UltraFICO Takes Shape with FICO x Plaid, CFPB Targets ECOA Rules, Made Card Bets on Homeowner Rewards

Made Card launches homeowner rewards, Wealthfront tests mortgages, Klarna rolls out a stablecoin, ChatGPT adds shopping research, Worldpay builds agentic tools, Cash App pilots a real time score, and more.

Hey Toaster Readers,

This week is sponsored by our friends at Spinwheel.

FICO and Plaid are pairing traditional scoring with live cash flow data through the new UltraFICO Score. The CFPB proposes limiting fair lending liability by removing “disparate impact” from ECOA, a shift that would require proof of intentional discrimination and change how lenders document and defend their credit decisions. And Made Card raised new funding to build a rewards product around real homeowner spending, including mortgage payments.

The rest of the week brought plenty of signals. Wealthfront is testing mortgages. Klarna is launching a stablecoin. OpenAI rolled out shopping research in ChatGPT. Worldpay introduced tools for agentic commerce. Cash App is piloting a real time score. And a Colorado ruling added pressure to BNPL models.

Earnings stayed solid across the board. Intuit posted strong Q1 growth led by QuickBooks and Credit Karma. Oportun logged another profitable quarter with better credit trends. Pathward finished the year with higher noninterest income. Green Dot’s embedded finance engine kept picking up speed. loanDepot narrowed its loss on stronger margins. BILL delivered steady core revenue gains and new partnerships. Better lifted revenue and continued pushing AI deeper into underwriting.

Quick note. There is no The Free Toaster Jobs Edition this week while the team takes a short Thanksgiving break. You can read last week’s issue here and subscribe to get the next one when it’s back next Friday.

One more thing before we dive in. We are planning a small dinner meetup in Q1 to connect folks in consumer lending who care about building strong direct mail programs. Likely in NYC. If you want details as we finalize plans, reply to this email with “DM meetup” and we’ll keep you posted.

Here’s what’s happening across fintech right now.

Happy Thanksgiving!

— Carlos Caro, Founder at New Market Growth

— Nick Madrid, Co-Founder of Uncovered Media and Ghostmode

PS: To support our Newsletter, please share it with one colleague!

With a single call to our simple, dev-friendly APIs, Spinwheel offers the only comprehensive connection to your consumers' financial accounts. Spinwheel delivers PII, real-time, verified account data, and the ability to make payments across all major debt categories – all within your brand's experience.

With many happy customers, including:

FICO Partners with Plaid to Launch Next-Generation Cash Flow UltraFICO® Score

FICO, the global analytics software leader, just announced a powerful partnership with Plaid, a leading financial data network, to launch the next generation of the cash flow UltraFICO® Score. This new, enhanced solution will combine the proven reliability of the FICO Score, which 90% of top US lenders use, with real-time consumer-permissioned cash-flow data from over 12,000 financial institutions via Plaid's market-leading infrastructure. The goal is to give lenders a single, unified score for "superior consumer risk assessment" without adding operational complexity. FICO vice president Julie May noted that this partnership directly addresses the market's demand for "a broader perspective on consumer credit readiness". Lenders get an immediate boost from this solution as it offers alignment with the flagship FICO® Score, streamlined implementation, and universal compatibility. The collaboration aims to help lenders make "more confident, inclusive credit decisions through a simple and scalable solution," according to Plaid's head of partnerships, Adam Yoxtheimer. (FICO)

CFPB Wants to Eliminate Disparate-impact Claims Under ECOA

The Consumer Financial Protection Bureau (CFPB) is proposing a rule change that would stop lawsuits based on "disparate impact," a legal concept used to punish lenders when their standard policies accidentally hurt specific groups (like racial minorities) even if there was no intent to discriminate. The proposal also makes it harder to prove a lender discouraged people from applying for loans and bans for-profit banks from running special credit programs based on race or sex. The main takeaway is that if this rule passes, regulators and borrowers would need to prove a lender intentionally discriminated, rather than just showing that a bank's policy resulted in unequal outcomes. This shift aligns lending rules with recent Supreme Court decisions and significantly raises the bar for challenging unfair lending practices. (Consumer Finance Monitor)

