Happen Bank Is Running Chime in Reverse Playbook — Here's the Bet

Lend first, earn the deposit relationship later. How the bank formerly known as LendingClub is running Chime's playbook backwards.

Hey Toaster Readers,

This week is sponsored by New Market Growth.

With the slow news cycle and the July 4th holiday, we decided to reflect a bit more on one story that recently dropped. We think it was easy to skip but there there is something deeper at play that others might appreciate.

Last Tuesday, LendingClub officially ceased to exist and rebranded to Happen Bank. We covered the initial announcement in April, but the dust has settled and we wanted to dig into the strategy underneath. This is one of the clearest examples we have seen of a lender picking a specific customer segment, the “Motivated Middle,” and engineering every product and reward around them. If you market lending or deposit products, you will want to spend five minutes unpacking how Happen ties its rewards directly to profitable customer behaviors.

Let’s get toasting!

(Don’t miss our First big Toaster Summit)

Affiliate Marketing Summit for Lenders and Publishers

Proudly Sponsored by Experian & Engine by Gen

We have a new site! And our Day 2 experience (which has much smaller capacity) is selling faster than we anticipated.

LendingClub Became Happen. The Real Story Is Who It’s Chasing.

Last Tuesday, Scott Sanborn rang the Nasdaq opening bell and LendingClub officially ceased to exist. The company now trades as Happen, Inc. under the ticker HAPN, having completed both a full rebrand to Happen Bank and a stock listing switch from the NYSE to Nasdaq. [American Banker]

We covered the announcement when it dropped in April. So why come back to it now that the paint is dry? Because to us, there’s a more interesting story layered under the rebrand.

This is one of the cleanest examples we’ve seen of a lender picking a customer segment first and then engineering every product, reward, and dollar of funding around that one person. If you market lending or deposit products for a living, this is worth 5 minutes unpacking.

First, what Happened to Lending Club?

Quick scale check: Happen reports 5M+ lifetime members and $100B+ in lifetime originations (sourced from their 2025 10-K).

For readers who know LendingClub as “the P2P lending pioneer”: that company hasn’t existed for years. Happen is a nationally chartered digital bank running a marketplace bank model with two revenue engines.

The first engine is the balance sheet. Deposits fund loans held for investment, generating net interest income. The second engine is the marketplace. Happen originates loans and sells them to investors, collecting origination fees, servicing fees, and gains on sale capital-light fee income.

The loan book is overwhelmingly consumer: unsecured personal loans (debt consolidation is the core franchise), auto refinance, point-of-sale financing, and a newly launched home improvement vertical. A small commercial book focuses primarily on active SBA lending, while existing commercial real estate loans and equipment leases have ceased origination and are being retained to maturity.

In Q1 2026, originations were split roughly down the middle, 52% sold to marketplace investors and 48% retained, which matters for the strategy below. Both engines get stronger when the same borrower gets cheaper to fund and safer to underwrite.

