NerdWallet's Q1 '26 Earnings: Why Is The Stock Down 18%?

NerdWallet reduced the lower end of their full year guidance, and it spooked investors

NerdWallet (NASDAQ: NRDS) reported $222 million in Q1 2026 revenue this week, up 6% YoY. Non-GAAP operating income hit a Q1 record of $34 million.

The headlines were fine.

The Q&A was less fine IMO (see below for my take).

Source: NerdWallet Q1 ‘26 investor letter.

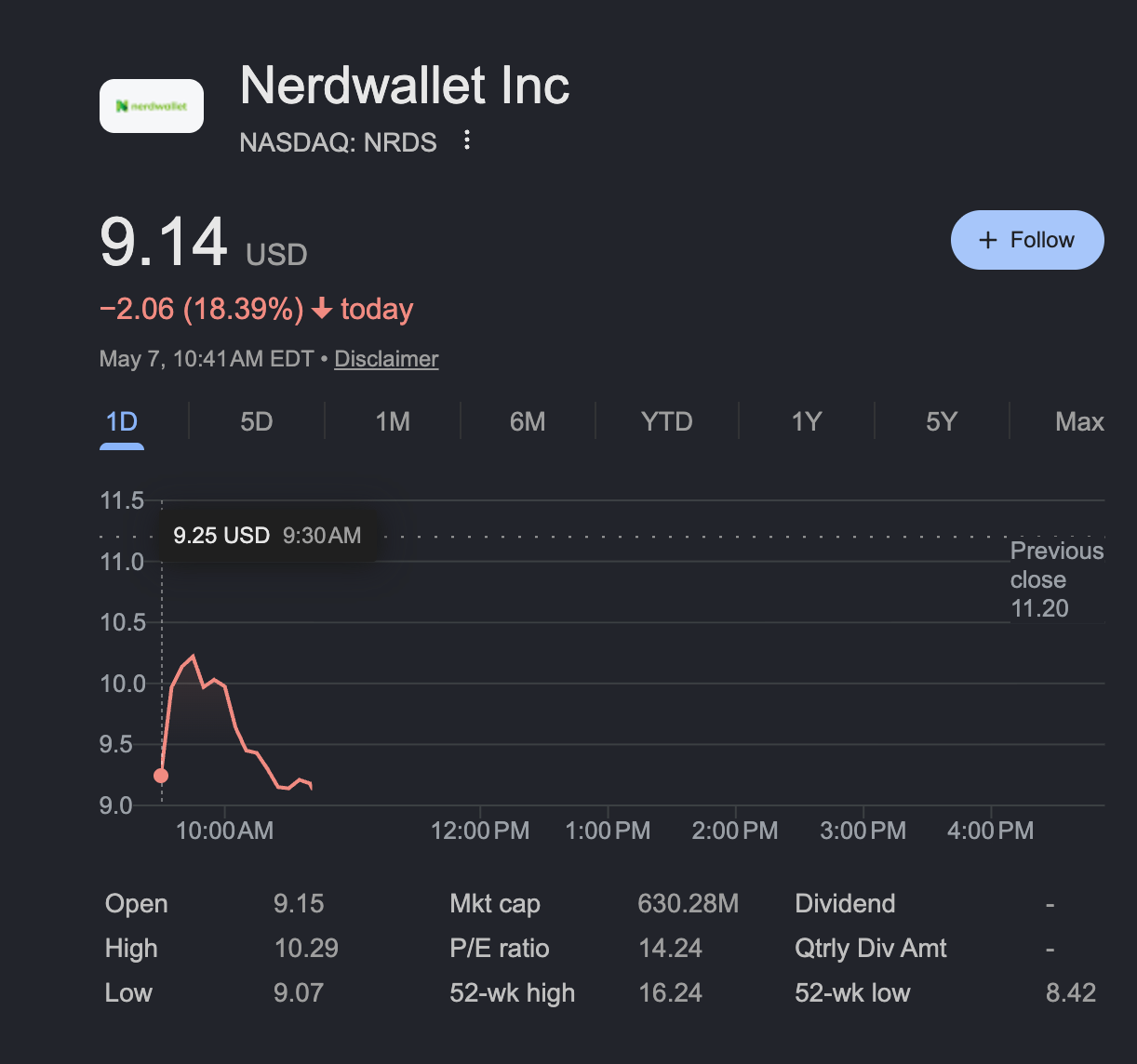

And, the stock market’s reaction (down 18% after the earnings report) reflects a “maybe things aren’t fine at NerdWallet” POV.

Source: Google.

The call had at least five moments worth flagging. We pulled them out so you don’t have to sit through the 45 minute call yourself.

One auto insurance carrier flinched and the full-year guidance changed.

CEO Tim Chen didn’t sugarcoat it: “We have a lot of concentration towards a few carriers currently and a few channels.”

A single large carrier pulled back in March. That alone was enough to ding Q1, is expected to hit Q2 harder, and force NerdWallet to lower the bottom of full-year NGOI guidance.