Why We Invested in Made Card, Jump Capital

Made Card is launching a rewards credit card that aims to turn homeownership, often the biggest monthly expense, into a financial advantage for families, much like Amex did for travel or Ramp did for business spend. The core idea is simple: homeowners deserve rewards that reflect actual spending patterns, which is why Made Card offers 3X points on gas, groceries, utilities, and streaming, 2X points on home improvement and furniture, and, critically, 1X points on mortgage payments up to the total monthly card spend. The card also provides unique savings, allowing cardholders to apply points toward mortgage closing costs or refinancing through partnerships with national companies like Fairway Home Mortgage. The investors backed Made Card because it solves a "real consumer pain point" and creates a "dual-sided model" that delivers value to consumers and improves "stickiness" for industry partners like mortgage originators. The credit card serves as a "strong wedge" to build a much larger financial platform that will eventually help homeowners manage the full property lifecycle, including maintenance, upgrades, and warranties. The timing is ideal, as high mortgage rates and "rising" homeownership costs mean consumers are actively seeking financial products that give something back. (Jump Capital)

Wealthfront Announces Entrance Into The Mortgage Business

Wealthfront is moving into mortgages, giving a small group of Colorado clients early access to an automated home-lending platform that promises lower rates, no sales calls, and a fully self-serve application. The product will expand to Texas, California, and more states ahead of a full 2026 rollout. Wealthfront says its software-driven model cuts origination costs, and early demand suggests its existing users, with a median age of 35 and about $310K on the platform, are ready to fold home buying into the same dashboard they use for savings and investing. It is the firm’s clearest step toward becoming a broader personal finance home rather than a stand-alone investing app. (Housing Wire)

Klarna to Launch Dollar-backed Stablecoin as Race in Digital Payments Heats up

Klarna is rolling out a dollar-backed stablecoin called KlarnaUSD in 2026, positioning it as a faster and cheaper way to move money across borders while regulators in the U.S. and Europe tighten digital asset rules. The token will run on Tempo, a payments-focused blockchain built by Stripe and Paradigm, and is part of a broader shift among major payment firms as PayPal and Stripe have already launched their own stablecoins. Klarna says its automated model will make everyday payments smoother for its largely U.S. user base, and the move marks a sharp turn toward crypto from a company whose CEO was once skeptical. (Reuters)

