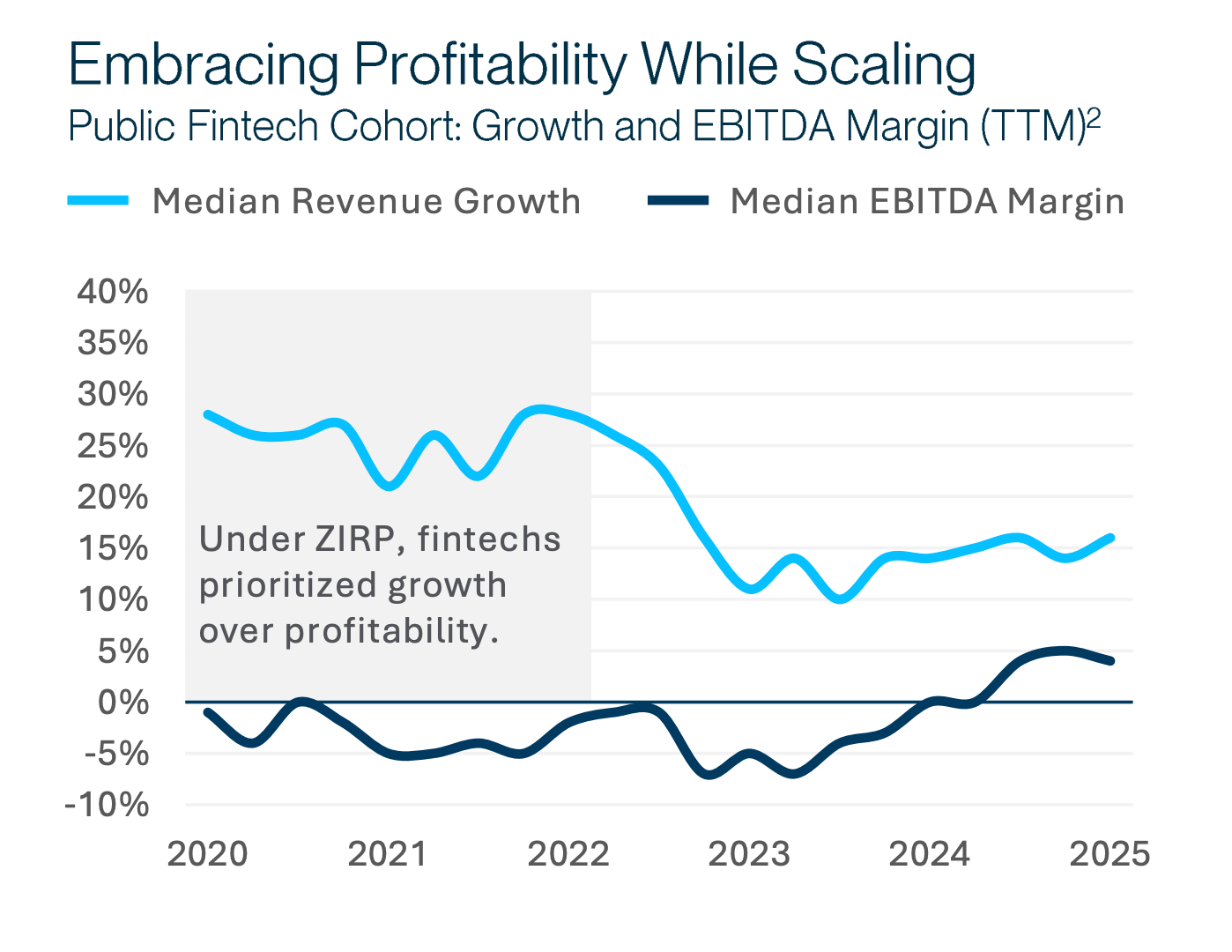

4. Fintechs are prioritizing profitability over top-line revenue growth

SVB’s The Future Of Fintech Report, Oct 2025

I’ve heard it in board rooms for years. Profitability over growth. Profitability over growth.

SVB’s public fintech cohort data shows revenue growth notably down from the ZIRP era, and profitability notably up.

Looks like CEOs have been taking those boardroom conversations to heart.