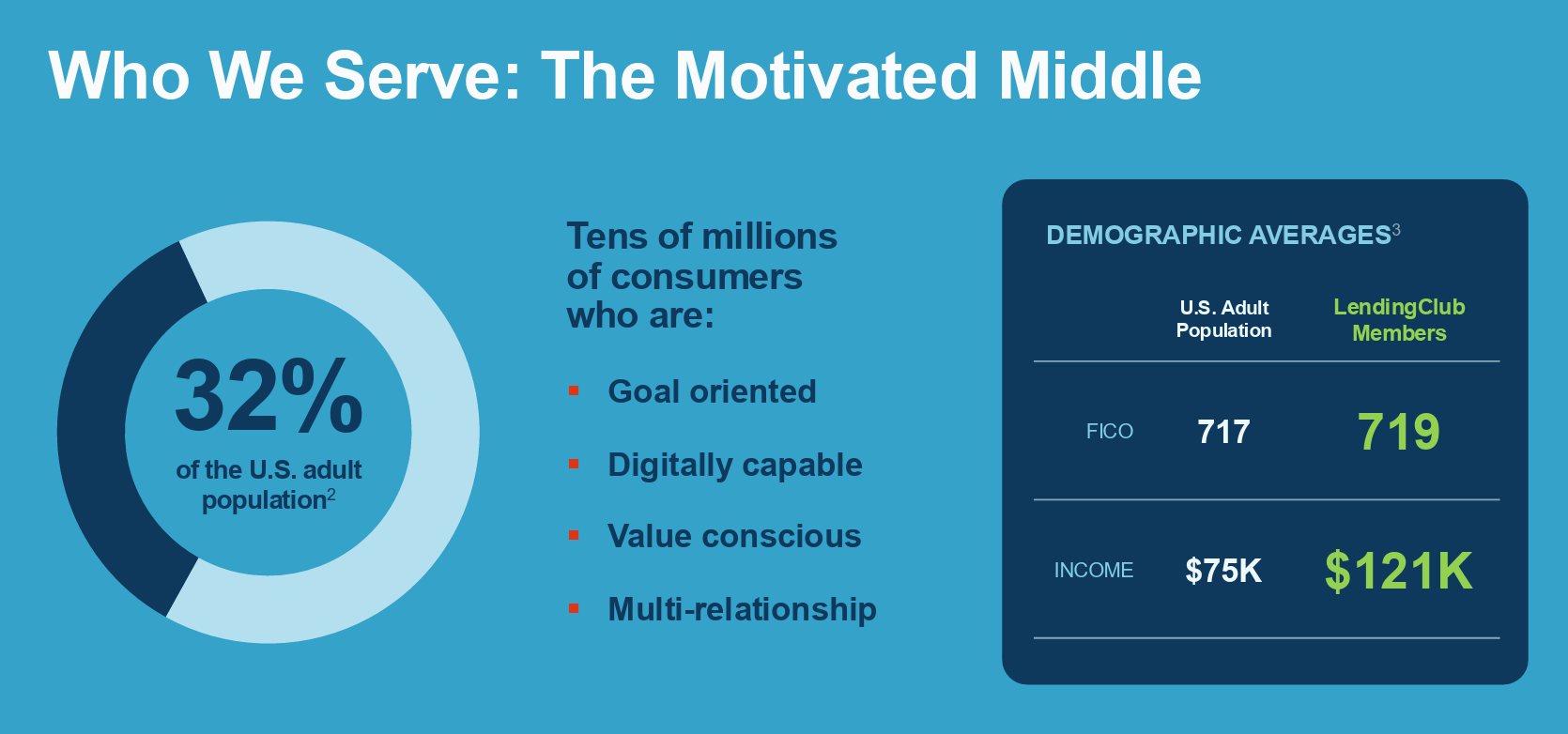

Happen focusing on the “Motivated Middle”

Happen’s own words: it’s a bank built for “high-FICO, high-income, digitally savvy consumers actively managing their financial lives.” Not the underbanked. Not private-banking clients.

Prime borrowers who still actively use credit.

Look around the industry and you see why this lane was open.

Chime and Dave built their businesses on low-to-moderate-income consumers — overdraft protection, early wage access, interchange-funded economics. SoFi staked out high earners with student loan refi, wealth management, and premium lifestyle branding. Chase, Citi, and BofA sit on trillions in near-zero-cost deposits but don’t always succeed in securing the consumer’s lending business.

The middle, the person with a 740 FICO who carries a $25K consolidation loan and a real savings balance, was nobody’s primary target. Happen is planting a flag there.

The sequencing question (Chime in reverse)

Chime did the hardest thing in consumer banking first: winning the direct deposit relationship, then expanding into credit. Happen is running the opposite play, and it’s the same one SoFi, Capital One, and Amex ran before it. Lend first, because that’s where the money is (and, frankly, because a lending license is far easier to get than a bank charter). Then use the loan relationship to earn your way into deposits and checking.

Loan-first is the more logical sequence for profitability.

But it leaves Happen with a real challenge: it doesn’t own the primary banking relationship yet, and the deposit market is brutally crowded. Which distribution channels it picks to close that gap is the thing to watch over the next few quarters.