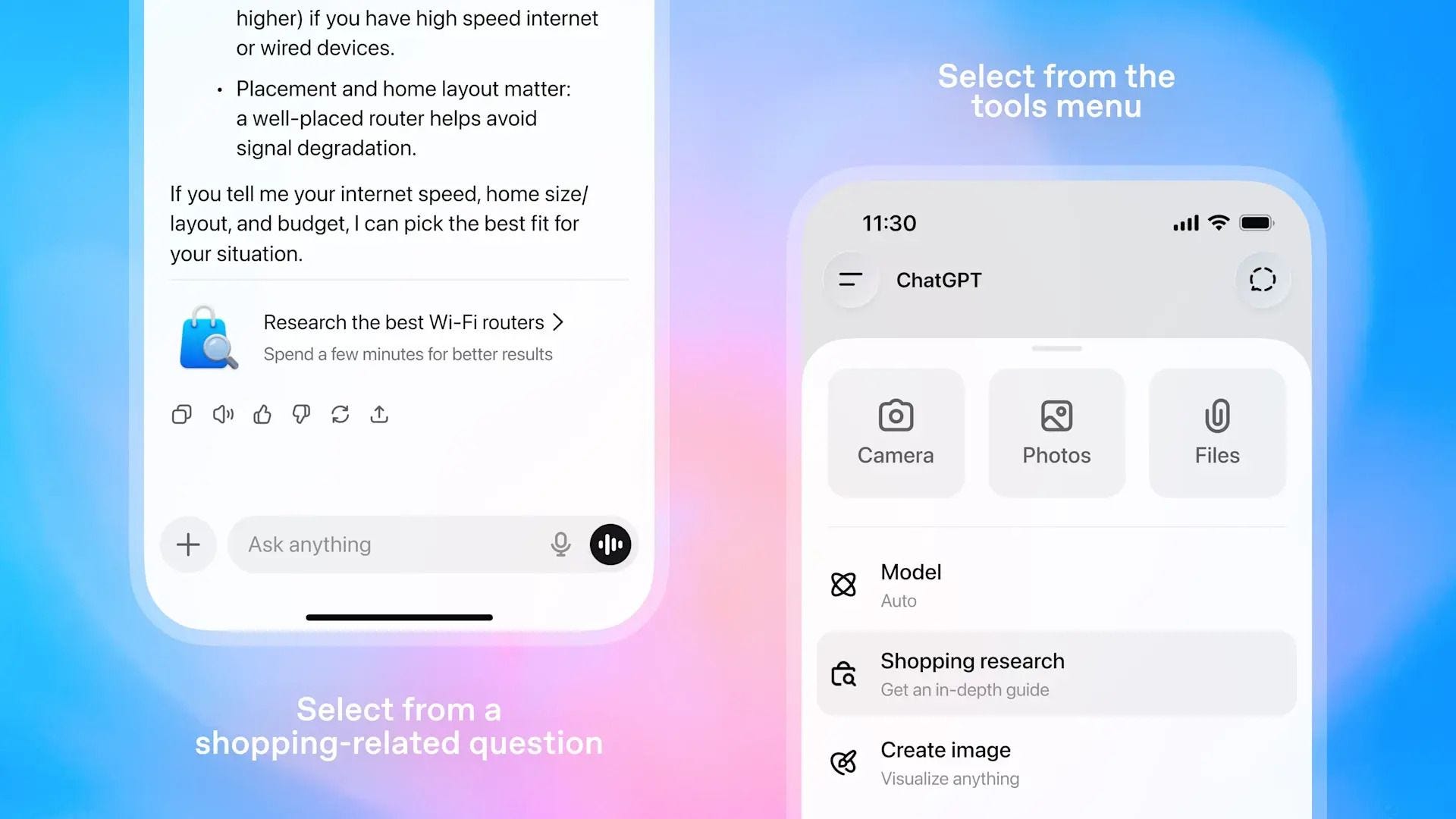

Introducing Shopping Research in ChatGPT

Source: OpenAI

OpenAI is rolling out a new shopping research mode in ChatGPT that builds personalized buyer guides instead of simple product answers. Users describe what they need, and the tool asks clarifying questions, searches trusted sources in real time, and returns curated picks with prices, specs, and tradeoffs. It works across categories like electronics, home, beauty, and sports, and is available on all plans for the holidays. The feature runs on a version of GPT-5 mini trained specifically for product discovery and can tailor results using ChatGPT memory for people who opt in. (OpenAI)

Enjoying this week’s issue?

If you’ve been enjoying The Free Toaster, help us spread the word. Forward it to someone who lives and breathes lending, marketing, or fintech like you do. The best conversations in this space start with a good read.

Your shares help us reach more builders in consumer lending, and help us produce our Newsletter & Podcast.

Worldpay Debuts Model Context Protocol to Bolster Agentic Commerce

Worldpay is rolling out support for agentic commerce with a new Model Context Protocol toolkit that lets developers plug AI agents directly into its payments stack. The MCP standard gives models like ChatGPT, Claude, and Gemini a secure way to read data, trigger workflows, and complete actions, turning them from passive chatbots into systems that can actually perform tasks. Worldpay says nearly half of shoppers are open to letting an AI bot browse for them, and the company is pairing MCP with support for OpenAI’s Agentic Commerce Protocol so ChatGPT users can shop through Instant Checkout at participating merchants. The move positions Worldpay as one of the first major payment processors to build real infrastructure for AI-driven shopping. (PYMNTS)