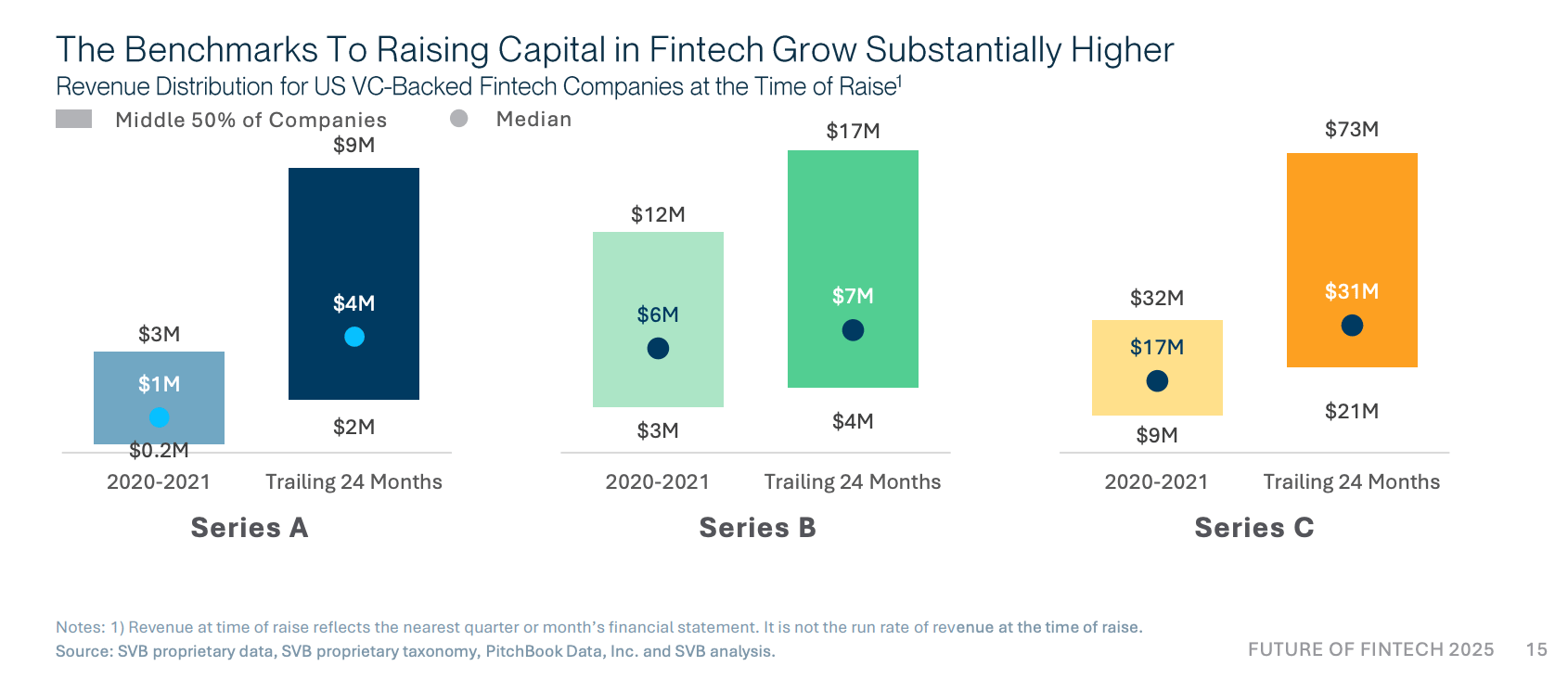

5. The bar to raise VC money has increased

This chart says it all:

SVB’s The Future Of Fintech Report, Oct 2025

The median fintech raising a Series A in 2020-2021 had $1MM in the nearest monthly or quarterly financial statement. In the last 24 months, that number has increased to $4MM.

That chart above shows a similar pattern of increasing revenue bars for Series B and Series C companies.

With advances in technology and profitability/sustainability valued at a premium, investors can be pickier about which companies they fund.

Recap: Takeaways for Lenders

1. The market expects Fed rates to decline by 100-125 bps in the next 12 months, potentially boosting consumer demand for loans.

2. High delinquency rates (12%+) in the student category is a reason for lenders to be cautious with new originations.

3. The current government administration is creating a favorable regulatory environment for lenders.

4. Fintechs are trading lower growth for higher margins to meet investor demands.

5. The revenue bar for raising VC has increased, and may continue to increase as founding teams learn how to do more with less headcount (with AI and improvements in the fintech technology stack).

Footnotes:

Note that the SVB reports commentary said “Americans younger than 40 owe $1.2T in student debt, more than any other debt category.” Since this commentary is inconsistent with the chart we included that shows student debt outstanding, it is unclear which data point is accurate. In this article, we assumed was shown in the chart was correct.

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need to accelerate your affiliate marketing? Chat with New Market Growth

Need to win on other growth channels? Chat with FIAT Growth

About Us

Welcome to The Free Toaster! The newsletter for marketing pros at fintechs, banks, and lenders.

Inspired by the free toasters banks used to give to each new customer, we’re here to help you acquire more customers at scale. We deliver fresh news, data, and insights, minus the breadcrumbs.

Want to follow the authors on social media?

Carlos Caro is the founder of New Market Growth, an agency that helps lenders build affiliate programs.

Nick Madrid is the co-founder of Ghostmode, a media company that builds Newsletters, Podcasts, and communities in high-value B2B niches.