But first, a quick note from our sponsor:

New Market Growth

New Market Growth helps lenders build and scale affiliate marketing programs on channels like Credit Karma, Experian Marketplace, Lending Tree, Bankrate, Credible, and many more. NMG clients spend $50-$100MM per year in affiliate channels, and the founding team (one of whom is Free Toaster co-founder Carlos Caro), have advised in excess of 50 lenders over the course of their corporate and agency careers.

If you’re a Free Toaster Reader at a lender that spends over $500K per month in affiliate marketing, we’re offering a free, 90-minute audit of your affiliate marketing program. After research we’ll conduct on our side, we’ll book time to share the strengths, weaknesses, and opportunities we observe in your program.

Outside eyes could help unlock the growth you’re looking for in H2 2026.

Email carlos@newmarketgrowth.com with subject line “90-minute audit” and we’ll contact you to get the preliminary information we need to get to work.

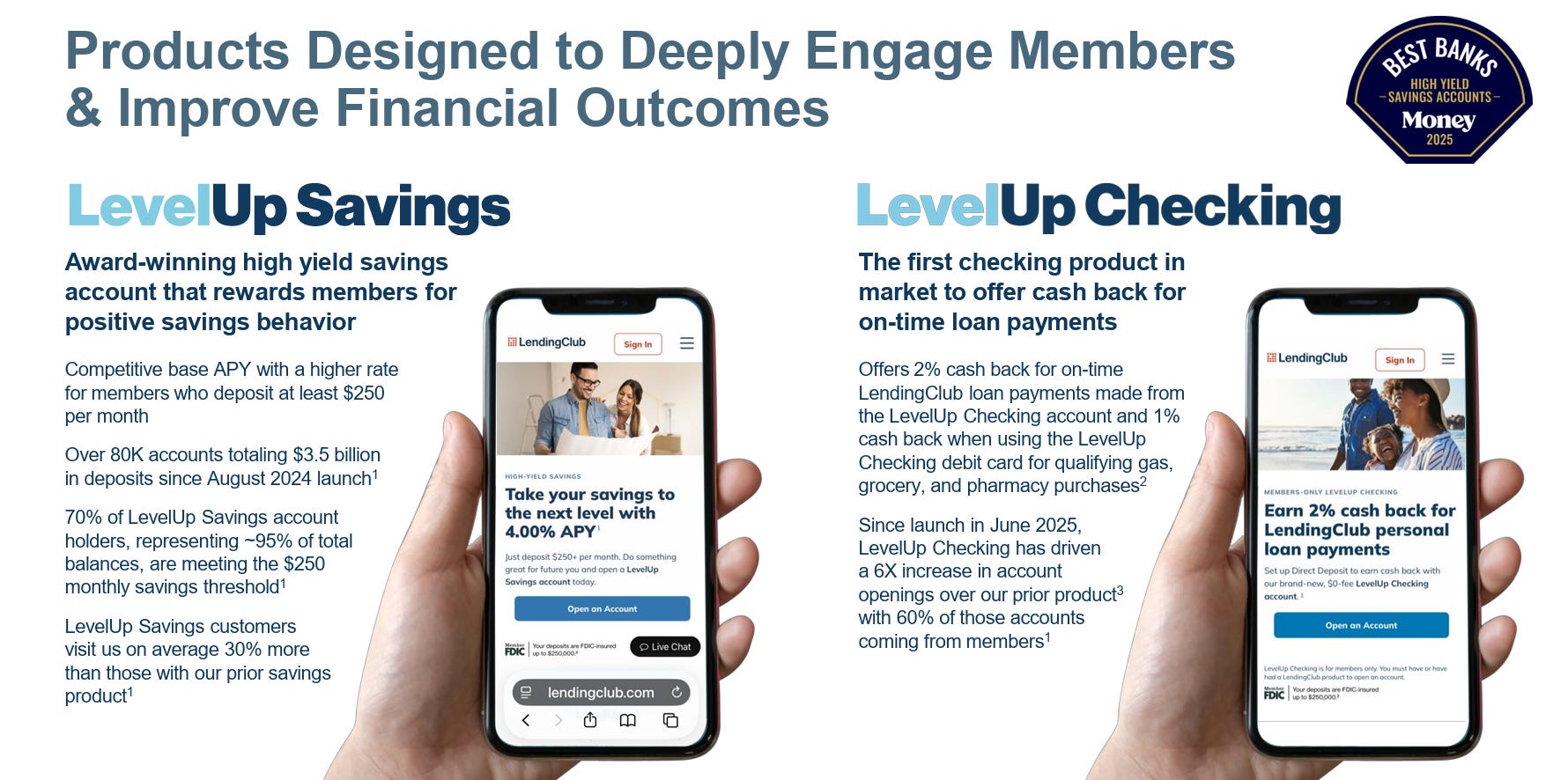

The flywheel: rewards that pay for behaviors, not balances

This is where the strategy gets concrete. Happen’s two deposit products are engineered so that every reward dollar buys a behavior that improves Happen’s own bottom line.