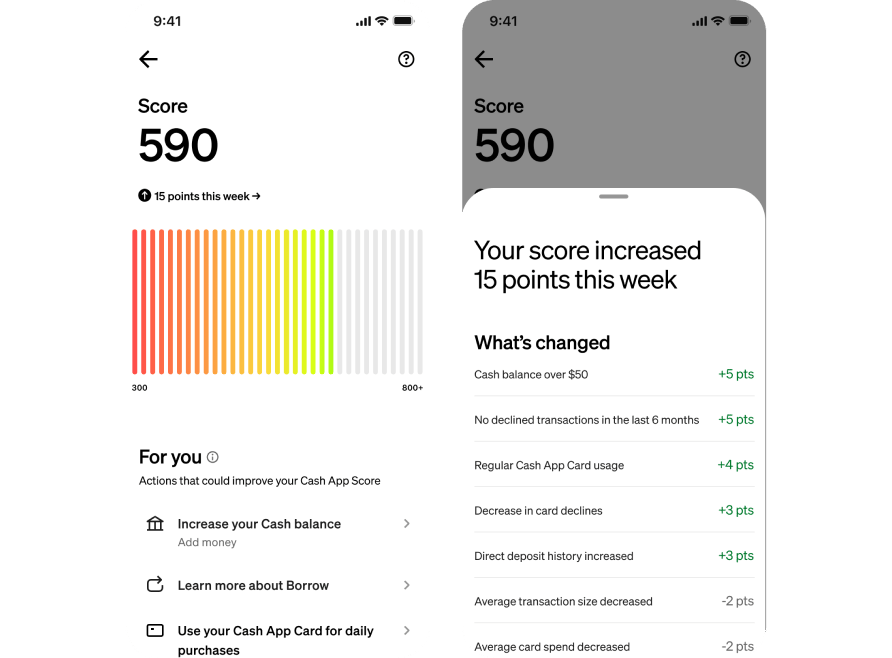

Cash App Score Pilot Launches Utilizing Near Real-time Data

Source: CashApp

Cash App is piloting a new Cash App Score that updates in near real time and shows select users how their day-to-day activity affects their ability to access Cash App Borrow. The score pulls from live signals like paycheck deposits, savings balances, spending patterns, and repayment history, and the app gives personalized steps that can raise a user’s score and increase their borrowing limit. Block says behavioral data is far more predictive than traditional credit files, noting that most Cash App Borrow users have low FICO scores yet maintain strong repayment rates. The broader rollout is planned for 2026 as Cash App positions this model as a more transparent and inclusive form of credit assessment. (CashApp)

Colorado Court Ruling Puts BNPL Lending Models Under Fresh Pressure

A Colorado appellate ruling is creating new pressure for BNPL lenders by allowing the state to apply its interest-rate caps whenever either the borrower or the lending bank is located in Colorado. That change undercuts the rate-exportation model many BNPL firms rely on through sponsor banks and means fees that push effective APRs upward could now breach state limits. Providers warn this adds another layer to an already fragmented regulatory landscape, forcing tighter state-by-state pricing, more compliance staff, and more complex underwriting engines. Some BNPL firms may respond by trimming products in low-cap states or switching to more merchant-subsidized zero-percent plans as they wait to see if other states adopt similar interpretations. (PYMNTS)