If one insurance partner can move the full-year P&L, maybe the recent gains they’d seen in insurance weren’t broad-based. Maybe one or two carriers were leaning in (read: had extra marketing budget NerdWallet happened to capture), and are now moving back to a more sustainable position.

From past earnings reports (we covered the previous one here), the data was showing their former flagship business - credit cards - has been on a steady decline since 2023.

The narrative was that insurance was rocket-shipping to save the day.

Now the question is whether insurance follows credit cards down once the carriers driving recent growth pull back.

SMB is down 15% and nobody on the call seemed to care.

SMB revenue dropped 15% YoY, to $25M. The reason given in prepared remarks was a single sentence: “Within our SMB vertical, we saw year-over-year declines driven by organic search headwinds.” Motley Fool

That was it. No turnaround plan. No timeline. No diagnosis of which SMB products are bleeding versus holding.

Then the Q&A opened up. Three analysts asked three questions, about vertical integration spend, NGOI guidance math, and LLM traffic. Zero on SMB.

Either the sell side has already written SMB off, or management has trained them not to ask. Neither is a good look for a category that, just a few quarters ago, was being talked about as a meaningful diversification story.

Worth noting: buried in the CFO’s prepared remarks was a note that the SMB decline was partially offset by growth in loan originations. That’s an interesting positive, small business loan demand showing up in the funnel, and not one analyst pulled the thread.

That give you clues on where SMB sits in the priority stack right now.

“Organic search headwinds” is doing a lot of heavy lifting.

That phrase shows up for both SMB and credit cards. It’s a polite way of saying Google and AI are eating our free traffic.

Tim’s LLM update, within the context of the insurance business: NerdWallet has dominant share of money-related queries inside LLMs, conversion is high, and it’s “a very small piece of our overall pie right now from a revenue perspective.”

Translation: the channel that’s growing isn’t material to the insurance business, yet. The old cash cow channel, SEO, is shrinking. That’s a scary reality for a business that depends on low cost, high-conversion traffic to thrive.

(For more on this dynamic, see our prior piece, The SEO Apocalypse Has Arrived.)

The margin beat had a Super Bowl-sized asterisk on it.

Q1 NGOI - at $34 million - looked great. Why? Per CFO Lauren StClair, the gain came from “lower other marketing expenses on lower brand spend, partially offset by higher performance marketing spend.”

In English: they didn’t run a Super Bowl ad this year, brand spend dropped, and they put more dollars into performance marketing.

Two takeaways:

The margin lift is partially a one-time comp benefit, not a structural improvement. Q2 NGOI is guided down from $34M to $6M–$14M.

A NerdWallet that buys more of its traffic each year is a NerdWallet that needs partners with elite conversion economics. Expect more pressure on bounty/CPA pricing, more A/B tests, and less patience for clunky application flows.

If your funnel is mid, I expect you’re going to feel the pressure. Best conversion rates will rise to the top, and the average/bad ones could effectively disappear.

“Vertical integration” sounded more defensive than offensive.

Morgan Stanley’s analyst directly asked Tim to walk through the ROI math on the new investments. The answer leaned on “our cost of capital is pretty high” and the idea that AI tools make it cheaper to build internally.

Building NerdWallet Insurance Experts, a branded agency routing calls to captive and independent agents, is a real pivot from their credit card content days.

NerdWallet is moving from lead-gen marketplace to operating their own customer-facing financial services business. That’s a different animal than referrals.

They’re entering it partly because the referral business is under pressure. Read into that what you want.

You partner with, or are considering partnering with NerdWallet. Now what?

NerdWallet still has the brand, the traffic, and the cash flow to be a top distribution partner, especially if you’re in deposits or personal loans (both growing). But this call had the texture of a company transitioning from a high-margin SEO business to a paid-traffic-and-services business. Both of which play outside of their historical competencies and could have a different margin profile.

Action items:

Ask your NerdWallet rep how your specific category (let’s say credit cards), is trending, at the top of the house. You need to know if the decline you’re seeing is you losing market share or you preserving or building share inside a declining category.

Audit your conversion funnel. In a performance-marketing-led NerdWallet, conversion is placement. Double down here. The last thing you want is for NerdWallet to conclude that your offer doesn’t work when the traffic source moves from free (SEO) to $20 per click from Google or Meta.

Diversify your affiliate mix, and work through what you’d do if a partner you currently count on for a good chunk of your volume were to create a shock in your lead flow.

At the highest level, I empathize with NerdWallet’s struggles.

I think their brand has an incredible amount of equity and trust in the category, and I’m rooting for them to get through this rough patch and back into sustainable, strategic growth in the lending category.

But, given the clues they dropped in this quarter’s earnings, I can’t help but be a bit worried about their future in a world where SEO continues to decline in importance.

Want this kind of breakdown in your inbox every Wednesday? You know what to do.