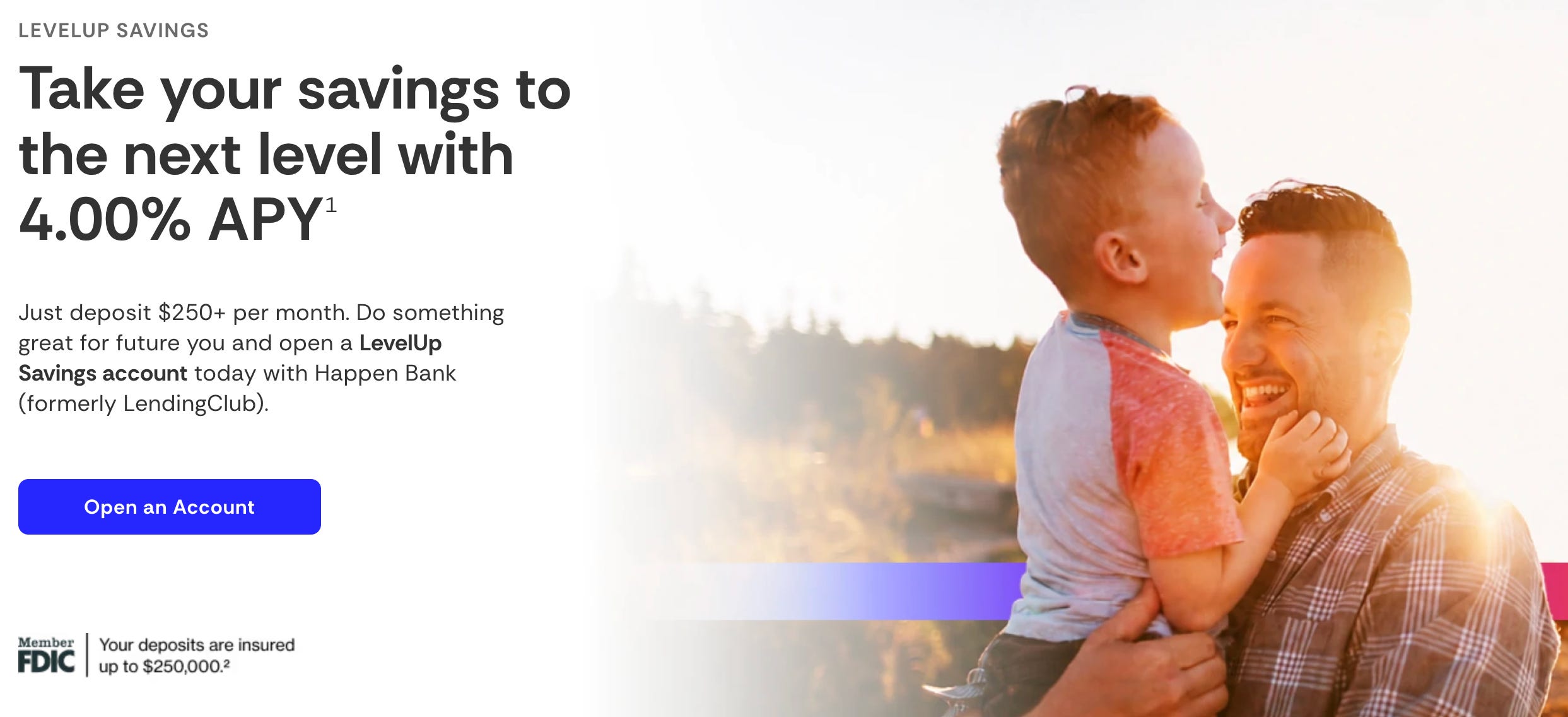

LevelUp Savings (launched August 2024) pays a higher APY (currently 4% APY) to members who deposit at least $250/month, rewarding the growth behavior instead of the raw balance. It’s built 80K+ accounts and $3.5B in deposits, and savings customers visit 30% more often than the prior product’s.

[LevelUp Savings] built 80K+ accounts and $3.5B in deposits, and savings customers visit 30% more often than the prior product’s.

LevelUp Checking (launched June 2025) pays 2% cash back on on-time personal loan payments made from the account, plus 1% back on gas, grocery, and pharmacy debit purchases. It simultaneously pulls low-cost deposits in, moves loan servicing inside Happen’s ecosystem, and pays the borrower to do the exact thing that keeps charge-offs down. Since launch, account openings are running 6x the prior checking product, and 60% of accounts come from existing members. The cross-sell is seemingly working.

Now the number that left us scratching our heads a bit.

Happen discloses that 70% of LevelUp Savings holders, representing ~95% of balances, hit the $250 monthly threshold. Do the basic math they invite: 95% of $3.5B spread across 70% of 80K accounts works out to an average balance near $59K among threshold-meeting savers. (The disclosed account and balance figures are as of March 31, 2026)

That’s not a mass market audience.

That’s an affluent saver earning 4.00% APY, which raises a question Happen hasn’t answered: why is that customer with $59K in savings taking out a $20–30K personal loan? Either the savers and the borrowers are different pockets of the member base, or the “prime borrower who still borrows” is wealthier than the debt-consolidation stereotype suggests.

TOASTER’S TAKE

The rewards program is designed thoughtfully for the audience (and the P&L). Every Happen incentive pays for a behavior tied to a P&L line (deposit cost, on-time payment, balance growth).