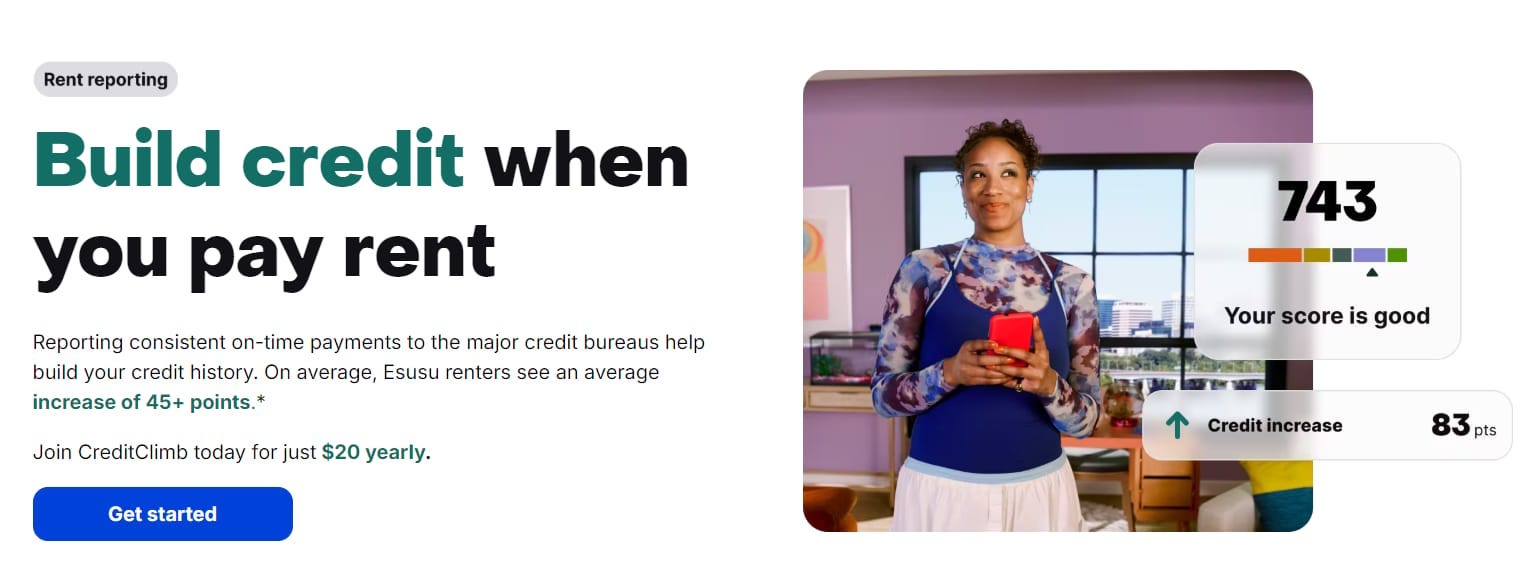

Zillow Lets Renters Report Payments to Credit Bureaus

Source: Zillow

Zillow is launching CreditClimb, a $20-per-year service that lets renters report on-time rent payments to Equifax, Experian, and TransUnion and add up to two years of past payments to their file. The tool is powered by Esusu, whose users have seen average score gains of around 45 points, and aims to help renters qualify for better financing or future rentals by turning an existing monthly expense into a credit-building signal. The move comes as more renters choose to self-report payments even while landlord participation dips, suggesting growing consumer demand for credit access without opening new credit cards. (PYMTS)

Revolut Hits $75B Valuation in New Capital Raise

Revolut has hit a $75 billion valuation after a new share sale led by Coatue, Greenoaks, Dragoneer, and Fidelity, making it one of Europe’s most valuable private tech companies. The round let employees cash out and marks a sharp climb from its $48 billion valuation last year. The neobank is scaling aggressively with banking licenses across Europe and new launches in India, Mexico, and soon Colombia and South Africa, while revenue jumped 72 percent in 2024 to $4 billion and its crypto-focused Wealth division posted explosive growth. Revolut says the raise supports its goal of reaching 100 million customers by 2027 and operating in more than 30 new markets by 2030. (TechCrunch)

Green Dot to Split Fintech, Banking Units in Deals With Smith Ventures, CommerceOne

Green Dot is breaking itself in two, selling its non-bank fintech arm to Smith Ventures for $690 million while merging Green Dot Bank with CommerceOne to form a new publicly traded bank holding company. Shareholders will get $8.11 in cash plus stock in the new entity, and most of the fintech sale proceeds will go to investors and strengthening the bank’s capital base. The split also comes with a seven-year agreement that keeps the combined bank as the exclusive issuing partner for the fintech business. Both deals are expected to close in 2026 pending shareholder and regulatory approval. (MarketWatch)

Please support our Newsletter by recommending us to one of your colleagues!

And, please check out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need to accelerate your affiliate marketing? Chat with New Market Growth

Need to win on other growth channels? Chat with FIAT Growth

Growth Tracker: Earnings and New Investments

Intuit started fiscal 2026 with strong results, growing Q1 revenue 18% to $3.9B and lifting GAAP operating income 97% to $534M, with GAAP EPS up 127% to $1.59. Non-GAAP operating income rose 32% to $1.3B and non-GAAP EPS reached $3.34, up 34%. Global Business Solutions and Consumer each grew 21%, fueled by a 25% jump in QuickBooks Online Accounting and a 27% surge in Credit Karma, while TurboTax and ProTax posted steady gains. Intuit also repurchased $851M in stock and raised its dividend 15%. Management reiterated full-year guidance, expecting 12–13% revenue growth and continued margin expansion driven by its AI-driven platform strategy. (Intuit)

Oportun posted its fourth straight quarter of GAAP profitability, reporting Q3 net income of $5.2M, a $35M improvement from last year, with GAAP EPS of $0.10 and adjusted EPS of $0.39, up sharply from $0.02 in Q2. Revenue rose to $238.7M, and originations climbed 7% to $512M as credit demand held up. Credit metrics improved across the board: the annualized net charge-off rate fell to 11.8% and the 30+ day delinquency rate dropped 44 bps to 4.7%. Operating expenses declined 11% year over year, driving better margins, and the adjusted operating expense ratio improved 123 bps. The portfolio ended the quarter at $2.6B, and management raised full-year adjusted EPS guidance on continued cost discipline and stable credit performance. (Oportun)

Pathward ended fiscal 2025 with a steady Q4, reporting net income of $38.8M, up from $33.5M last year, with diluted EPS of $1.69. Revenue rose 4% to $186.7M, driven by a 13% lift in noninterest income from stronger secondary market revenue and higher card and deposit fees. Net interest margin improved to 7.46% on better asset mix, while adjusted NIM including rate-related partner expenses was 6.04%. Loans and leases closed at $4.66B, up year over year but slightly lower sequentially after moving $144M of consumer finance loans to held-for-sale. Credit trends reflected that shift: the ACL fell to $53.3M, while nonperforming loans rose to 2.05% of total loans. The company repurchased 180,740 shares and finished the year with strong capital levels, including a 12.70% CET1 ratio, as full-year net income reached $185.9M. (Pathward)

Green Dot delivered a strong Q3, growing operating revenues 21% to $494.8M on expanding embedded finance demand and new BaaS launches. Net loss widened to $30.8M due to restructuring charges, equity-method investment losses, and China exit costs, though non-GAAP net income came in at $3.5M. B2B Services remained the growth engine, with segment revenue up sharply to $364.2M, while Consumer trends improved with new financial service center partners. Active accounts and gross dollar volume rose across the platform, and year-to-date adjusted EBITDA reached $159.6M, up 31%. Management raised full-year guidance, now expecting $2.0B–$2.1B in non-GAAP revenue, $165M–$175M in adjusted EBITDA, and $1.31–$1.44 in non-GAAP EPS as embedded finance momentum offsets restructuring and compliance investments. (Green Dot)

loanDepot narrowed its loss in Q3 2025 as revenue rose 14% quarter over quarter to $323.3M, driven by stronger pull-through lock volume, better gain-on-sale margins, and higher servicing income. Net loss improved to $8.7M from $25.3M in Q2, while adjusted net loss tightened to $2.8M. Gain-on-sale margin increased to 3.61% from 3.11% last quarter, and adjusted EBITDA nearly doubled to $48.8M. Pull-through lock volume climbed 10% to $7.0B, though loan originations dipped 3% to $6.5B. Servicing performance remained stable, with the portfolio reaching $118.2B in UPB and 60+ day delinquencies holding at 1.5%. Cash increased to $459M, up $51M sequentially, reflecting improved operating leverage and disciplined expense management. Management said leadership changes and organizational realignment are positioning the company to accelerate tech-enabled origination and expand profitable share in a still-fragmented mortgage market. (LoanDepot)