The deposit business doesn’t reduce CAC, it raises the CAC you can afford. When 60% of new checking accounts come from existing borrowers, the lifetime value of a new loan customer goes up. That lets you bid more for media and buy growth on the margin. At scale, the Fortune 500 banks of the world happily push CAC up as long as the marginal customer is profitable. The question for Happen: is that what the next two quarters of marketing spend will show?

The metrics we want to understand this better: checking account volumes (they gave us savings, why not checking?), cross-hold rates, and blended CAC. Until then, we have a number of questions: How many of those affluent savers came from the loan base versus straight rate-shopping on 4.00% APY? Does the flywheel actually convert borrowers into primary banking relationships, or just into high-yield deposits?

Happen’s bet?

That the most overlooked customer in consumer finance is the prime saver who still borrows — and that you win them by paying them to behave in ways that improve your deposit base, your loss curves, and your cross-sell rates all at once.

Only time will tell and the proof will show up in the CAC and cross-sell numbers.

Please support our Newsletter by sharing this edition with a colleague!

And, consider checking out our sponsors:

Need an affiliate marketing platform/network? Chat with Fintel Connect

Need to improve application page conversions? Chat with Spinwheel

Need help with performance marketing? Chat with Bulldog Media Group

Need to grow in big marketplaces like Credit Karma? Chat with New Market Growth

Need to hire top-tier talent in fintech or lending? Chat with CTB1

Looking for a new role?

The Free Toaster Jobs Edition tracks where fintech teams are actually investing across marketing, product, data, credit, risk, and partnerships.

Catch you next week,

The Free Toaster Team

P.S.: If you’d like to sponsor or host an event in the consumer lending community in 2026, we’d like to hear from you. The Free Toaster will be organizing & hosting curated events this year, and we’d love to work with you as a sponsor.