BILL delivered steady Q1 growth, with revenue up 10% year over year to $395.7M and core revenue up 14% to $358.0M on stronger subscription and transaction fees. The company processed $89B in payment volume, up 12%, and 33M transactions, up 16%. Gross profit reached $318.7M, while non-GAAP operating income was $68.2M. Net loss was $3.0M, though non-GAAP net income held at $70.2M. BILL also announced new Embed 2.0 partnerships with NetSuite, Paychex, and Acumatica, expanding reach across major SMB platforms. Management reiterated FY26 guidance, expecting 9–11% revenue growth and up to $265M in non-GAAP net income. (BILL)

Better reported Q3 revenue of $44M, up from $29M last year, with funded loan volume steady at $1.2B and up 56% year over year excluding a discontinued partnership. Net loss narrowed to $39M from $54M, and adjusted EBITDA loss improved to $25M. Purchase loans accounted for 64% of volume, while HELOC and refi growth drove most of the gains. The company onboarded two major partners in Q3 and a third in October, fueling early Q4 momentum toward a $500M monthly run-rate. Better also advanced its AI stack with automated HELOC underwriting and broader use of Betsy™, and reaffirmed its goal of reaching adjusted EBITDA breakeven by Q3 2026. (Better)

Looking for your next fintech role?

Stay ahead of where the industry is hiring. The Free Toaster Jobs newsletter curates standout openings in fintech marketing, product, data, and risk each week, along with insights into the trends shaping hiring across leading lenders, neobanks, and fintech startups.

Subscribe to The Free Toaster Jobs to get the latest roles and hiring insights delivered straight to your inbox (Toaster subs that don’t opt-in won’t get the Friday jobs Edition).

Missed last week’s edition? Check out the most recent job listings here.

Other News We’re Reading

(Set to Acquire) Capital One Set to Acquire Hopper Travel Software and Hire Key Hotel and Engineering Staff: Scoop (Skift)

(Mortgage Tech) Mortgage tech Haven raises $8M in Series A funding (HousingWire)

(Data Theft) US banks scramble to assess data theft after hackers breach financial tech firm (TechCrunch)

(Regulation) FDIC Capital Rules May Push Banks to Rethink FinTech Partnerships (PYMNTS)

(Payments) Liverpool’s New PayPal Deal Aims To Own The Fan Checkout (Forbes)

(Fintech) NY AG’s office scrutinizes SoLo Funds (Banking Dive)

(Agentic Money) AIUSD Launches First Agentic Money Infrastructure, Backed by Elite AI, Crypto, and Fintech Leaders (Reuters)

(BNPL) David’s Bridal Taps Sezzle to Bring BNPL to the Wedding Aisle (PYMNTS)

(Regulation) Bank Policy Institute Leads Opposition to Stripe Banking Charter (PYMNTS)

(CFPB) Lenders Brace for CFPB’s Underwriting Shakeup (PYMNTS)

(CFPB) Lawmakers Encourage CFPB to Protect Consumer Choice While Rewriting Rule 1033 (PYMNTS)

(Retail Media) CVS Turns First-Party Data Into Retail Media Power Play (PYMNTS)

(Agentic Payments) EMVCo Working on How Global Specifications Can Support Agentic Payments (EMVCo)

(AI Deal) Intuit CFO talks $100 million OpenAI deal, innovation, and the road ahead (Fortune)

(Asset Finance) FIS Expands Auto Market Presence with Cloud-based Asset Finance Solution (FIS)

(AI Leadership) Wells Fargo Names Saul Van Beurden to Lead Artificial Intelligence; Kleber Santos to Expand Responsibilities and Serve as Co-CEO of Consumer Banking and Lending with Van Beurden (Wells Fargo Newsroom)

Spot something worth sharing with your team? Drop this week’s edition in their inbox:

Catch you next week,

The Free Toaster Team

p.s. If you’re working on anything new in acquisition or credit, we’re always curious to hear about it.